CSRD Compliance Templates for Supply Chain Reporting

Sep 18, 2025

Explore essential templates for CSRD compliance that streamline supply chain reporting on environmental, social, and governance impacts.

The Corporate Sustainability Reporting Directive (CSRD) mandates organisations to report on the environmental, social, and governance (ESG) impacts across their entire value chain. Meeting these stringent requirements involves detailed data collection, supplier engagement, and alignment with European Sustainability Reporting Standards (ESRS).

To simplify compliance, several tools and templates are available, each tailored for specific reporting needs:

neoeco: Integrates ESG data into financial systems for automated reporting and audit-ready precision. Best for organisations seeking a unified financial and sustainability approach.

GHG Protocol Supply Chain Template: Focuses on greenhouse gas (GHG) emissions reporting, particularly Scope 3, but relies heavily on manual data entry.

ESRS-Compliant Reporting Framework: Offers structured reporting aligned with full CSRD requirements, including environmental, social, and governance metrics.

SBTi Value Chain Emissions Tracker: Helps organisations track and report Scope 3 emissions in line with science-based targets.

GRI Supply Chain Impact Assessment Template: Prioritises social and environmental impact assessments with detailed supplier monitoring.

Each option varies in automation, integration, and focus. Choosing the right tool depends on your organisation's goals, supply chain complexity, and reporting maturity.

ESRS VSME Reporting Template (CSRD) - Demo Video

Key Requirements for CSRD Supply Chain Templates

Meeting the Corporate Sustainability Reporting Directive (CSRD) standards means gathering extensive ESG data across the entire value chain. Reporting templates need to capture both quantitative metrics - like greenhouse gas (GHG) emissions, water usage, and waste production - and qualitative evaluations of supplier practices and risk management strategies.

The European Sustainability Reporting Standards (ESRS) form the backbone of CSRD compliance, offering a detailed framework that covers environmental, social, and governance (ESG) dimensions. On the environmental side, ESRS addresses areas such as climate change, pollution, water management, biodiversity, and circular economy principles. Social standards focus on workforce conditions, labour practices within the value chain, community impacts, and consumer-related concerns. Governance requirements emphasise business ethics and corporate governance structures.

To meet these rigorous standards, templates must reflect both impact and financial materiality. This includes maintaining robust audit trails, automated data validation, detailed source records, and clear accountability. Such measures are essential to ensure the data can withstand external assurance processes, particularly for emissions calculations.

GHG Protocol alignment is a critical component for consistency with established carbon accounting methods. Templates should calculate Scope 1, Scope 2, and, most importantly, detailed Scope 3 emissions as outlined by the GHG Protocol. For organisations aiming to manage Scope 3 emissions comprehensively, templates must capture supplier-specific data across all fifteen Scope 3 categories. This level of detail is crucial for organisations working on Scope 3 emissions management.

Sector-specific requirements add an extra layer of complexity. For instance:

Manufacturers may need to track the impacts of raw material extraction.

Service industries might focus on evaluating indirect supplier relationships.

Financial institutions must document financed emissions.

Retailers often require product lifecycle assessments.

Templates must be adaptable to these industry-specific needs while adhering to ESRS guidelines.

CSRD also demands a high level of data granularity. Effective templates should capture details at the facility level, assess product-specific impacts, and account for temporal variations. This granular data supports more accurate impact evaluations and aligns with the directive's focus on forward-looking disclosures and target-setting.

Another key requirement is integrating sustainability data with financial reports. This ensures consistency and comparability with financial statements. For organisations looking to adopt this approach, exploring financially-integrated sustainability management can provide valuable insights into aligning sustainability efforts with financial reporting.

Lastly, stakeholder engagement is a crucial part of CSRD compliance. Organisations must document how they engage with stakeholders across their value chain, including suppliers, local communities, and civil society groups. Templates should provide structured methods to record stakeholder feedback, outline engagement processes, and demonstrate how this input informs sustainability strategies and reporting priorities.

