ISSA 5000:

The New Global Standard for Sustainability Assurance

Sustainability disclosures are now subject to the same audit scrutiny as financial reports. ISSA 5000 provides the global assurance framework that auditors will use to validate ESG data under CSRD, ISSB, and UK SRS.

What Does ISSA 5000 Cover?

ISSA 5000 applies to assurance engagements over any sustainability information prepared by a reporting entity — whether that information is quantitative, qualitative, or forward-looking in nature.

This includes quantitative disclosures, such as greenhouse gas emissions, Scope 1, 2, and 3 data, and other environmental metrics that can be numerically measured and reported. Equally important are qualitative disclosures, encompassing governance structures, sustainability strategies, risk management approaches, and climate risk mitigation plans. ISSA 5000 also extends to forward-looking information, such as transition plans, net zero targets, scenario analysis outcomes, and any assumptions underpinning future-state disclosures.

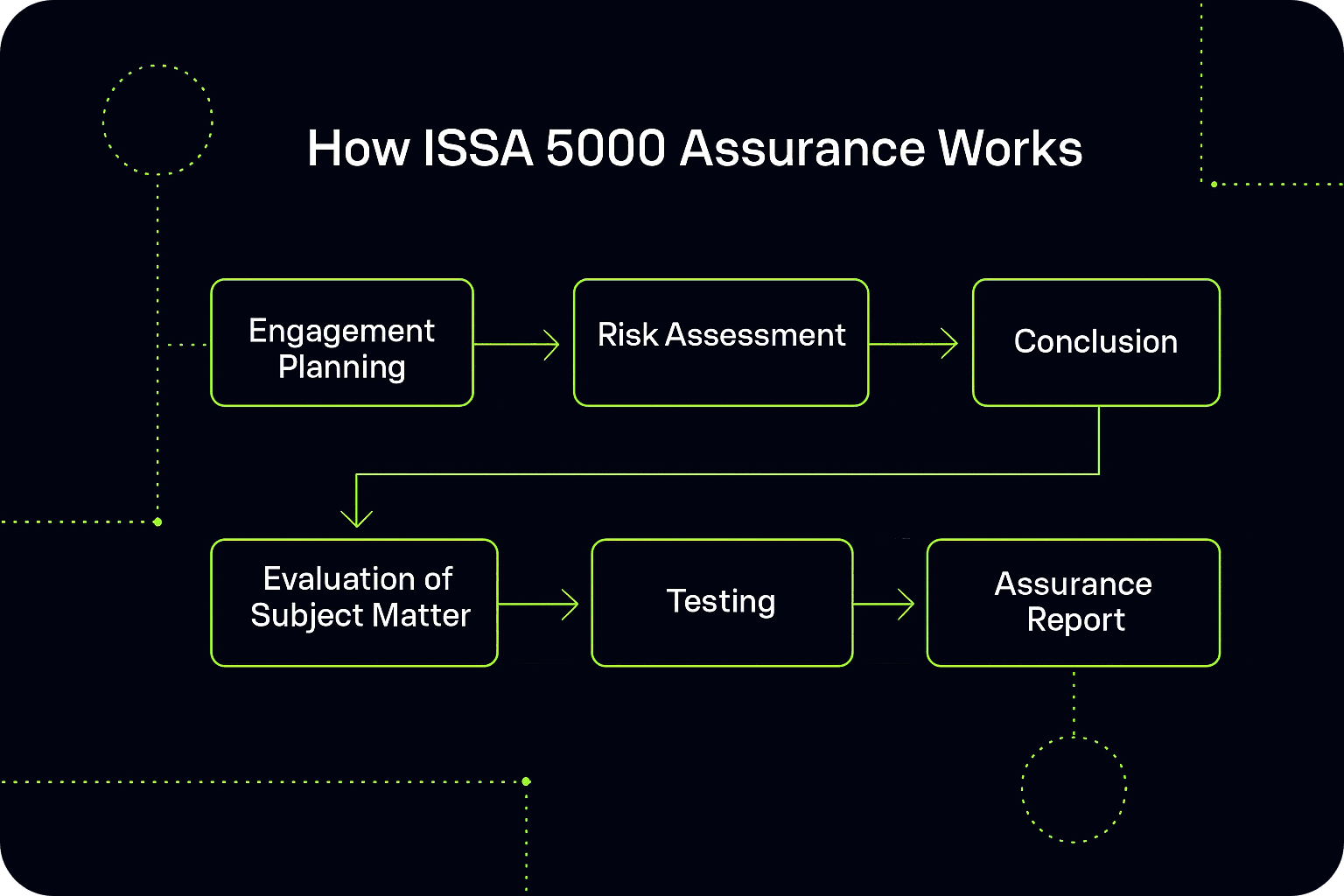

To meet assurance requirements under ISSA 5000, companies must demonstrate that their sustainability disclosures are based on credible, controlled, and consistently applied processes. Assurance engagements evaluate several key areas:

Firstly, auditors will assess the company’s internal controls and reporting processes supporting sustainability disclosures, ensuring that the processes for collecting and consolidating data are robust and documented.

Secondly, practitioners review the data management systems underpinning the reporting — including how data flows from operational sources through to disclosure outputs, and whether those systems enable traceability and completeness of reported metrics.

Another critical focus is the appropriateness of estimation methodologies. Many sustainability metrics, particularly Scope 3 emissions or climate scenario impacts, involve assumptions and estimates. Under ISSA 5000, companies must justify and document the methods used, ensuring consistency and transparency.

Consistency with recognised reporting frameworks — such as CSRD, ISSB IFRS S1 and S2, or UK SRS — is also a requirement. Auditors will verify that disclosures align to the relevant standards used in the sustainability report.

Finally, transparency regarding data gaps, proxy data, and assumptions is essential. ISSA 5000 expects companies to openly disclose where data is incomplete or estimated, and whether any proxies or industry averages have been used in place of primary data.

ISSA 5000 can be applied to a variety of reporting outputs. It can support the assurance of standalone sustainability reports, integrated within annual reports, or applied to specific sustainability disclosures embedded within regulatory filings. Regardless of the reporting format, the objective remains the same: to provide investors and stakeholders with confidence that the sustainability information disclosed is complete, accurate, and trustworthy.

