ISO 14064 for Transport Emissions

Dec 7, 2025

Practical guide to using ISO 14064 to measure, verify and reduce transport emissions while aligning with SECR/UK SRS and financial systems for audit-ready reporting.

ISO 14064 provides a globally recognised framework for tracking and reporting greenhouse gas emissions, particularly in the transport sector. It aligns with UK reporting requirements like SECR and the UK SRS, helping organisations measure emissions from company vehicles, logistics, and business travel. The standard is divided into three parts: creating emissions inventories (14064-1), quantifying reductions (14064-2), and verifying data (14064-3). Accurate reporting requires clear boundaries, reliable data, and correct emission factors.

Key points:

Scopes: Emissions are categorised into Scope 1 (direct), Scope 2 (indirect energy use), and Scope 3 (value chain activities).

Data sources: Fuel receipts, telematics, invoices, and expense claims are critical for calculations.

UK compliance: ISO 14064 supports SECR and UK SRS reporting.

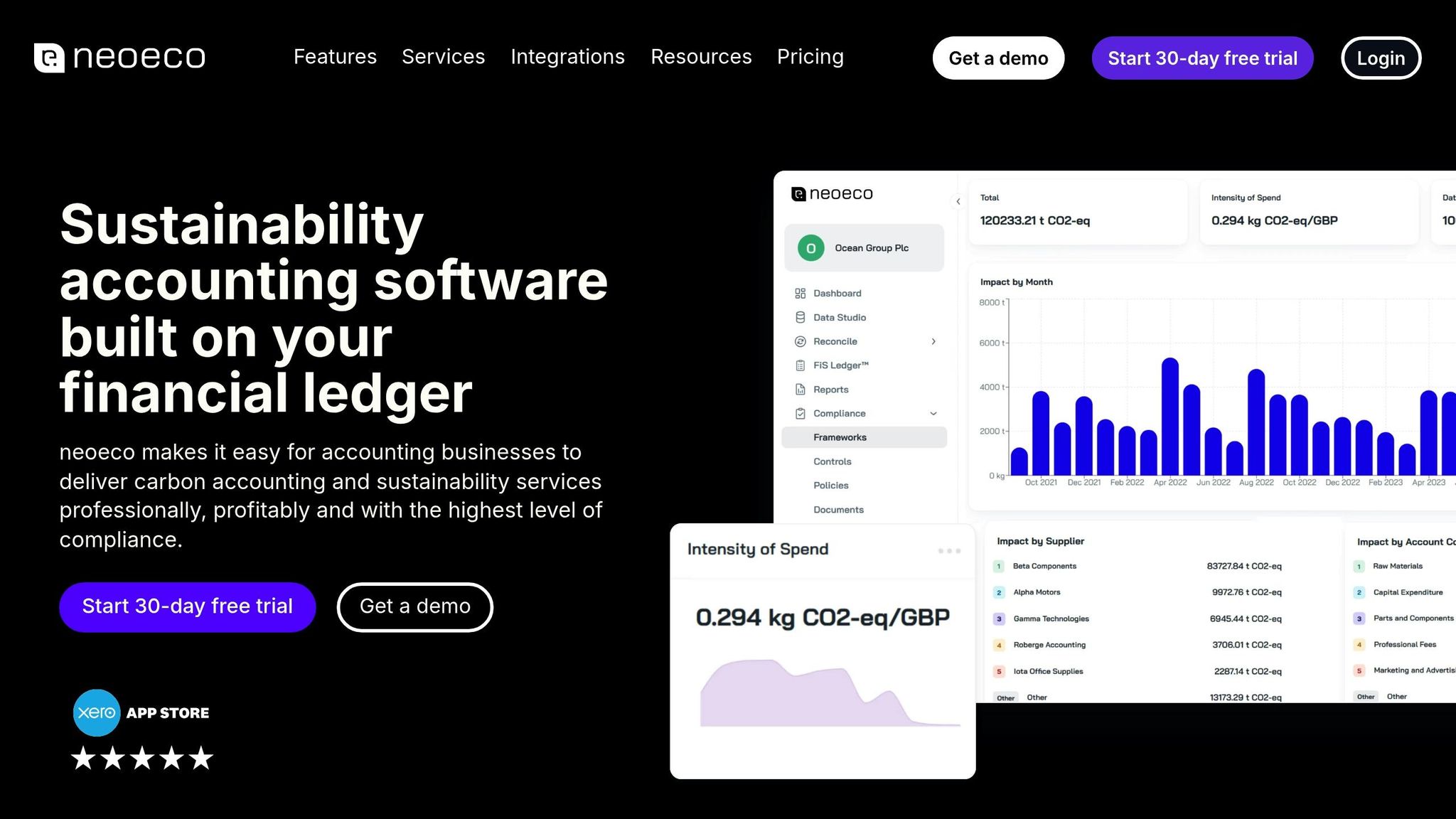

Tools: Platforms like neoeco integrate financial and emissions data, simplifying calculations and ensuring audit readiness.

This framework helps organisations track emissions, verify data, and implement reduction projects, such as fleet electrification or route optimisation, while maintaining compliance with UK regulations.

ISO 14064 Explained: The Ultimate Guide to Measuring Your Carbon Footprint

How ISO 14064 Defines Transport Emissions

ISO 14064 provides a structure for monitoring transportation emissions, encouraging organisations to consider all relevant activities when assessing their environmental impact. While it doesn’t enforce a fixed classification for transport emissions, it emphasises the importance of a thorough and inclusive approach.

Transport Emissions in Scope 1, 2, and 3

Transport emissions are categorised under the following scopes:

Scope 1 (Direct emissions): These come from transport activities directly controlled by the organisation, such as company-owned vehicles.

Scope 2 (Indirect emissions): This includes emissions from energy usage, like the electricity used to charge electric vehicles.

Scope 3 (Other indirect emissions): These cover transport-related activities within the organisation's value chain, such as third-party logistics or employee commuting.