1. neoeco

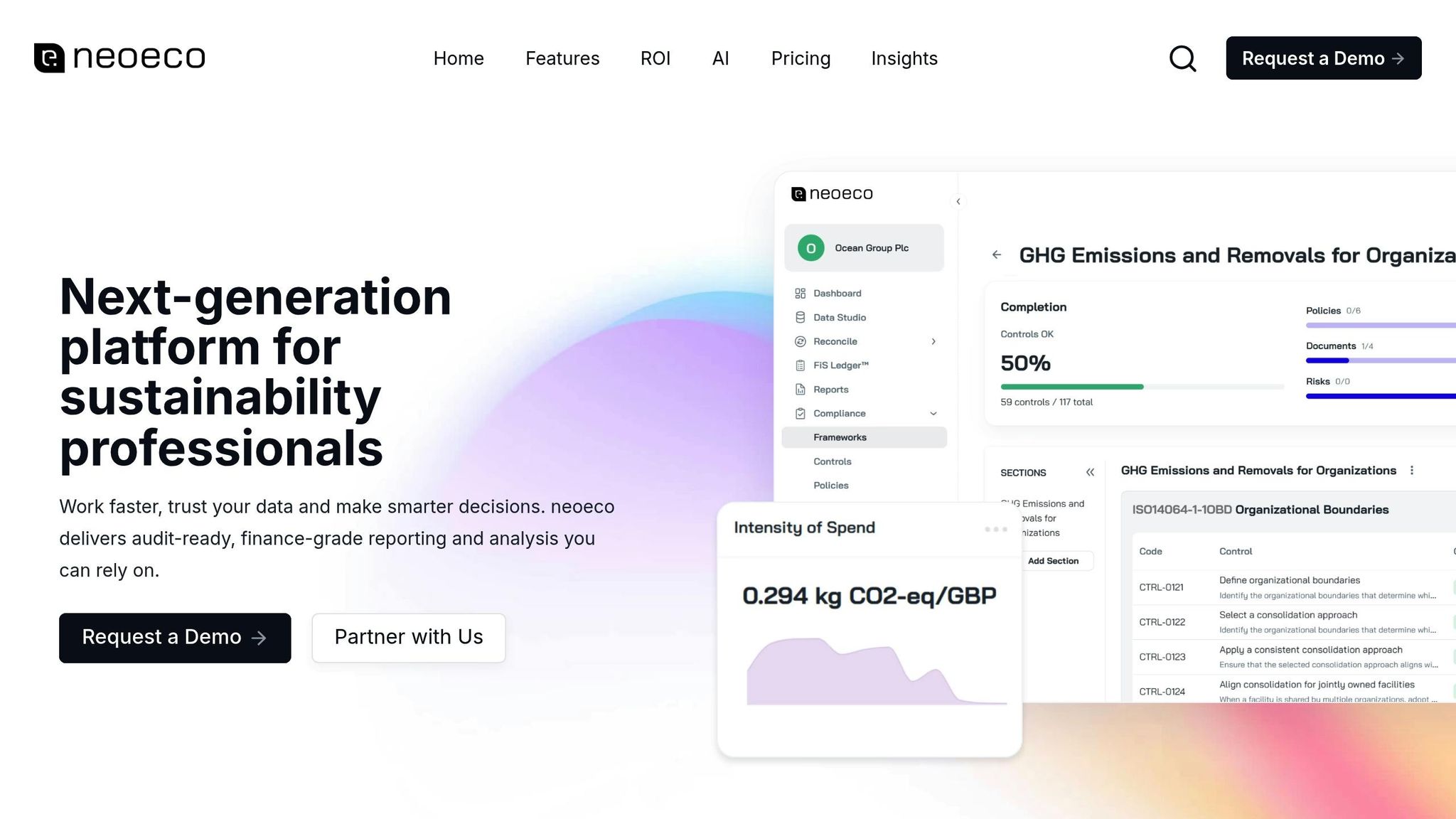

neoeco is a financially-integrated sustainability management (FiSM) platform that transforms how CSRD supply chain reporting is handled. It achieves this by embedding ESG data directly into every financial transaction using its unique FiS Ledger. Instead of treating sustainability as a separate entity, neoeco merges financial and sustainability data into one cohesive system.

