CSRD Compliance with Supply Chain LCA Tools

Nov 5, 2025

Explore how Life Cycle Assessment tools simplify compliance with the CSRD, ensuring accurate and reliable sustainability reporting across supply chains.

The Corporate Sustainability Reporting Directive (CSRD) is transforming how companies disclose sustainability data, requiring detailed reporting across entire supply chains. Starting in 2025, large organisations must report on 2024 data. By 2026, all qualifying large companies will follow, with international firms affected by 2028. The directive's double materiality principle demands companies assess both their supply chain's impact on the environment and society, and how sustainability factors affect their business.

Key Takeaways:

Mandatory Reporting: CSRD replaces voluntary frameworks with standardised, audited reporting.

Double Materiality: Companies must evaluate both financial and societal impacts.

Scope 3 Challenges: Up to 80% of emissions stem from supply chains, requiring detailed data collection.

LCA Tools: Life Cycle Assessment platforms simplify compliance by automating data collection, integrating with financial systems, and ensuring audit-ready reporting.

LCA tools are essential for meeting CSRD requirements, offering automated workflows, real-time data integration, and precise impact assessments. These platforms streamline supply chain reporting, making compliance efficient and reliable.

Building sustainable supply chains | Life cycle assessments

CSRD Supply Chain Reporting Requirements

The Corporate Sustainability Reporting Directive (CSRD) shifts sustainability reporting from a voluntary activity to a mandatory, standardised process, demanding transparency across entire value chains. This directive goes beyond traditional environmental reporting, introducing detailed obligations that reshape how organisations collect, verify, and disclose supply chain data.

Double Materiality in Supply Chains

At the core of CSRD's supply chain requirements is the double materiality principle. This framework requires organisations to assess two key dimensions: how their supply chain activities impact the environment and society (impact materiality), and how environmental and social factors influence their business operations and financial outcomes (financial materiality).

This dual approach adds layers of complexity to supply chain reporting. Companies must evaluate risks, impacts, and opportunities throughout their entire value chain. This includes immediate supplier relationships as well as downstream activities, such as product use and disposal at the end of its lifecycle.

A key task is identifying "impact hotspots" - areas in the supply chain where activities lead to significant environmental or social consequences. This involves collecting detailed data on supplier practices, resource usage, and social conditions. Additionally, companies need to assess how issues like climate risks, resource shortages, or social disruptions might affect both supply chain resilience and financial performance.

The double materiality assessment spans all ESG topics outlined in the European Sustainability Reporting Standards (ESRS). These include climate change, pollution, water and marine resources, biodiversity, resource use, workforce conditions, affected communities, consumer impacts, business conduct, and governance. For each area, companies must demonstrate how their supply chain both contributes to and is affected by these sustainability factors. Tools like Life Cycle Assessment (LCA) systems can help by streamlining data collection and analysis for these dual assessments.

Data Quality and Audit Standards

CSRD introduces strict requirements for audit-ready, digital sustainability data. All sustainability data must be submitted in a standardised digital format and subjected to limited third-party assurance.

Supply chain data must meet the ESRS criteria for completeness, reliability, and traceability. Each data point must be verifiable, accurate, and comparable across reporting periods and between organisations. This is especially challenging for Scope 3 emissions, which can account for up to 80% of a company’s environmental footprint and often stem from complex supplier networks.

To meet these audit requirements, companies need robust data governance systems. This includes clear documentation of data collection methods, supplier engagement processes, and calculation practices. For instance, integrating reporting frameworks like ISSB into financial strategies can help streamline compliance efforts. Learn more about ISSB reporting here.

Organisations are expected to make "reasonable efforts" to collect value chain data, even in areas where complete data isn’t yet available. They must document their efforts and outline plans for improvement. Over time, this creates a continuous expectation for better data quality and broader coverage.

Data must also be machine-readable and standardised to enable automated processing and easy comparison. For UK-based organisations operating in the EU, this presents additional challenges, as they must align with both UK and EU standards while managing complex international supply chains. Early adoption of integrated platforms that support multiple frameworks is critical for maintaining compliance and market access.