The application of these scopes should align with the organisation's operations and be carefully structured to prevent overlaps in reporting.

Defining these scopes clearly is essential for setting precise boundaries, which we’ll explore further below.

Organisational Boundaries vs Operational Boundaries

ISO 14064 requires organisations to establish clear organisational and operational boundaries. This clarity ensures emissions are attributed correctly and eliminates the risk of double counting. By defining these boundaries properly, organisations can maintain accurate and reliable reporting.

Common Transport Emission Sources

To address transport emissions effectively, organisations need to identify major sources, such as:

Road freight and delivery services.

Business travel across various modes of transport.

Goods or passenger movement via air, rail, or maritime routes.

Employee commuting habits.

Collecting relevant data - like fuel consumption or distances travelled - is crucial. Organisations then apply appropriate emission factors to calculate their impact for each category.

Tools like neoeco can simplify this process by connecting financial transactions directly to emissions data. This integrated approach allows accounting firms to map transport-related expenses to recognised emissions categories, ensuring alignment with ISO 14064 and other frameworks.

In the next section, we’ll explore how these definitions inform the creation of a transport emissions inventory.

Creating a Transport Emissions Inventory Under ISO 14064

Following the guidelines of ISO 14064, a well-organised inventory is key to accurate transport emissions reporting. Developing this inventory involves setting clear boundaries, collecting reliable activity data, and applying consistent calculation methods.

Setting Boundaries for Transport Emissions

When it comes to transport activities, the first step is deciding what operations fall within your reporting scope.

Organisational boundaries define which entities you’ll include. If your organisation operates across multiple subsidiaries or joint ventures, you’ll need to decide on an approach - whether it’s equity share, financial control, or operational control - to determine how shared transport assets or outsourced logistics are accounted for.