Supported Standards and Frameworks

neoeco aligns with key frameworks such as ISSB (IFRS S1 & S2), GHGP, TCFD, SBTi, SASB, CDP, and GRI. Its ISSB reporting ensures that supply chain data gathered for CSRD compliance can also meet the requirements of multiple regulatory frameworks. This multi-purpose approach reduces redundant efforts and streamlines reporting processes.

Automation and Integration Capabilities

With AI-powered automation, neoeco simplifies data collection by reducing manual input. It integrates smoothly with accounting tools like Xero and QuickBooks, as well as ERP systems, energy metres, and HR platforms. This seamless connectivity creates automated data flows, capturing sustainability impacts in real time.

The FiS Ledger incorporates over 90 ESG impact factors into financial transactions using double-entry principles. This means every transaction automatically generates sustainability data, bridging the gap between financial and ESG reporting while reducing inconsistencies. This method ensures the platform is ready for audits and supports accurate reporting.

Audit-Readiness and Data Granularity

neoeco is built to deliver audit-grade precision. It maintains detailed audit trails and provides granular insights across 96 ESG categories. This level of detail supports CSRD external assurance requirements and enables comprehensive Scope 3 emissions reporting.

Suitability for Supply Chain Contexts

neoeco is tailored to address the complexities of CSRD supply chain reporting. Its Life Cycle Assessment (LCA) methodologies are particularly effective for tracking environmental impacts throughout a product's life cycle. This offers a full value chain perspective that aligns with ESRS standards.

The platform’s modular design allows businesses to customise reporting for their specific sectors. Whether it’s tracking raw material impacts for manufacturers, assessing indirect supplier relationships for service providers, or documenting financed emissions for financial institutions, neoeco adapts to meet diverse needs. For organisations managing extensive Scope 3 emissions, its real-time tracking capabilities provide continuous monitoring, enabling forward-looking disclosures and target-setting under CSRD guidelines.

2. GHG Protocol Supply Chain Template

The GHG Protocol Supply Chain Template serves as a key tool for measuring and reporting greenhouse gas (GHG) emissions across supply chains. Developed by WRI and WBCSD, it provides the foundational methodology that many organisations use to align with CSRD requirements for supply chain emissions reporting.

Supported Standards and Frameworks

This template is designed to align with CSRD's ESRS E1 requirements for Scope 3 emissions reporting. It incorporates the Corporate Value Chain (Scope 3) Standard, which categorises indirect emissions into 15 distinct groups. This detailed structure helps companies conduct the in-depth value chain impact assessments demanded by CSRD.

Additionally, the template integrates seamlessly with frameworks like the Science Based Targets initiative (SBTi) and CDP reporting standards. Many organisations rely on it to gather emissions data before transferring information to more advanced platforms. By bridging theoretical frameworks and practical execution, the template ensures solid documentation that stands up to audit scrutiny.

Audit-Readiness and Data Granularity

One of the template's strengths lies in its ability to support detailed audit documentation. It requires companies to record the sources, methods, and assumptions used for each category of emissions, creating clear audit trails. This approach aligns with CSRD's external assurance requirements, allowing auditors to trace emissions calculations back to their origins.

However, the template’s manual nature poses challenges for real-time reporting. Data is often collected on an annual or quarterly basis, which may not fulfil CSRD’s push for more frequent sustainability updates. Moreover, the reliance on supplier questionnaires and industry averages can raise concerns about data accuracy during audits.