The audit process itself requires direct access for auditors to underlying data and supporting evidence. This means sustainability teams must maintain well-organised, secure repositories of all compliance-related files, supplier documentation, and calculation methodologies. The era of narrative-driven reporting with minimal documentation is over, replaced by detailed data trails designed to withstand external scrutiny.

Using LCA Tools for CSRD Compliance

Life Cycle Assessment (LCA) tools provide a structured, science-based way to tackle the European Union's Corporate Sustainability Reporting Directive (CSRD) requirements. These tools streamline what was once a fragmented and manual process, transforming sustainability data collection into an automated system that aligns with regulatory expectations and is audit-ready.

How LCA Methods Align with CSRD Requirements

LCA methodology, with its four distinct phases, offers a clear framework for meeting the CSRD's supply chain reporting standards. Each phase addresses both the technical and strategic demands of compliance.

Goal and scope definition: This phase helps organisations identify the most relevant activities and impacts within their supply chains, supporting the CSRD's focus on double materiality. It establishes clear boundaries for reporting and pinpoints sustainability topics requiring detailed analysis across the eleven Environmental, Social, and Governance (ESG) categories outlined in the European Sustainability Reporting Standards (ESRS).

Inventory analysis: This step lays the groundwork for comprehensive data collection, which is essential for achieving value chain transparency. By systematically capturing resource inputs, emissions, and other environmental factors, organisations can generate the detailed datasets needed for accurate Scope 3 emissions reporting.

Impact assessment: Here, the raw data collected is translated into measurable outcomes. Organisations can quantify their environmental and social impacts, including areas like climate change, pollution, water consumption, and biodiversity. This ensures that the data aligns with the CSRD's reporting requirements.

Interpretation: The final phase bridges technical findings with strategic decision-making. It ensures that LCA results are not only included in regulatory disclosures but also integrated into business strategies, highlighting how sustainability influences corporate decisions and supports continuous improvement.

Once this methodology is in place, integrating LCA tools into existing systems makes compliance even more efficient.

Automated Data Collection and System Integration

Modern LCA tools eliminate the inefficiencies of manual reporting methods, automating the collection and standardisation of supplier data while ensuring traceability. These capabilities are essential for meeting the CSRD's external assurance requirements.

Real-time data synchronisation is a game-changer. By integrating with ERP systems, procurement platforms, and finance software via APIs, LCA tools enable seamless data flows. This ensures that financial transactions are directly linked to sustainability metrics, reducing inconsistencies and supporting the CSRD's requirement for financially integrated sustainability reporting.

A great example of this is Aasted, a Danish manufacturer that utilised Normative's LCA tool in 2023 to prepare for CSRD compliance. By automating Scope 3 calculations and integrating supplier data, Aasted achieved audit-ready reports with improved accuracy and efficiency.

Supplier engagement is another strength of advanced LCA platforms. These tools automatically send data collection requests to suppliers, track response rates, and validate submissions against industry benchmarks. This systematic approach ensures organisations make "reasonable efforts" to gather value chain data while building robust audit trails.

Platforms like neoeco exemplify this integrated approach. By unifying financial and sustainability data, these tools provide real-time, detailed insights across ESG impact categories. Their AI-driven automation and LCA methodologies not only support CSRD compliance but also aid CFOs and sustainability teams in making informed strategic decisions. Learn how ISSB reporting fits into a financially integrated strategy for more context on regulatory compliance.

LCA Tools vs Manual Reporting Methods

The limitations of manual reporting methods become glaring when compared to the capabilities of LCA tools, especially under the CSRD's rigorous requirements for data quality, auditability, and comprehensive coverage. Here's a side-by-side comparison:

Aspect | LCA Tools | Manual Methods |

|---|---|---|

Data Collection | Automated, real-time supplier integration | Spreadsheets and email requests |

Accuracy & Consistency | Standardised methods, built-in validation | Error-prone, lacks consistency |

Audit Trail | Complete digital documentation and version control | Scattered files, hard-to-trace sources |

Scope 3 Coverage | Comprehensive mapping of the value chain | Limited coverage, with data gaps |

Time Investment | Initial setup, minimal ongoing effort | Labour-intensive throughout the cycle |

Compliance Risk | Built-in CSRD alignment, automated updates | High risk of errors and missed standards |

Cost Structure | Higher upfront cost, lower operational expenses | Low initial cost, but high ongoing labour costs |

Automated LCA tools excel in areas like validation, standardisation, and error checking, ensuring that sustainability data meets the CSRD's strict requirements for reliability and traceability. In contrast, manual methods often struggle to maintain consistency, especially across complex supply chains.