Operational boundaries focus on which transport activities to measure. This distinction becomes essential when balancing in-house operations with outsourced services. For example, if you manage your own delivery fleet but also use third-party couriers, you’ll need to categorise these activities under different scopes. Consistently documenting these boundaries across reporting periods avoids confusion, gaps, or double counting. In complex supply chains, where you might oversee a warehouse but not the vehicles collecting goods, creating a visual map of the transport chain can clarify where your responsibilities begin and end.

Once boundaries are established, the next steps involve gathering precise activity data and selecting the right emission factors.

Gathering Activity Data and Emission Factors

Transport-related data typically includes fuel consumption, mileage records, freight weights, and distances travelled. It’s important to collect this information consistently across all transport modes and providers.

Direct data sources - like fuel receipts, telematics systems, and vehicle management software - are the most reliable. For company-owned vehicles, operational systems often provide this data, though accessing it efficiently can be a hurdle.

When direct data isn’t available, spend-based data can serve as an alternative. This method uses financial transactions - such as fuel purchases, courier invoices, or freight bills - to estimate emissions. It’s particularly useful for Scope 3 transport emissions, where supplier data might be harder to obtain.

Sustainability accounting software can make the data collection process easier by integrating with financial systems. Many platforms also offer tools for uploading files, cleaning data, and aligning with reporting frameworks like the GHG Protocol, SECR, and UK SRS standards.

Emission factors are used to convert activity data into carbon dioxide equivalent (CO₂e) emissions. The UK Government provides annual emission factors for various transport modes, fuel types, and vehicle classes. Selecting the right factor is critical; for instance, a diesel van will have a different rate compared to a petrol car, and factors can also vary by vehicle size. Always aim to match your activity data with the most specific factor available.

Calculating Emissions by Transport Category

With your data and emission factors ready, you can calculate emissions for each transport category. This involves multiplying activity data by the corresponding emission factors.

Owned vehicles (Scope 1): For example, if your fleet consumed 5,000 litres of diesel, multiply this by the relevant emission factor from the UK Government guidelines to calculate total emissions. Keeping records by vehicle type and fuel grade ensures accurate results.

Subcontracted logistics (Scope 3): When detailed fuel data isn’t available, you can use spend-based emission factors to estimate emissions based on invoice information. This ensures you account for significant Scope 3 sources.

Business travel: Emissions from rail travel, flights, hire cars, and other modes require separate calculations using mode-specific factors. Since this data is often stored in expense systems rather than operational databases, linking these systems or scheduling regular data exports is essential to avoid missing information.

For organisations working with multiple clients, tools like neoeco offer centralised dashboards for real-time emissions tracking.

To ensure your calculations are reliable, incorporate audit-readiness from the start. Using audited financial data as the foundation for your inventory improves accuracy. Document your methodology, retain source data, and maintain a clear audit trail connecting raw activity data to final emissions figures. Systems with built-in audit controls can track completed tasks, flag missing details, and indicate items ready for review through checklists. These systems also allow auditors controlled access to reports and evidence, reducing the need for back-and-forth emails.

During the calculation process, you may encounter unexpected challenges, such as missing data or unclear categorisation. Address these issues systematically to ensure your emissions reporting remains consistent over time and aligns with ISO 14064 standards.

Verification and Emission Reduction Projects Under ISO 14064

Once your emissions inventory is complete, the next steps are to verify its accuracy and start implementing decarbonisation initiatives. ISO 14064 provides a clear framework for both verifying data and managing emission reduction projects. Let’s delve into how ISO 14064-3 and ISO 14064-2 enhance these processes.

Verification Under ISO 14064-3

ISO 14064-3 outlines the principles for verifying greenhouse gas inventories, including emissions from transport. This standard ensures that your reported data is accurate, thorough, and consistent with established methodologies.

Third-party verification plays a key role here. When your emissions data is reviewed by clients, investors, or regulators, independent verification demonstrates that your figures meet recognised standards. This is especially important in transport, where data often comes from a mix of sources, such as fuel receipts, telematics systems, courier invoices, and expense claims.

