May 15, 2025

ISSB: Emerging Global Standard for Sustainability Reporting

Understand the importance of optimizing workflow processes to enhance efficiency. Learn techniques for identifying bottlenecks, streamlining tasks, and implementing workflow automation.

Stephen Pell

Co-founder and CEO

Standards

4 Min Read

The sustainability reporting landscape is undergoing rapid transformation, and finance leaders are now at the forefront of that change.

With the release of IFRS S1 and S2, the International Sustainability Standards Board (ISSB) has laid the foundation for a globally consistent approach to sustainability-related financial disclosures. These standards are not simply regulatory developments; they represent a material shift in how businesses assess and communicate risk, performance, and long-term value.

For CFOs, the implications are clear: sustainability is no longer adjacent to financial reporting. It is becoming structurally integrated with it.

The Shift from Parallel ESG Reporting to Financial Integration

Historically, sustainability disclosures have operated in parallel to financial reporting, relying on assumption-based data, fragmented methodologies, and varying regional standards. While these efforts have created visibility, they have fallen short of the assurance, comparability, and decision-usefulness expected by investors, auditors, and boards.

The ISSB seeks to resolve this disconnect by embedding sustainability reporting within the architecture of financial disclosure. Built on the widely accepted TCFD framework, the ISSB introduces a clear set of expectations designed to align sustainability metrics with enterprise value and financial risk.

This evolution brings sustainability into familiar territory for finance professionals: materiality, auditability, and accountability.