Scalability is another critical factor. As CSRD requirements expand, LCA tools can easily adapt to larger supplier networks, new reporting frameworks, and evolving regulations. Manual methods, however, become increasingly cumbersome, leading to incomplete reporting and higher compliance risks as organisations grow. This scalability makes LCA tools a forward-thinking choice for businesses preparing for the future of sustainability reporting.

Choosing and Setting Up Supply Chain LCA Tools

After understanding the advantages of Life Cycle Assessment (LCA) tools for CSRD compliance, the next step is selecting and implementing the right one. Picking the right tool is crucial to ensure smooth data integration and audit readiness. A misstep here could lead to compliance issues, poor data quality, and delays that might jeopardise your reporting deadlines.

Key Features to Look For in LCA Tools

When choosing an LCA tool, there are several essential features to consider:

CSRD and ESRS compatibility: The tool must align with the European Sustainability Reporting Standards (ESRS). This ensures it can handle reporting across critical ESG areas such as climate change, pollution, biodiversity, and workforce-related metrics. Without this alignment, your reports may not meet regulatory standards.

Double materiality assessment: The tool should evaluate both how your organisation impacts the environment and society (impact materiality) and how sustainability issues affect your business (financial materiality). This dual perspective is a core requirement under CSRD, and manual methods won't suffice.

Automated data collection and validation: Advanced LCA tools streamline data collection by automating supplier requests, tracking responses, and validating submissions against industry benchmarks. These features are essential for producing audit-ready reports.

System integration capabilities: A good LCA tool should integrate seamlessly with your existing systems. Look for compatibility with ERP platforms like SAP or Business Central, accounting software such as Xero, Sage, or QuickBooks, and procurement systems via APIs.

Audit-ready reporting: The tool must generate detailed reports with clear documentation of data sources, calculations, and assumptions. This transparency is vital for external auditors to verify your disclosures.

Steps to Implement an LCA Tool

Implementing an LCA tool requires a structured approach to ensure success:

Define reporting boundaries: Start by mapping your value chain and categorising suppliers based on spend, impact, and data availability. Prioritise collecting data from key suppliers, particularly in areas where most of your environmental impact occurs. Use existing data sources like financial systems and procurement records as a foundation.

Integrate the tool with your systems: Begin by connecting the LCA tool to financial systems to establish automated data flows. Match financial transactions with sustainability metrics, and test the integration thoroughly before expanding to other systems.

Automate data collection and validation: Set up workflows for engaging suppliers, using automated templates and clear deadlines. Implement validation rules to ensure data quality and create supplier portals to simplify the submission process.

Train your team and suppliers: Provide guidance on data requirements, collection protocols, and submission processes. Conduct training sessions to ensure everyone understands what’s expected.

Generate and review reports: Regularly test CSRD-compliant reports to identify any data gaps or errors. Involve finance, sustainability, and legal teams in reviewing these reports to ensure accuracy. Document all methodologies, assumptions, and data sources for audit purposes.

By following these steps, you can implement an LCA tool that ensures compliance and supports efficient reporting.