The verification process involves an independent auditor evaluating your emissions inventory against the requirements of ISO 14064-1. They will scrutinise key elements like boundary definitions, data sources, and calculation methods to ensure the quality of your reported data.

To support verification, it’s crucial to maintain clear documentation that links data sources, emission factors, and calculations. For example, if your inventory includes data from fuel card transactions, freight invoices, and business travel expenses, the connections between these sources and the final emissions figures must be transparent and traceable.

Platforms such as neoeco simplify this process by integrating financial data with emissions controls. This integration reduces the need for manual reconciliation and speeds up verification. Auditors can access reports and evidence directly, eliminating the need for lengthy back-and-forth communication via email.

Verification not only ensures data accuracy but can also identify areas for improving data collection, enhancing the reliability of your inventory over time.

Applying ISO 14064-2 to Transport Decarbonisation Projects

Once your data is verified, ISO 14064-2 provides guidance for managing and quantifying emission reduction projects. Building on your verified emissions inventory, this standard helps you measure and report the impact of specific decarbonisation initiatives.

While ISO 14064-1 focuses on measuring emissions and ISO 14064-3 ensures verification, ISO 14064-2 is all about quantifying, monitoring, and reporting on reductions achieved through targeted projects. This is particularly useful for transport-related decarbonisation efforts.

Project-level accounting under ISO 14064-2 starts with establishing a baseline - essentially, what your emissions would have been without any intervention. Actual emissions are then measured after implementing changes, and the difference represents the reduction. This calculation must follow consistent methods and be verified to ensure the reductions are genuine.

Examples of transport decarbonisation projects include fleet electrification, route optimisation, shipment consolidation, or switching to rail transport. Each project requires a carefully defined baseline and ongoing monitoring to demonstrate measurable reductions.

For instance, replacing diesel vans with electric vehicles involves setting a diesel baseline and comparing it to the emissions reductions achieved through electric charging, adjusted for UK grid factors. Similarly, route optimisation might use historical fuel consumption or mileage data as a baseline. After implementing new routing measures, tracking actual fuel use or distance travelled can help quantify the savings, though factors like traffic patterns and seasonal variations must also be considered.

ISO 14064-2 stresses the importance of continuous monitoring and reporting. For transport projects, this could involve regular fuel consumption reports, mileage summaries, or even real-time telematics data to track performance.

If you’re managing multiple decarbonisation projects across different transport categories, keeping organised records is crucial. Finance-integrated systems can automatically track emissions reductions alongside the financial costs of these initiatives. This makes it easier to evaluate return on investment and prioritise future projects. Such an approach aligns with the principles of financially-integrated sustainability management, where emissions and financial data are managed together rather than in isolation.

Verification of emission reductions follows the same principles as inventory verification under ISO 14064-3, but with an added emphasis on proving that reductions are genuine and permanent. This structured method allows organisations to communicate their decarbonisation achievements with confidence, presenting verified reductions from specific projects to build trust with stakeholders.

Connecting ISO 14064 Transport Emissions with Financial Systems and UK Reporting Requirements

Transport emissions are closely tied to financial transactions like fuel purchases and invoices. Bridging these two data streams is crucial for accurate reporting and meeting UK regulations.

UK Reporting Requirements for Transport Emissions

The UK has introduced both mandatory and voluntary frameworks for organisations to report greenhouse gas emissions, including those from transport. ISO 14064 provides a framework that aligns well with these standards.

Streamlined Energy and Carbon Reporting (SECR) applies to UK-incorporated quoted companies, large unquoted companies, and large limited liability partnerships. Under SECR, organisations must disclose their UK energy use and associated greenhouse gas emissions, covering transport-related emissions from company vehicles and business travel. Reporting of Scope 1 and Scope 2 emissions is mandatory, while Scope 3 emissions are encouraged if they are significant.