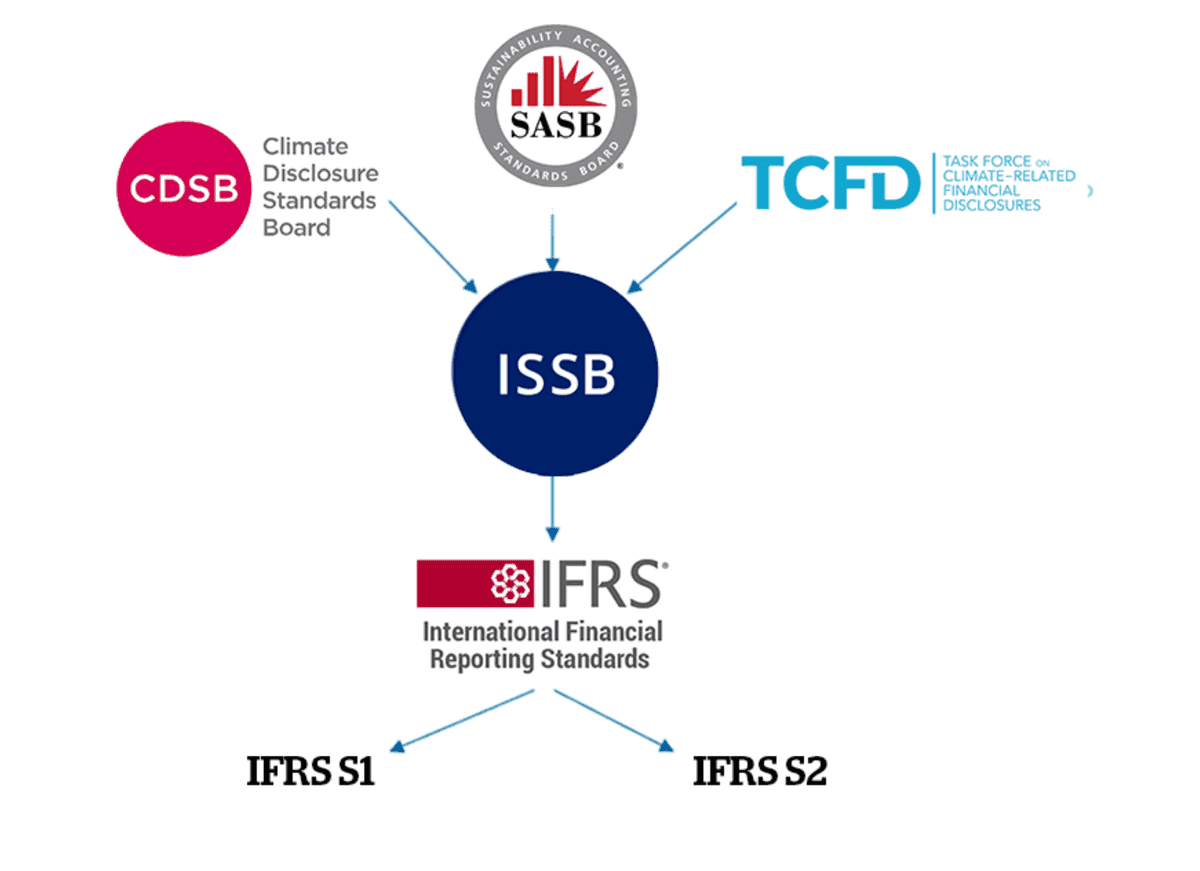

The ISSB Standards at a Glance

The ISSB has issued two core standards:

IFRS S1: General Requirements: Mandates disclosure of all sustainability-related risks and opportunities that could reasonably be expected to affect a company’s financial position, performance, or prospects. Designed to complement existing financial accounting standards, S1 ensures disclosures align with the financial statements in timing, assumptions, and presentation.

IFRS S2: Climate-related Disclosures: Builds on S1 with detailed requirements related to climate-specific risks and opportunities. These include Scope 1–3 emissions, scenario analysis, mitigation strategies, resilience assessments, and climate-related metrics aligned with industry-specific guidance. S2 formalises and enhances the recommendations of the Task Force on Climate-related Financial Disclosures (TCFD), which now falls under ISSB governance.

Together, these standards enable organisations to provide a coherent, investor-focused narrative on how sustainability risks are identified, managed, and reflected in financial outcomes.

Why CFOs and Financial Reporting Teams Must Take the Lead

More than 30 jurisdictions, representing over half of global GDP, are already incorporating ISSB standards into national policy frameworks. The UK’s forthcoming Sustainability Reporting Standards (UK SRS) are expected to align closely with ISSB guidance, accelerating the transition from voluntary reporting to mandatory compliance.

For CFOs and financial reporting teams, this represents both a challenge and an opportunity:

Challenge: Existing ESG systems may lack the rigour, traceability, and financial integration required under ISSB. Compliance will demand new processes, cross-functional collaboration, and greater assurance over non-financial data.

Opportunity: Finance functions are uniquely positioned to lead this integration, bringing governance, internal control, and materiality discipline to sustainability reporting. In doing so, they elevate sustainability from a reporting exercise to a strategic capability.

Characteristics of a Finance-Led Approach to Sustainability Reporting

To meet the demands of ISSB, and future regulatory expectations, organisations will need to evolve their sustainability reporting infrastructure. The emerging model will be characterised by:

System integration: Sustainability-related risks and metrics must be embedded in financial planning, forecasting, risk management, and capital allocation frameworks.

Assurance readiness: Disclosures must be supported by robust documentation, data lineage, and internal controls, consistent with those applied to financial statements.

Strategic relevance: ESG reporting should move beyond compliance to inform decision-making, clarifying the financial impact of climate, resource, and reputational risks.

Board alignment: As reporting becomes subject to audit and board oversight, finance leaders will play a central role in translating sustainability disclosures into business model implications.

A Final Thought

The introduction of ISSB standards marks a significant milestone in the evolution of corporate reporting. It signals a world where sustainability performance is assessed with the same discipline as financial results, and where finance teams have a critical role to play in ensuring accuracy, alignment, and strategic relevance.

This is not simply about adapting to a new reporting framework. It is about redefining how organisations understand value, resilience, and risk in a changing world.

Finance is no longer a passive observer in the sustainability transition. It is the engine that must drive it forward.