Suitability for Supply Chain Contexts

The template is particularly effective for addressing the complexities of multi-tiered supply chains. Its 15 Scope 3 categories ensure that all indirect emissions are accounted for, meeting CSRD's focus on detailed and forward-looking data. It’s especially well-suited for manufacturers with stable supplier networks, offering clear guidance on data collection methods, from spend-based calculations using economic models to supplier-specific data gathering.

For organisations managing extensive Scope 3 emissions, the template provides a structured way to identify emission hotspots and prioritise reduction strategies. It also includes tools for assessing uncertainty, which are crucial for preparing transparent CSRD disclosures. These tools allow companies to communicate data reliability and outline plans for improvement. Additionally, the methodology supports scenario analysis, enabling businesses to model the potential impact of supply chain changes on emission reductions.

3. ESRS-Compliant Reporting Framework

The ESRS-Compliant Reporting Framework is designed to align supply chain data collection with the Corporate Sustainability Reporting Directive (CSRD) by adhering to the European Sustainability Reporting Standards (ESRS), which came into effect in January 2024. This framework ensures that data is collected and reported in a structured way to meet the specific requirements of the CSRD.

Supported Standards and Frameworks

The framework is organised into four key ESRS sections: general overview, environmental matters, social matters, and governance matters. This structure ensures that supply chain data is reported in a manner that aligns with CSRD disclosures. Beyond the essential ESRS requirements, it supports integration with additional standards like the EU Taxonomy, TCFD, and SBTi. This integrated approach is particularly helpful for organisations with complex supply chains, allowing them to gather data once and use it across multiple reporting obligations. Looking ahead, the framework is prepared for the sector-specific ESRS standards expected in 2026, ensuring it remains compatible with future developments. These integrations also pave the way for more effective digital automation in subsequent phases.

Automation and Integration Capabilities

Modern ESRS frameworks incorporate ESG reporting software to handle large volumes of supply chain data. These systems often include supplier portals that facilitate direct data submissions, minimising manual input and improving data accuracy through built-in validation rules. API integrations enable seamless connections to existing enterprise systems like ERP platforms and procurement databases, which is particularly important for organisations with extensive supplier networks. Additionally, the framework automatically standardises data to align with local conventions, enhancing compatibility and usability.

This level of integration improves data traceability and ensures readiness for audits.

Audit-Readiness and Data Granularity

Every data point within the framework is trackable, supported by version control and detailed documentation of collection methods, assumptions, and validation processes. Features such as version control and the ability to upload evidence create transparent, supplier-level audit trails. The framework emphasises data granularity, capturing detailed information at the supplier level - covering areas like emissions data, human rights practices, and governance metrics - rather than relying on general industry averages. Tools for uploading certifications, audit reports, and other verification documents further strengthen third-party assurance and improve the reliability of reported data.

Suitability for Supply Chain Contexts

This framework is particularly well-suited to addressing the challenges of supply chain sustainability, focusing on key impacts such as Scope 3 emissions and social risks. It includes specialised tools for supplier engagement, such as training modules and standardised templates to ensure consistent data collection across diverse supplier bases. Multi-tiered supply chain mapping capabilities allow organisations to gain a deeper understanding of their value chains by identifying critical suppliers and assessing their impacts. Additionally, performance tracking features enable ongoing monitoring and provide support for suppliers that may need additional guidance. For organisations managing global supply chains, localisation features ensure that varying regulatory requirements and reporting standards are accommodated while maintaining overall ESRS compliance.

4. SBTi Value Chain Emissions Tracker

The Science Based Targets initiative (SBTi) Value Chain Emissions Tracker offers a structured way to monitor supply chain emissions, helping organisations meet CSRD obligations. Since value chain (or Scope 3) emissions often make up 70% to 90% of a company’s total greenhouse gas emissions, tracking these is critical for thorough sustainability reporting. This tool ensures alignment with established GHG protocols and CSRD standards.

