ESG and Firm Value: What Accountants Should Know

ESG metrics are reshaping how businesses are valued. With frameworks like ISSB and CSRD now in effect, sustainability reporting has become as rigorous as financial reporting. Here's why this matters:

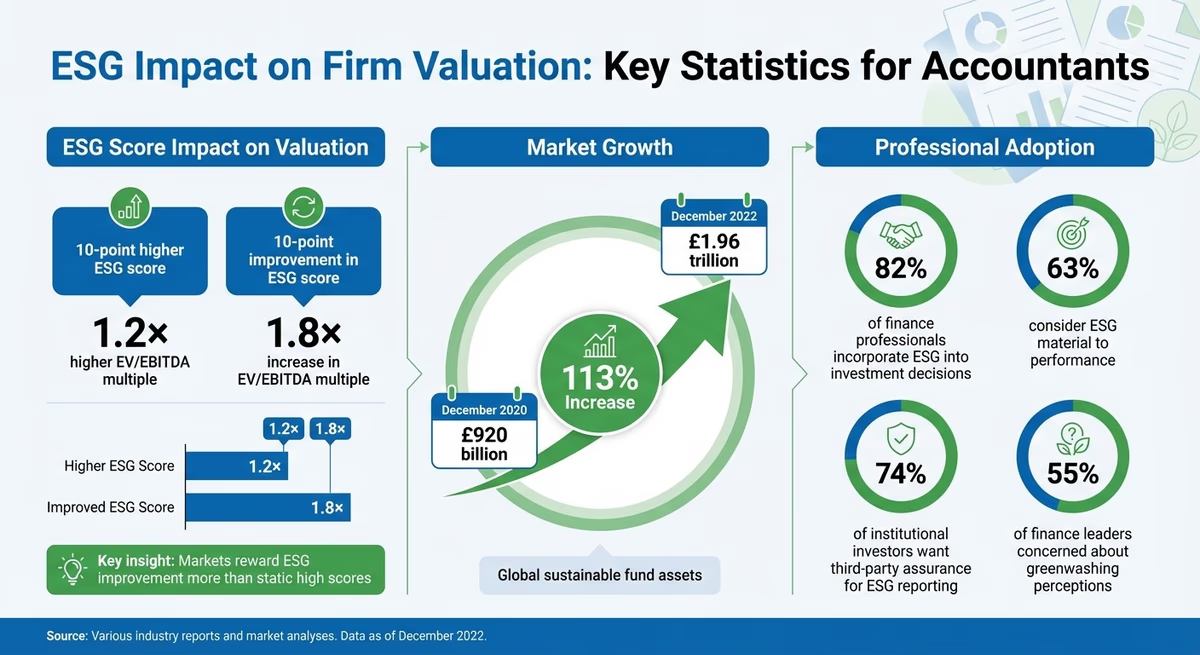

- A 10-point improvement in ESG scores can boost EV/EBITDA multiples by up to 1.8x.

- Global sustainable fund assets surged from £920 billion (Dec 2020) to £1.96 trillion (Dec 2022).

- 82% of finance professionals now factor ESG into investment decisions.

Accountants play a critical role in integrating ESG data into financial systems, ensuring it meets audit standards. By treating sustainability metrics with the same precision as financial data, firms can manage risks and improve valuation. Tools like neoeco simplify this process by linking financial transactions to recognised sustainability frameworks.

ESG Impact on Firm Valuation: Key Statistics for Accountants

How ESG Performance Affects Firm Valuation

The Link Between ESG and Firm Value

ESG performance plays a key role in shaping firm valuation, primarily through adjustments to discount rates and valuation multiples. Rather than altering cash flow estimates, financial professionals factor ESG into assessments of systematic risk and risk premiums. This approach reflects the growing recognition of ESG-related risks in investment decisions.

For example, companies with a 10-point higher ESG score often achieve an approximately 1.2x higher EV/EBITDA multiple. Moreover, firms that improve their ESG score by the same margin typically see an average 1.8x increase in their EV/EBITDA multiple. This highlights an important trend: markets tend to reward progress and momentum in ESG performance more generously than static high scores. For accountants advising on ESG strategies, this insight underscores the importance of demonstrating continuous improvement.

This shift in capital allocation priorities has been significant. Global sustainable fund assets grew from £920 billion in December 2020 to £1.96 trillion by December 2022. Additionally, 82% of finance professionals now incorporate sustainability information into their investment decisions, with 63% considering it material to performance. ESG has transitioned from being a peripheral issue to a central driver of valuation. Much of this integration is being pushed by external stakeholders - such as shareholders, debtholders, and consultants - rather than internal corporate actors. This dynamic creates a pressing need for accountants to provide reliable and audit-ready ESG data. This requires firms to build traceable ESG data systems that ensure accuracy and transparency.