ISO 14064-1 offers a clear methodology that fits SECR requirements, covering boundary setting, data collection, and emission calculations. By using ISO 14064 principles, organisations can ensure their transport emissions data meets the standards expected by UK regulators, making SECR reporting more straightforward.

UK Sustainability Reporting Standard (UK SRS), launched in 2024, takes a broader approach. While SECR focuses on energy and carbon, UK SRS requires more detailed climate-related disclosures across the value chain. For transport emissions, this includes a detailed breakdown by source, explanations of methodologies, and links to business activities. Using recognised frameworks like ISO 14064 ensures consistency and comparability in these disclosures.

ISO 14064's structured approach is well-suited to these UK frameworks. Now, let’s see how integrated financial systems simplify compliance.

Finance-Integrated Emissions Reporting with neoeco

Understanding the frameworks is one thing; connecting financial data to carbon reporting is another. Many organisations struggle with linking financial transactions to emissions data. Transport emissions calculations depend on activity data already present in financial systems - for example, fuel purchases recorded on petrol cards, logistics invoices, taxi receipts, and vehicle lease payments. Extracting this information manually, categorising it, applying emission factors, and maintaining audit trails can be tedious and prone to errors.

neoeco solves this problem by integrating directly with financial systems like Xero, Sage, and QuickBooks. The platform automatically maps transactions to recognised emissions categories under GHGP, ISO 14064, and UK frameworks like SECR and UK SRS. This eliminates manual data entry, ensuring emissions reporting is based on accurate financial data.

For transport emissions, the system links fuel card transactions to Scope 1, EV charging costs to Scope 2, and logistics expenses to Scope 3. It applies the correct emission factors based on transaction type, fuel source, and vehicle category, streamlining the reporting process.

This integrated approach aligns with the principles of Financially-integrated Sustainability Management (FiSM), combining emissions and financial data into one system. For transport, this means organisations can monitor both the carbon impact of logistics operations and the financial costs, enabling better decisions around decarbonisation investments.

neoeco’s compliance engine formats outputs for SECR and UK SRS, allowing you to focus on analysis and reduction strategies rather than formatting data.

"One system for all rules: neoeco keeps up with GHGP, SECR and UK SRS, and more so you never have to learn new frameworks."

Built-in audit controls ensure traceable links between data sources, emission factors, and calculations, making ISO 14064-3 verification straightforward. The platform’s evidence hub securely stores supporting documentation, making it easy to provide data when required.

"Audit-ready controls: Track what's done, what's missing, and what's ready for review in one simple checklist."

For accounting firms managing multiple clients, this approach offers clear benefits. You can handle all client sustainability data from one dashboard, ensuring consistent methodologies while tailoring reports to individual needs. Whether your client is in logistics or professional services, the data collection and calculation processes remain consistent.

The platform’s smart transaction mapping links ledger entries to Scope 1, 2, and 3 categories using GHGP and ISO 14064 methodologies. This automation reduces the time needed to create transport emissions inventories, allowing firms to offer carbon accounting services efficiently without requiring specialist sustainability expertise.

neoeco also generates professional, branded reports with clear visualisations, showing emissions by transport category, trends over time, and progress towards reduction targets. For organisations working on transport decarbonisation under ISO 14064-2, the platform tracks emissions reductions alongside costs and savings, demonstrating the return on investment for each initiative.

Finally, neoeco’s compliance with SOC 2 and GDPR ensures that client financial and emissions data is secure and meets the data governance standards required by UK regulators and professional bodies.

Conclusion

ISO 14064 offers a clear, internationally recognised framework for measuring, reporting, and verifying transport emissions. It covers all aspects of transport-related greenhouse gases, from company-owned vehicles and business travel to the complexities of supply chain logistics. By setting clear boundaries, using consistent calculation methods, and supporting independent verification, the standard helps organisations create reliable emissions inventories that meet both voluntary and regulatory requirements.