Supported Standards and Frameworks

The tracker is designed to align with the Greenhouse Gas Protocol, which provides guidelines for greenhouse gas accounting and setting targets. It addresses all 15 Scope 3 categories outlined by the GHG Protocol, covering both upstream and downstream emissions. This broad coverage is essential for CSRD compliance, as the European Sustainability Reporting Standards require detailed reporting across all three emissions scopes.

Automation Capabilities

Digital platforms integrated with the SBTi framework simplify data collection and enhance supplier performance tracking. By centralising Scope 3 data, these tools make it easier to identify categories, calculate emissions, and maintain proper documentation.

Documentation and Audit-Readiness

Under the SBTi framework, targets must include at least 67% of reported mandatory Scope 3 emissions. This requirement places emphasis on maintaining accurate records of calculations and assumptions, ensuring readiness for future audits and assurance standards.

Suitability for Supply Chain Reporting

The tracker is particularly effective for organisations where Scope 3 emissions account for more than 40% of their overall greenhouse gas footprint. Its methodical approach aligns with CSRD's focus on detailed Scope 3 emissions management. By enabling systematic reporting, it supports credible climate strategies and ensures compliance with CSRD’s rigorous disclosure requirements.

5. GRI Supply Chain Impact Assessment Template

The Global Reporting Initiative (GRI) Supply Chain Impact Assessment Template is designed to evaluate the environmental and social effects across an organisation's value chain. By focusing on material, non-financial impacts, it helps reinforce a company's commitment to sustainability while aligning with CSRD compliance requirements.

Supported Standards and Frameworks

This template is grounded in two key GRI Topic Standards: 308: Supplier Environmental Assessment and 414: Supplier Social Assessment. These standards require organisations to report on their economic, environmental, and social impacts throughout their supply chain. The modular structure of the template allows businesses to select Topic Standards that align with their identified material topics, ensuring relevance to their unique supply chain contexts.

The template tracks around 30 supply chain metrics and over 90 data points. These include details such as the number of new suppliers screened for environmental and social criteria, assessments of supplier impacts, identified negative impacts within the supply chain, and cases where supplier relationships were terminated due to sustainability issues. This detailed approach not only supports CSRD's focus on thorough impact reporting but also aligns with frameworks like CDP, SASB, and TCFD.

Automation and Integration Capabilities

Advancements in ESG platforms have brought automation to GRI reporting, simplifying data collection and offering real-time insights. These tools enable organisations to monitor their supply chains more effectively, ensuring suppliers meet sustainability goals while supporting compliance with CSRD requirements.

Audit-Readiness and Data Granularity

One of the key strengths of the GRI template lies in its detailed data requirements and robust documentation processes. By collecting data from both internal systems and suppliers, the template ensures a comprehensive view of supply chain impacts. However, this requires the use of standardised templates with clearly defined data points, sources, responsible parties, and quality assurance checks.

By focusing on impact measurement rather than purely financial metrics, the template provides auditors with concrete evidence of sustainability performance. For organisations managing Scope 3 emissions in real-time, its emphasis on supplier assessment data creates valuable audit trails that meet both GRI and CSRD reporting standards. This level of documentation is crucial for conducting practical and effective supply chain impact assessments.

Suitability for Supply Chain Contexts

The GRI template is particularly suited to organisations aiming to demonstrate thorough impact management across their value networks. Unlike frameworks that prioritise financial relevance, GRI places a strong emphasis on a company's effects on people and the environment. This makes it an excellent choice for businesses with complex supply chains, where impacts often extend well beyond direct operations.

Its integration capabilities allow businesses to utilise existing supplier data while building comprehensive impact assessments that meet both GRI and CSRD requirements. The flexibility to work alongside other reporting frameworks ensures consistent messaging across various sustainability disclosures. Such detailed assessments are vital for achieving robust supply chain reporting that aligns with CSRD standards.