However, the impact of ESG on valuation is far from uniform. Industry-specific factors and regional regulations significantly influence how ESG considerations affect firm value.

How ESG Impact Varies by Sector and Geography

While ESG considerations broadly influence valuations, their effects are highly dependent on industry and geography. The weight placed on the Environmental (E) and Social (S) pillars varies by sector, while the Governance (G) pillar tends to have a more consistent influence across industries. For instance, sectors such as oil, gas, and chemicals face steeper discount rate adjustments due to higher exposure to transition and physical risks.

Geographical differences are equally important. European companies, for example, operate under stricter regulations, such as the Sustainable Finance Disclosure Regulation (SFDR) and the Corporate Sustainability Reporting Directive (CSRD). These frameworks require deeper ESG integration into valuations compared to less regulated regions . As a result, European financial professionals are leading the way in ESG valuation practices, with institutional investors increasingly viewing ESG as a core component of systematic risk rather than an optional factor.

For UK accounting firms, understanding these regional and sector-specific nuances is vital. Whether advising on cross-border investments or preparing clients for domestic requirements like the UK Sustainability Reporting Standards (UK SRS), staying informed about these evolving frameworks is key to delivering effective guidance.

The Role of Financial Accounting in ESG Valuation

Integrated Reporting and ESG Disclosure

Sustainability reporting has evolved from general narratives to precise, financially integrated data. Frameworks like the UK SRS and IFRS S1 vs S2 require organisations to provide integrated, auditable disclosures. This pushes accountants to evaluate sustainability issues with a focus on risks and materiality that have a measurable financial impact. The goal is to move away from vague commitments and instead deliver verifiable, data-driven insights. This requires firms to align ESG data with ISSB standards to ensure global comparability. By embedding sustainability metrics into budgets, forecasts, and capital allocation, companies can make smarter decisions. For instance, linking carbon data to procurement decisions allows finance teams to understand the emissions impact of their purchasing choices directly. This integrated approach ensures sustainability data becomes an essential part of financial systems.

"Sustainability is becoming a finance function issue not by accident, but by necessity." - Stephen Pell, Co-founder and CEO, neoeco

Building Credibility Through Financially-Integrated Sustainability Management (FiSM)

FiSM takes integrated reporting a step further by embedding sustainability metrics directly into financial processes. It connects sustainability data to financial ledgers, eliminating the need for manual spreadsheets and reducing the chances of errors. For UK accounting firms, this approach helps break down data silos and ensures consistency. Tools like neoeco automate the mapping of financial transactions to emissions categories such as GHGP, ISO 14064, SECR, and UK SRS. By integrating with systems like Xero, Sage, or QuickBooks, these tools generate audit-ready reports directly from financial data.

"Accountants, already trusted with the integrity of financial statements, are uniquely placed to extend that trust to sustainability data." - Stephen Pell, Co-founder and CEO, neoeco

Managing ESG Risks: Controversies and Their Impact on Firm Value

The Financial Cost of ESG Failures

The connection between ESG performance and a company's value makes managing ESG risks essential for maintaining financial stability. When ESG controversies arise - whether they involve environmental violations, governance scandals, or social missteps - they often lead to financial losses. Analysts respond to such incidents by lowering long-term earnings forecasts, viewing ESG failures as a systematic risk factor. This means they adjust discount rates rather than cash flow projections, making ESG risks a key consideration in company valuations.

The financial impact, however, depends on which ESG pillar is involved. Environmental issues, such as greenhouse gas emissions or pollution, are more frequently reflected in valuation adjustments. On the other hand, social and governance issues, while harder to quantify, can also significantly damage investor trust. For example, poor management practices can lead to both reduced earnings expectations and a loss of confidence among investors. Furthermore, with 55% of finance leaders concerned that sustainability reporting in their sector might be dismissed as "greenwashing", the reputational damage from weak ESG management can extend far beyond immediate penalties. These risks highlight the importance of robust ESG strategies to protect both financial and reputational value.

Reducing Risk Through Better ESG Management

Strong ESG practices not only help companies avoid financial damage but can also enhance their valuation. For instance, an improvement of 10 points in an ESG score has been linked to a 1.8× increase in EV/EBITDA, showcasing the benefits of proactive risk management. Markets tend to reward clear, measurable improvements in ESG performance more than they do steady but unremarkable results.

To help companies reduce their exposure to ESG risks, accounting firms encourage the use of quantifiable, auditable data rather than relying on vague, narrative-driven commitments. Establishing a dedicated ESG Controller role within the finance team can ensure that sustainability data is held to the same rigorous standards as financial reporting. Conducting pre-audit assurance exercises can also help uncover gaps in data and controls early, allowing firms to address weaknesses before disclosures are made. With 74% of institutional investors indicating that independent third-party assurance would boost their confidence in ESG reporting, implementing rigorous processes can directly support a company's valuation and credibility. Tools that integrate sustainability metrics into financial systems - such as platforms designed for ISSB reporting - enable companies to manage ESG risks with the same precision applied to financial controls.