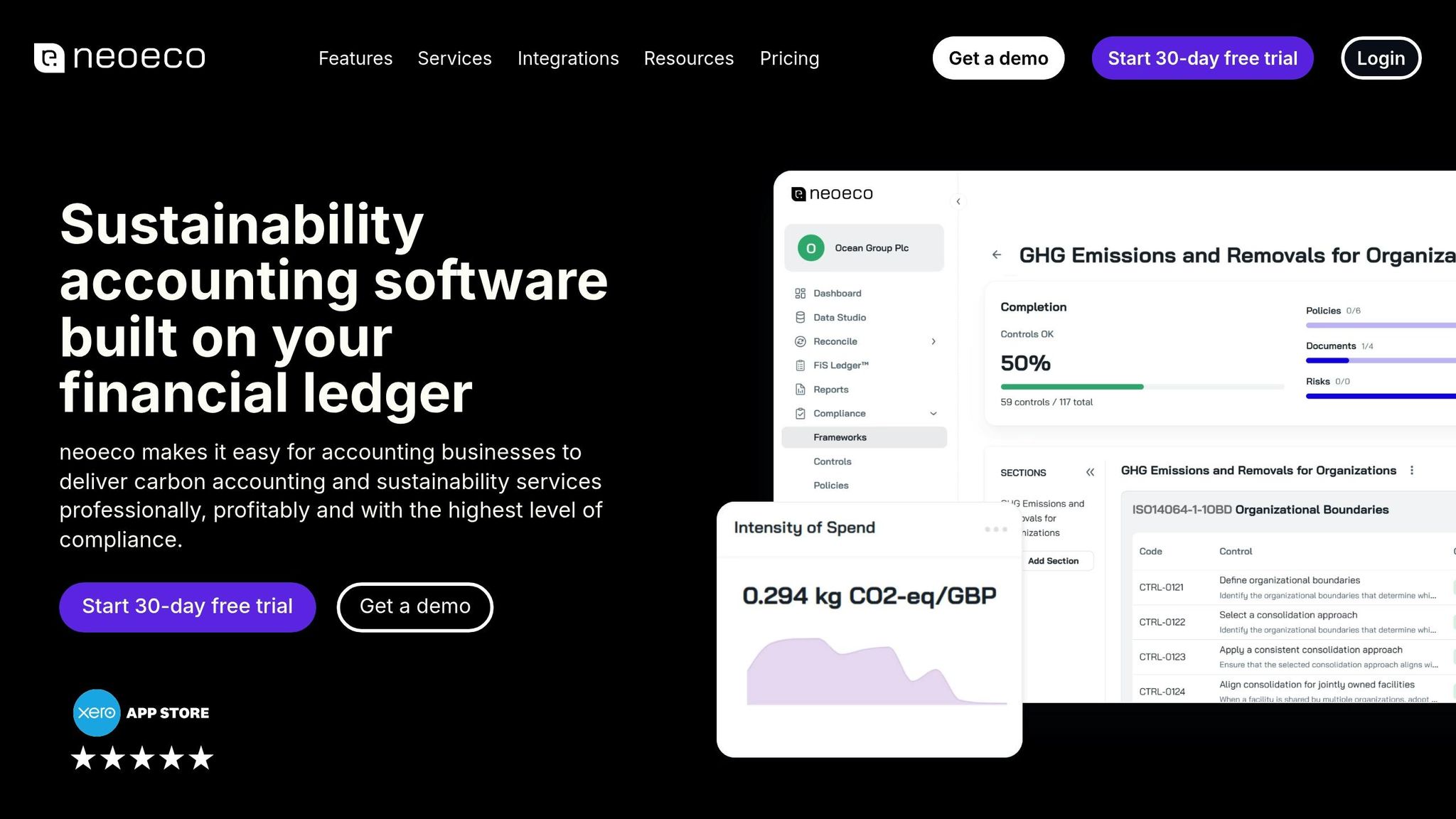

neoeco: A Modern Sustainability Platform

neoeco is a next-gen LCA tool designed specifically for CSRD compliance. It combines financial and sustainability data using AI-driven automation and ISO-compliant methodologies, offering detailed, real-time insights across all ESG impact areas required by CSRD.

What sets neoeco apart?

Direct financial system integration: neoeco connects seamlessly with accounting software like Xero, Sage, QuickBooks, Business Central, and SAP. This integration builds sustainability data directly from financial transactions, eliminating the need for separate data collection systems while ensuring audit-grade accuracy.

Multi-framework compliance: In addition to CSRD and ESRS, neoeco supports frameworks such as ISSB (IFRS S1 & S2), GHGP, TCFD, SBTi, SASB, CDP, and GRI. This flexibility ensures you're prepared for evolving regulations without needing additional tools.