Template Comparison: Features and Benefits

When choosing a template for your organisation's CSRD supply chain reporting needs, it's essential to assess each option's capabilities and how they align with your goals. The table below summarises the key features of the available templates.

Template | Supported Standards | Automation Level | Audit-Readiness | Integration Capabilities | Best Suited For |

|---|---|---|---|---|---|

neoeco | ISSB (IFRS S1 & S2), CSRD, GHGP, TCFD, SBTi, SASB, CDP, GRI | AI-driven automation with FiS Ledger embedding 90+ ESG factors | Audit-grade accuracy through double-entry principles | Seamless integration with Xero, QuickBooks, ERP systems, energy metres | CFOs and finance teams requiring financially-integrated sustainability management |

GHG Protocol Supply Chain Template | GHGP, CSRD (partial), SBTi | Manual data entry with basic calculation tools | Strong documentation framework for Scope 3 verification | Limited integration; requires manual data import | Organisations focused primarily on carbon emissions tracking |

ESRS-Compliant Reporting Framework | CSRD (full compliance), TCFD, GRI (partial) | Moderate data automation | High audit-readiness with structured disclosure requirements | Moderate integration with existing ESG platforms | EU companies requiring comprehensive CSRD compliance |

SBTi Value Chain Emissions Tracker | SBTi, GHGP, CSRD (emissions only) | Automated target tracking and progress monitoring | Strong verification processes for science-based targets | Good integration with carbon management systems | Companies with established science-based targets |

GRI Supply Chain Impact Assessment Template | GRI 308, GRI 414, CDP, SASB, TCFD | Real-time monitoring through ESG platforms | Comprehensive impact documentation across 90+ data points | Flexible integration with supplier assessment tools | Organisations prioritising social and environmental impact measurement |

The table highlights the core differences, but understanding how these features impact your compliance strategy is equally important.

Standards Coverage and Compliance Depth

neoeco stands out for its broad standards coverage, including ISSB, making it a strong choice for multinational organisations managing diverse reporting requirements. Its versatility simplifies compliance across multiple frameworks.

In comparison, the GHG Protocol template focuses on emissions reporting, which is ideal for organisations just starting with sustainability efforts. However, its limited scope may not fully address the broader CSRD requirements, potentially necessitating additional tools as regulations expand beyond carbon metrics.

Automation and Efficiency

Automation plays a critical role in reducing manual effort and minimising errors. neoeco leverages AI-driven FiS Ledger technology to embed ESG data directly into financial transactions, creating an automated and reliable audit trail.

On the other hand, templates like the GHG Protocol rely heavily on manual data entry, which can be a time-intensive process, especially for organisations with complex supply chains. However, this manual approach can allow for greater customisation and control over data validation, which some organisations may prefer.

Integration and Ease of Implementation

For organisations managing complex reporting systems, seamless integration with accounting tools and ERP systems is essential. neoeco excels in this area, creating a unified data ecosystem that supports real-time data capture and detailed audit trails. This capability is especially valuable when managing Scope 3 emissions in real time, as supplier data can flow directly into reporting systems without interruption.

The ESRS-Compliant Reporting Framework, while offering moderate integration, may require more manual configuration to align with existing workflows. Organisations must weigh the trade-offs between automation and the customisation required for their technical infrastructure.

Cost and Resource Considerations

Costs can vary significantly between templates. neoeco operates on an annual licensing model, offering modular add-ons that help reduce long-term operational expenses through automation. Conversely, the GRI template provides pricing flexibility but may require additional investment in training and integrating with existing systems.

Scalability and Future-Readiness

As CSRD requirements evolve, scalability becomes a key factor. neoeco's comprehensive framework ensures organisations are well-prepared for future regulatory changes, aligning with the FiSM manifesto to integrate sustainability into core financial processes. This proactive approach minimises the risk of needing costly system replacements as compliance demands grow.

