ISSB Reporting: IFRS S1 & S2 (2025 Edition)

Stay ahead of sustainability disclosure mandates. neoeco transforms ISSB reporting into a finance-led advantage, from materiality to audit-ready reports.

Overview of ISSB, IFRS S1 & S2

Financially Material Focus

IFRS S1 & S2 Standards

TCFD-Aligned

Disclose in Financial Reports

Why ISSB Reporting Matters Now

ISSB has already been endorsed by IOSCO, the global body of securities regulators, and is seen as the new benchmark for capital market disclosures. It matters because:

Investors are demanding comparability across jurisdictions and industries.

Regulators are embedding ISSB into law, e.g., via UK SRS and CSRD interoperability

Firms want to avoid duplication with fragmented voluntary ESG frameworks

According to the IFRS Foundation's 2024 Jurisdictional Guide, global adoption is accelerating — with phased implementation and capacity-building underway in the UK, Australia, Japan, and Canada.

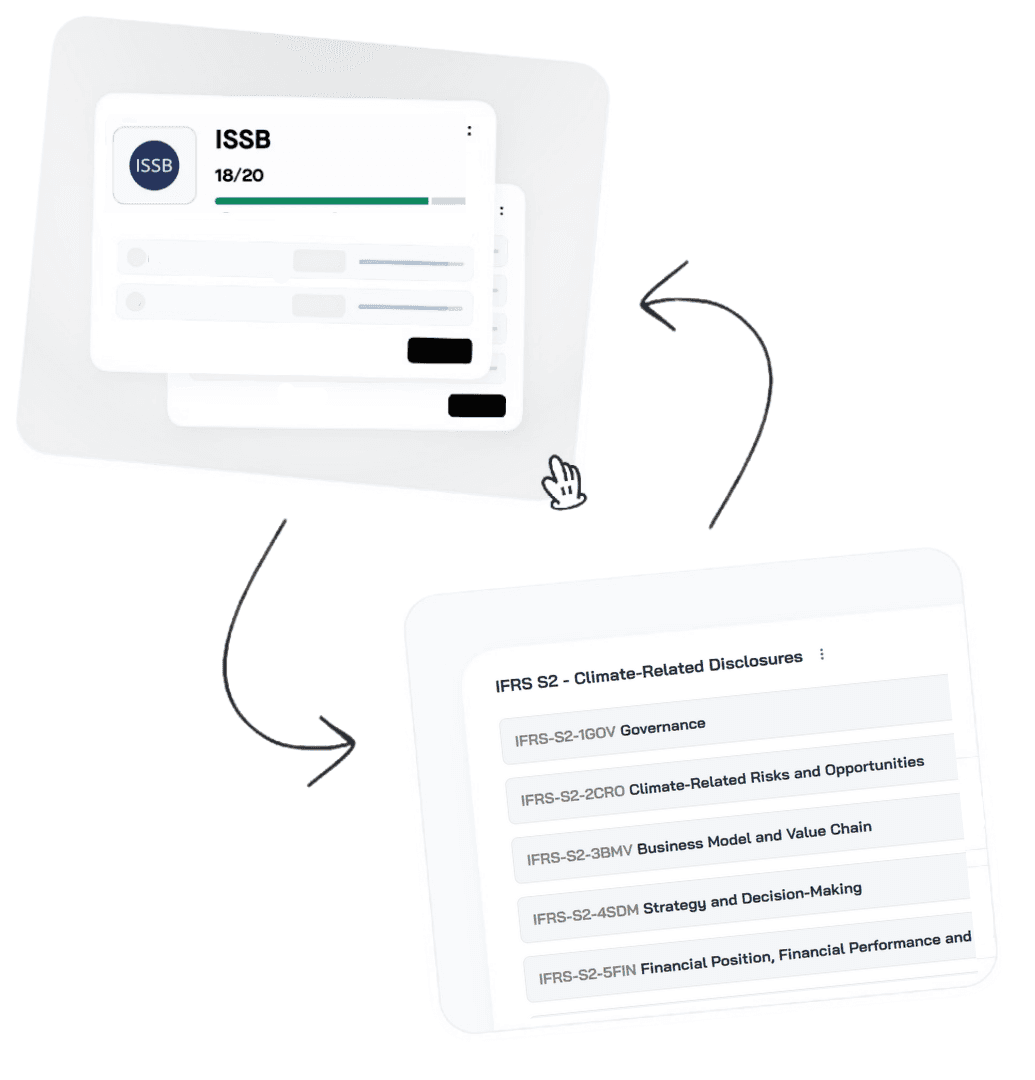

Key Components of ISSB Reporting

ISSB reporting is structured to bring clarity and consistency to sustainability disclosures by focusing on two core standards: IFRS S1 & S2.

These standards define what companies must report on to meet investor expectations around sustainability risks and opportunities. IFRS S1 provides a framework for disclosing general sustainability-related financial information, while IFRS S2 focuses specifically on climate-related disclosures.

Together, they form the foundation of ISSB’s global baseline, designed to integrate seamlessly with financial reporting and ensure decision-useful, comparable data across markets and industries.

IFRS S1: General Sustainability-related Financial Disclosures

IFRS S2: Climate-related Disclosures

What it’s for

Establishing a global framework for sustainability-related disclosures across industries

Providing detailed climate-related disclosures that help investors understand climate risks and opportunities

Who it applies to

Any company preparing general-purpose financial reports

Companies with material climate-related financial risks and opportunities

Core requirements

– Governance

– Strategy

– Risk management

– Metrics and targets

– Climate-related governance and strategy

– Scenario analysis

– Emissions disclosures (Scopes 1, 2, and 3)

– Climate risk integration

– Metrics and targets

How to Prepare

To prepare for ISSB reporting, CFOs, CSOs, and sustainability leaders should begin laying the foundation now. The shift to IFRS S1 and S2 standards requires more than a disclosure checklist — it demands cross-functional alignment, robust data systems, and board-level oversight. Whether reporting becomes mandatory in your jurisdiction in 2025 or 2026, taking these early steps will ensure your organisation is audit-ready, investor-aligned, and ahead of the regulatory curve.

Assess your current disclosures against IFRS S1 and S2.

Map data sources - especially for Scope 3 emissions

Build a cross-functional team involving finance, ESG, risk, and ops.

Plan early for assurance and audit-readiness.

Download your free ISSB checklist

Finance leaders, sustainability teams, and strategic operators navigating ISSB, CSRD, and the capital implications of ESG. If you're building sustainability reporting that holds up to audit and drives value — this is your playbook.