"Finance leaders are highlighting the difficulty of producing credible reporting disclosures due to the highly complex nature of sustainability topics and the overwhelming amount of reliable data required for the new mandatory sustainability reporting." - Dr. Velislava Ivanova, EY Global Strategy and Markets Leader, Climate Change and Sustainability Services

Key Financial Metrics for Measuring ESG Impact

Core Metrics: EV/EBITDA and DCF Models

For accountants, understanding how traditional financial metrics intersect with sustainability performance is becoming essential. One key metric, the EV/EBITDA multiple, has shown a 1.8× increase with a 10-point improvement in ESG scores. This makes it a critical indicator of the "ESG value premium." When it comes to Discounted Cash Flow (DCF) models, ESG considerations are now being factored in as a systematic risk. Instead of altering specific cash flow items, adjustments are made to the discount rate to reflect sustainability risks. This approach ensures ESG factors are integrated seamlessly into established financial frameworks.

Sustainability-Specific Indicators

Incorporating sustainability into financial analysis means accountants are increasingly required to evaluate carbon emissions during capital allocation, budgeting, and forecasting. Among the Environmental, Social, and Governance pillars, greenhouse gas emissions have emerged as the dominant factor in environmental assessments. Meanwhile, workforce well-being metrics lead the Social pillar, and management quality remains central to the Governance pillar.

To adapt, accountants must employ reliable methods that quantify sustainability risks in financial terms. These risks should be included in enterprise risk registers, allowing firms to calculate potential exposures in monetary terms. Tools and platforms, such as those designed for ISSB reporting, are bridging the gap between sustainability data and financial systems. By directly linking emissions data to financial reporting, these platforms ensure sustainability metrics are held to the same rigorous standards as traditional accounting data.

"Sustainability data must now be treated with the same professional scrutiny and discipline as financial data." - Stephen Pell, Co-founder and CEO, neoeco

The market is clearly favouring companies that demonstrate measurable ESG improvements. Firms that actively enhance their ESG scores often experience stronger valuation growth compared to those that maintain static results. By treating sustainability risks with the same precision as financial data, accountants can improve valuation models and help guide companies toward impactful ESG advancements.

Understanding Conflicting ESG Research Findings

Why ESG Research Findings Differ

Accountants analysing ESG research often face conflicting conclusions about how sustainability performance impacts firm value. These discrepancies arise from challenges in ESG data collection, ratings, and analysis methods.

ESG rating providers frequently disagree on the same company. Providers like MSCI, Refinitiv, and Sustainalytics use different proprietary methodologies. For example, Refinitiv tracks over 500 Key Performance Indicators (KPIs), leading to low correlations in scores for the same firm. Additionally, frequent changes to methodologies and historical data revisions make it difficult to compare results over time.

Regulatory differences also influence research outcomes. Studies focusing on European markets often show stronger ESG integration, driven by regulations such as the Sustainable Finance Disclosure Regulation (SFDR). Conversely, research from regions with less stringent ESG requirements may highlight varying levels of adoption or disclosure practices. Sector-specific factors also play a role - industries like oil, gas, and electric utilities tend to price climate risks more prominently than others.

Valuation methods vary widely. Some analysts adjust discount rates to reflect ESG as a risk factor, while others modify cash flow projections directly. A study of 3,025 non-financial companies in the eurozone between 2005 and 2020 found that while traditional accounting measures now explain less about market values than they did in 2005, ESG ratings have yet to show consistent value relevance in explaining price variations. This indicates that markets are still figuring out how to price ESG data effectively.

These differences highlight the importance of incorporating detailed and reliable ESG metrics into financial analysis, especially for accountants aiming to bridge these gaps.

Applying Research Insights to Accounting Practice

Given the inconsistencies in ESG research, accountants must approach ESG data with a critical eye when integrating it into valuation models. It’s essential to understand the rating provider’s methodology and the specific metrics they prioritise. Rather than relying on aggregate scores, focus on detailed, sector-relevant indicators. For example, greenhouse gas emissions are key for environmental assessments, while workforce well-being metrics are central to the Social pillar.

"The lack of commonly accepted ESG reporting standards or low levels of ESG reporting regulation at the firm level leads to comparability issues, limiting an investor's ability to select firms on ESG criteria." - Amel-Zadeh and Serafeim

Distinguish between risk-based and cash flow-based approaches in ESG valuations. A survey of over 300 European financial professionals revealed that most respondents preferred adjusting discount rates over cash flow components when incorporating ESG into Discounted Cash Flow (DCF) models. Understanding the valuation mechanism used in research can help accountants determine its relevance to specific client needs.