Ultimately, the right choice depends on your organisation's current sustainability maturity, technical setup, and long-term compliance strategy. Platforms like neoeco offer comprehensive automation and financial integration, making them ideal for organisations seeking a unified approach. Meanwhile, more targeted templates may better suit companies focused on specific compliance frameworks or just beginning their sustainability journey.

Implementation Methods and Documentation Best Practices

Achieving effective CSRD supply chain reporting hinges on a well-organised data collection and documentation process. Given the complexity of modern supply chains, careful planning and the right technological tools are essential to ensure compliance.

Building a Centralised Data Framework

For CSRD compliance to work seamlessly, organisations need a unified data system capable of managing diverse supply chain information. Disconnected data silos can disrupt consistency and make traceability a challenge.

neoeco's FiS Ledger technology addresses this by embedding over 90 ESG impact factors directly into financial transactions using double-entry accounting principles. This approach ensures sustainability data is accurate enough to meet audit standards. By unifying data collection, it simplifies supplier engagement and creates a strong foundation for compliance.

This integration eliminates the need for separate systems to gather data. Instead, environmental and social impacts are automatically recorded and categorised during procurement transactions. This reduces manual errors and provides real-time visibility into supply chain activities, aligning seamlessly with CSRD requirements.

Engaging Suppliers and Collecting Data

Engaging suppliers effectively means creating systems that allow continuous data collection rather than relying on periodic updates. For example, integrating ESG data collection into routine processes like invoice approvals or contract renewals can normalise this practice for suppliers. When suppliers see ESG reporting as part of standard business operations, compliance rates tend to improve.

CSRD documentation also requires organisations to detail the methodologies and assumptions used in their supply chain calculations. This involves keeping thorough records of data sources, conversion factors, and any estimates made when direct data isn’t available. Life Cycle Assessment (LCA) methodologies often underpin these calculations, ensuring they hold up under scrutiny.

With a steady stream of data coming in, automated checks become critical to maintaining quality.

Automation and Ensuring Data Quality

Relying on manual processes for CSRD compliance can lead to errors, especially when dealing with complex supply chains that involve hundreds or even thousands of suppliers. Automation simplifies this by mapping supplier data to CSRD categories, applying conversion factors, and flagging potential quality issues. This is especially useful for managing Scope 3 emissions in real time, where supplier actions can directly influence an organisation's carbon footprint.

Automated validation rules are essential for quality assurance. For instance, energy consumption data outside expected ranges can be flagged automatically for review, helping to prevent errors from spreading through the reporting system. By combining automated data capture with financial system integration, organisations can achieve audit-grade precision.

Keeping Documentation Audit-Ready

CSRD compliance requires organisations to maintain detailed, well-organised documentation that supports every disclosed figure and methodology. This documentation must be readily accessible to auditors and provide clear links between the raw data and final reports.

Digital audit trails play a key role here, recording every step from data collection to final reporting. These trails capture who collected the data, when it was processed, what calculations were applied, and any adjustments made during reviews.

Documentation should also include evidence of supplier verification processes, such as third-party certifications or on-site inspections. When primary data isn't available, organisations must explain why industry averages or estimates were used and outline plans to improve data quality in future reporting cycles.

Integrating Sustainability with Financial Systems

As mentioned earlier, embedding sustainability data into financial systems is crucial for CSRD compliance. This integration ensures that sustainability reporting meets the same standards of accuracy and auditability as financial reporting.

The FiSM manifesto highlights how combining sustainability management with financial processes helps organisations maintain a unified approach to ESG compliance. By aligning sustainability data with core financial operations, businesses can ensure their CSRD reporting achieves the transactional accuracy auditors expect.

This integration also supports real-time monitoring of supply chain impacts. For example, if a supplier’s environmental performance declines, the system can flag the issue and calculate its effect on overall CSRD metrics, enabling proactive responses.