Audit-ready controls: With features like evidence hubs, progress tracking, and streamlined auditor access, neoeco simplifies the audit process and keeps compliance documentation well-organised.

For organisations aiming to manage Scope 3 emissions in real-time, neoeco provides the detailed value chain visibility needed for CSRD reporting. Its modular design and annual licensing model make it a scalable solution tailored to your organisation's sustainability goals.

Summary: Meeting CSRD Requirements with LCA Tools

LCA tools are transforming sustainability reporting by replacing manual, error-prone processes with automated, audit-ready systems that align with the stringent demands of the CSRD. Despite this, only 22% of companies are fully prepared to meet compliance requirements.

These tools provide a solid technical framework for systematically measuring and reporting environmental, social, and governance (ESG) impacts across an organisation's entire value chain. Considering that up to 80% of a company's environmental footprint comes from its value chain - particularly suppliers and downstream product usage - automated solutions are crucial for capturing this data accurately.

A key aspect of CSRD compliance is integrating financial and sustainability data. The directive requires companies to publish both types of information together in management reports, which must undergo third-party assurance. Platforms that merge financial and ESG data - based on financially-integrated sustainability management principles - are invaluable for meeting this requirement, supporting the unified approach previously highlighted.

Aasted’s successful preparation for the CSRD using an LCA platform illustrates how standardising data and aligning Scope 3 emissions reporting can greatly simplify supply chain transparency.

LCA tools also play a pivotal role in addressing CSRD's double materiality requirement. They allow organisations to evaluate not only the financial implications of sustainability issues on their business but also their broader impact on people and the environment. Manual methods cannot deliver the detailed, real-time insights needed for such comprehensive assessments. Automated tools, on the other hand, ensure consistent and traceable reporting processes.

For organisations aiming to manage Scope 3 emissions in real time, these platforms provide the visibility required to comply with CSRD standards. They standardise the collection and reporting of data, ensuring accuracy and traceability while supporting the submission of digital reports mandated by the directive. This capability strengthens the audit-ready digital reporting discussed earlier.

The shift towards automated systems reflects a wider industry trend. With thousands of companies expected to adopt these technologies between 2025 and 2028, investing in reliable LCA platforms now not only ensures compliance today but also prepares organisations for future challenges.

FAQs

How can businesses identify and address key environmental and social risks in their supply chains to meet the CSRD's double materiality requirements?

Life Cycle Assessment (LCA) tools offer businesses a way to identify key areas of concern - often called 'impact hotspots' - within their supply chains. By assessing the entire lifecycle of products and services, these tools shed light on critical issues like carbon emissions, resource consumption, and social inequalities.

Platforms such as neoeco simplify this process by combining LCA techniques with financial and sustainability data. This empowers organisations to pinpoint these hotspots and take meaningful actions to address them. It also helps ensure alignment with the CSRD's double materiality framework while supporting ESG reporting that's ready for audits.

What challenges might organisations face when using Life Cycle Assessment (LCA) tools to align supply chain data with CSRD requirements?

Integrating Life Cycle Assessment (LCA) tools with financial systems to meet CSRD requirements can be a tricky process. Companies often grapple with issues like maintaining consistent data across financial and sustainability platforms, handling detailed supply chain information, and ensuring reporting formats align with CSRD standards.

To tackle these challenges, it's important to adopt tools that merge financial and sustainability data effortlessly. For instance, platforms like neoeco leverage AI-powered automation alongside LCA methodologies to streamline the process. These tools can deliver real-time insights and produce audit-ready ESG disclosures, helping organisations stay compliant with CSRD while cutting down on manual work and improving data accuracy.

How do Life Cycle Assessment (LCA) tools improve the accuracy and reliability of sustainability data for compliance reporting?

Life Cycle Assessment (LCA) tools improve precision and dependability by automating data collection and using activity-based calculations. This approach reduces the chances of human error and ensures uniformity when measuring sustainability metrics.

Modern platforms like neoeco take it a step further by using AI to address Scope 3 emissions, offering detailed and up-to-the-minute insights. These features not only help businesses align with frameworks like CSRD but also make supply chain sustainability reporting audit-ready.