For UK organisations, ISO 14064 aligns closely with mandatory frameworks like SECR and the upcoming UK SRS. Its principles - such as boundary setting, data collection, and applying emission factors - translate seamlessly into compliance-ready reporting. This alignment not only reduces duplication of effort but also ensures transport emissions data meets the expectations of regulators, investors, and other stakeholders. Importantly, it highlights the growing need for better integration between financial data and emissions reporting.

The main challenge lies in linking financial transactions to accurate emissions calculations. Transport emissions rely on data already present in financial systems, such as fuel purchases, logistics invoices, vehicle leases, and travel expenses. Finance-integrated tools like neoeco simplify this process by directly connecting financial data from platforms like Xero, Sage, and QuickBooks to emissions metrics. The platform automatically maps transactions to ISO 14064 categories - fuel card purchases align with Scope 1, EV charging costs with Scope 2, and freight invoices with Scope 3 - eliminating the need for manual input. This results in quicker, more precise emissions inventories.

"We evaluated multiple ESG tools and felt more confused each time. neoeco cut through the noise - the only platform that connects financials to sustainability with LCA-level accuracy."

For accounting firms, this approach presents opportunities to expand their services without requiring deep sustainability expertise. Audit-ready controls and evidence storage meet ISO 14064-3 verification standards, while real-time dashboards help track progress towards emissions reduction targets. Additionally, transport decarbonisation projects aligned with ISO 14064-2 benefit from tracking emissions reductions alongside financial costs and savings, making it easier to demonstrate the return on investment for each initiative.

As UK reporting requirements continue to evolve, organisations that integrate ISO 14064 standards with financial data gain a significant advantage. This combination simplifies compliance, delivers robust emissions data, and supports actionable sustainability strategies, ensuring businesses stay ahead in a rapidly changing regulatory landscape.

FAQs

How does ISO 14064 support compliance with UK regulations like SECR and UK SRS for transport emissions?

ISO 14064 offers a structured approach to measuring and managing greenhouse gas emissions, helping organisations carry out life cycle emission analyses more effectively. This framework is especially helpful for meeting UK-specific reporting obligations like SECR (Streamlined Energy and Carbon Reporting) and UK SRS (Sustainability Reporting Standards).

With tools like neoeco, the process becomes even more straightforward by automating the mapping of transactions to recognised emissions categories outlined by ISO 14064, SECR, and UK SRS. This automation delivers precise, finance-grade carbon data and generates audit-ready reports - eliminating the hassle of manual calculations or spreadsheet errors.

What challenges do organisations face when linking financial data to emissions calculations under ISO 14064?

Organisations often face hurdles when trying to align financial data with emissions calculations under ISO 14064. One major challenge is linking financial transactions to the correct emissions categories. This task demands a deep understanding of both financial systems and carbon accounting principles. Errors in categorisation can result in emissions reports that are either incomplete or inaccurate.

Another significant obstacle is the manual effort involved in processing data. Transforming financial records into emissions data can be a time-consuming and error-prone exercise, particularly for organisations with intricate operations or a high volume of transactions. Using automation tools like neoeco can simplify this process. These tools not only ensure compliance with ISO 14064 but also produce reliable, audit-ready reports, saving time and reducing the risk of human error.

How does third-party verification under ISO 14064-3 improve the reliability of transport emissions data for stakeholders?

Third-party verification under ISO 14064-3 plays a key role in ensuring transport emissions data is both accurate and consistent with established international standards. When an independent organisation reviews this data, it helps businesses demonstrate openness and earn the trust of stakeholders - whether that's regulators, clients, or investors.

This kind of verification strengthens confidence by confirming that emissions calculations adhere to the correct methodologies and that any reported reductions are legitimate and can be substantiated. For companies in transportation and logistics, it’s an essential step for meeting compliance standards and pursuing sustainability targets with assurance.