Adapting and Scaling for the Future

As supply chains grow and regulations evolve, organisations must continuously refine their data collection and reporting methods. Successful systems include feedback loops to learn from each reporting cycle, which can lead to improvements in data quality, supplier engagement, and system performance.

Scalability is another critical factor, especially for businesses expanding into new markets or increasing their supplier base. The chosen platform should handle additional data, new reporting requirements, and larger supplier networks without requiring major system overhauls. By planning for growth, organisations can ensure their investments in CSRD compliance infrastructure remain valuable over time.

Conclusion

Selecting the right CSRD supply chain reporting templates can transform compliance from a daunting task into a manageable process. This guide has highlighted several options, ranging from the GHG Protocol's structured approach to emissions tracking to neoeco's method, which integrates sustainability data directly into financial systems.

Achieving effective CSRD compliance hinges on aligning reporting tools with your organisation's existing processes. Tools that ensure audit-grade accuracy and integrate seamlessly with financial systems are essential. Manual data collection simply cannot meet the real-time visibility demanded by CSRD. Automated solutions, on the other hand, not only simplify data capture but also align sustainability reporting with financial workflows.

Integrating ESG impact factors into financial systems ensures precise, unified reporting. This eliminates the gap between sustainability and financial data, enabling more strategic decisions. As regulations and supply chains continue to evolve, scalable and automated tools become a necessity, ensuring compliance both now and in the future.

Investing in systems that combine sustainability management with financial integration provides a strong, adaptable framework for CSRD reporting. This approach not only addresses current requirements but also positions organisations to meet the growing demands of global sustainability standards. By adopting automated, integrated tools, businesses lay the groundwork for meeting today's compliance needs while preparing for tomorrow's challenges.

For organisations committed to long-term success in sustainability reporting, financially-integrated sustainability management offers a comprehensive and forward-thinking solution.

FAQs

How can I choose the right CSRD compliance template for my organisation's supply chain reporting needs?

Choosing the right CSRD compliance template hinges on your organisation's specific reporting needs and how intricate your supply chain is. Start by determining whether you require a solution that provides end-to-end automation or a more targeted tool for managing and documenting supply chain emissions and related data.

When evaluating templates, ensure they align with your CSRD compliance obligations. Focus on key aspects like emissions reporting, double materiality, and audit preparedness. It’s also worth considering platforms that integrate both financial and sustainability data, as these can simplify the reporting process. Tools that utilise AI or methodologies such as Life Cycle Assessment (LCA) can offer valuable, real-time insights to enhance your reporting accuracy.

For a more integrated approach, platforms like neoeco are designed to bring together financial and sustainability data. This can help organisations meet CSRD requirements effectively while staying aligned with global reporting standards.

What are the main differences between manual and automated data collection for CSRD compliance, and how do they affect reporting accuracy?

Manual data collection for CSRD compliance depends heavily on human effort, making it both time-consuming and susceptible to mistakes. These errors can result in inconsistencies or inaccuracies in reporting, which may compromise an organisation's ability to meet compliance standards.

In contrast, automated data collection leverages advanced tools like AI to gather and process information efficiently and consistently. This approach minimises errors, boosts data accuracy, and ensures adherence to CSRD requirements. By adopting automation, organisations can save valuable time, improve the reliability of their data, and deliver reports that are more dependable and trustworthy.

How does integrating sustainability data with financial systems improve CSRD supply chain reporting?

Integrating sustainability data into financial systems ensures precise, consistent, and comprehensive reporting across both financial and non-financial metrics. By aligning these systems, organisations can minimise manual errors, simplify data validation, and leverage automated processes for data collection and verification. This makes meeting CSRD reporting and audit standards far more straightforward.

Tools like neoeco play a key role here, offering AI-powered automation and real-time insights. These platforms help organisations manage compliance more efficiently while keeping records audit-ready. The result? Greater transparency, reduced audit complexities, and significant savings in both time and resources.