In practical terms, ISSA 5000 establishes the audit roadmap for sustainability data — bringing non-financial disclosures under the same level of scrutiny as financial statements.

Why ISSA 5000 Matters for Finance and Audit Teams

Under regulations like CSRD, sustainability disclosures are now subject to assurance requirements:

Limited assurance today

Progressing towards reasonable assurance within 3–5 years.

For CFOs, controllers, and audit committees, this shift creates a new requirement: treat ESG data as assurable, investor-grade information. ISSA 5000 provides the standardised framework that auditors will use to:

Evaluate your company’s sustainability reporting controls.

Test the completeness and accuracy of disclosures.

Deliver an assurance conclusion – limited or reasonable.

In essence: ISSA 5000 puts sustainability reporting under the same audit lens as your financial statements.

What Is the Controls-First Approach to ESG Assurance?

In the context of sustainability reporting and assurance, neoeco’s Financially-Integrated Sustainability Management (FiSM) framework represents a shift away from reporting-focused tools towards a controls-first infrastructure. Unlike conventional ESG platforms — which treat disclosures as static end-products — FiSM is architected to treat emissions, ESG, and sustainability data as continuous operational processes governed by internal controls, audit trails, and structured workflows.

At the core of this approach is the neoeco Compliance Center: a centralized, finance-grade environment built to manage sustainability disclosures with the same rigour as financial reporting. Inspired by established financial controls frameworks and drawing parallels to leading compliance platforms like Vanta, the Compliance Center embeds assurance readiness directly into the reporting process.

Here’s how the controls-first model works in practice:

1. Controls, Not Checklists

Rather than retrofitting ESG data for audit at the end of the reporting cycle, neoeco’s platform continuously applies internal controls to data as it’s collected. Every data point — from emissions factors to supplier transactions — is processed through verification workflows that ensure completeness, accuracy, and traceability. These controls operate at the ledger level, mirroring financial reporting systems.

2. Continuous Audit Readiness

neoeco’s Compliance Center enforces real-time audit trails and control testing, ensuring that data is never siloed or static. Each transaction is automatically documented with immutable metadata: source, timestamp, and verification status. This allows sustainability data to be audit-ready by default — eliminating last-minute evidence gathering before assurance engagements.

3. Structured Around the FiSM Ledger

At the heart of the controls-first approach is the FiSM ledger — a hybrid, continuously updated system that integrates sustainability data into accounting workflows. Just as financial data is controlled and verified within ERP systems, sustainability data is subjected to the same principles of double-entry accounting, control testing, and reconciliation.

This foundation enables sustainability disclosures to meet assurance standards like ISSA 5000, ISAE 3000, and CSRD’s limited and reasonable assurance requirements — not as an afterthought, but as an integrated outcome of daily operations.

How Controls-Based ESG Reporting Works

Data Collection with Embedded Controls

Real-Time Audit Trails

Ledger-Level Data Structuring

Assurance-Ready Output

Continuous Monitoring and Updates

Limited vs. Reasonable Assurance Under ISSA 5000

Type of Assurance

Description

Best For

Limited Assurance

Negative assurance. Practitioner states nothing has come to their attention to indicate material misstatement. Lower level of evidence required.

Early-stage ESG reporters, Scope 3 reliance on estimates, disclosures in transition.

Reasonable Assurance

Positive assurance. Practitioner directly attests that disclosures are materially correct and free from misstatement. Higher level of scrutiny applied.

Mature reporters, high-risk industries, investor-sensitive sustainability disclosures.

neoeco's approach

Continuous, finance-led emissions and ESG data management via FiS ledger. Real-time traceability, transactional data capture, and documented controls ensure assurance readiness by design.

Companies preparing for limited or reasonable assurance under CSRD, ISSB, or UK SRS. Best for audit-focused CFOs, controllers, and sustainability teams seeking defensible, investor-grade disclosures.

neoeco’s Approach: Building Assurance-Ready ESG Infrastructure

At neoeco, we understand that preparing for ISSA 5000 assurance isn’t about adding another compliance checklist — it’s about transforming how sustainability data is managed.

Using our FiS ledger architecture:

Emissions and ESG data are captured at transactional level, with source traceability.

Data is structured in audit-ready format, aligned to financial reporting processes.

Controls, methodologies, and data lineage are documented natively.

Data systems are designed for both limited and reasonable assurance readiness.

For companies facing assurance under UK SRS, CSRD, ISSB, or ISO standards, neoeco provides the foundational infrastructure that allows both auditors and assurance practitioners to operate efficiently and effectively.

Why Accountants Lead in the ISSA 5000 Era

At its core, ISSA 5000 is an assurance standard — and its principles closely mirror those long established in financial audit. Concepts such as professional scepticism, controls testing, substantive analytical procedures, and sampling-based evidence evaluation are foundational to both financial and sustainability assurance engagements.

For this reason, accountants and audit professionals are naturally positioned to lead the transition toward assurance-ready sustainability reporting. CFOs, financial controllers, and internal audit leaders possess the expertise in governance, risk management, and controls oversight required to operationalise assurance standards like ISSA 5000. Just as they safeguard the integrity of financial disclosures, these professionals are now stepping forward to build credibility in non-financial reporting.

Within this new reporting paradigm, neoeco plays a critical role. Our platform enables organisations to realign responsibilities across sustainability reporting processes:

Accountants and finance teams take ownership of ESG and emissions data integrity — capturing, structuring, and verifying non-financial data with the same rigour applied to financial ledgers.

Sustainability teams retain responsibility for narrative and disclosure framing, ensuring strategic alignment and regulatory compliance.

The assurance process is no longer fragmented. neoeco integrates both functions, creating a unified, finance-led approach to sustainability reporting and assurance readiness.

In the ISSA 5000 era, audit readiness isn’t just about reporting — it’s about data governance. And accountants, more than anyone, understand what defensible, investor-grade reporting requires.

Prepare for ISSA 5000 with neoeco

Audit-ready sustainability reporting isn’t a future goal — it’s a 2025 requirement. neoeco’s finance-led platform ensures your ESG data meets the standard. neoeco represents a strategic shift:

Adaptable: Structured to evolve alongside regulations and data improvements.

Audit-Ready: Transaction-level data traceability built-in.

Financially Integrated: Emissions reporting aligned with financial reporting processes.

Composable: Open APIs for data ingestion from ERPs, supplier systems, and LCA tools.

In today’s regulatory environment, this flexibility isn’t optional — it’s essential.

Download our manifesto

And discover how to unify sustainability and finance — in one system, one ledger, and one source of truth.