It’s also worth noting that external stakeholders, such as investors, often integrate ESG into valuation models more extensively than corporate insiders. This gap suggests that research findings may reflect investor priorities more than operational realities. By grounding ESG disclosures in financially-integrated sustainability management, companies can align sustainability data with traditional financial reporting, ensuring it receives the same level of scrutiny and reliability.

Reporting and Valuation | Intro to ESG Course (Part 6)

Key Takeaways for Accounting Professionals

Accountants play a critical role in linking ESG performance with firm value. Your skills in risk management and materiality assessments are vital for embedding sustainability data into financial analysis. As Stephen Pell, Co-founder and CEO of neoeco, puts it:

"Sustainability data must now be treated with the same professional scrutiny and discipline as financial data."

Here's why this matters: research shows that a 10-point increase in an ESG score is associated with approximately a 1.2× EV/EBITDA multiple. Even more striking, a 10-point improvement can raise the multiple by about 1.8×. These numbers underline the tangible market impact of ESG performance, which accountants are uniquely positioned to quantify and communicate.

Sustainability reporting has evolved. No longer just marketing fluff, it’s now about auditable, integrated data. Frameworks like the UK SRS and ISSB require carbon data to directly inform capital allocation, budgets, and forecasts. This shift demands what neoeco calls financially-integrated sustainability management, where sustainability metrics are treated as part of the financial core.

Accountants should focus on sector-specific indicators and use materiality assessments to pinpoint direct financial risks. In valuation models, consider adjusting discount rates based on ESG performance rather than solely relying on cash flow projections. This approach helps reflect the broader impact of sustainability efforts on a company’s financial outlook.

For those looking to stay ahead, neoeco provides sustainability accounting software that simplifies the process. It maps financial transactions to recognised emissions categories (such as GHGP, ISO 14064, SECR, and UK SRS), eliminating the need for spreadsheets or manual conversions. This tool enables accountants to expand their services into sustainability management with minimal additional training, making compliance-ready carbon accounts more accessible than ever.

FAQs

How do ESG scores impact a company's valuation?

Companies with higher ESG scores often enjoy a boost in valuation. Why? Because strong ESG performance can lower a business's cost of capital and improve profit margins. Investors tend to view such companies as less risky and more dependable, making them a more appealing choice for investment.

On the flip side, poor ESG scores can spell trouble. They can raise perceived risks, drive up financing costs, and shake investor confidence, all of which can drag down a company's valuation. For accounting professionals, it's crucial to understand that ESG performance is now a key player in financial decision-making and building long-term value.

How can accountants help integrate ESG data into financial reporting?

Accountants are at the forefront of turning ESG data into dependable, audit-ready information that aligns seamlessly with financial reporting standards. By applying the same rigorous controls and verification processes used for financial statements, they ensure sustainability metrics are treated as robust, actionable data rather than mere narrative. This approach is critical for meeting the requirements of frameworks like the UK SRS, ISSB S1/S2, and other jurisdiction-specific standards.

With the help of tools that automate the mapping of transaction-level data to recognised emissions categories - such as Scope 1–3 under the GHGP or SECR - accountants can integrate metrics like carbon intensity per £ million of revenue directly into financial systems. Platforms such as neoeco simplify this process by integrating with widely used accounting software like Xero, Sage, and QuickBooks. This eliminates the need for manual spreadsheets, delivering accurate, finance-grade carbon data and audit-ready reports.

This seamless integration not only ensures compliance but also allows businesses to connect ESG performance with financial outcomes. Firms can uncover cost-saving opportunities, evaluate risks affecting valuation and cash flow, and make strategic, data-driven decisions. By bridging the gap between finance and sustainability, accountants empower organisations to navigate ESG challenges with precision and insight.

How does ESG affect firm value across industries and regions?

The influence of ESG (Environmental, Social, and Governance) factors on a company's value shifts dramatically depending on its industry and location. For energy-heavy industries like oil, gas, and utilities, environmental concerns such as carbon pricing and emissions reporting take centre stage. On the other hand, consumer goods and manufacturing businesses feel the impact more when it comes to sustainable supply chains and maintaining a positive brand image. For technology companies, governance and social issues - think data privacy and workplace diversity - are the main focus. Meanwhile, financial services experience heightened scrutiny around climate-risk management and disclosure practices.

Region also plays a huge role in how ESG factors affect businesses, thanks to differences in regulations and market demands. In Europe and the UK, strict standards like the EU Taxonomy and the UK SRS push companies to provide detailed emissions data. Falling short can lead to fines or higher borrowing costs. Over in the United States, the regulatory landscape is more fragmented, with varying rules at federal and state levels leading to inconsistent adoption. In emerging markets, while stringent laws may be lacking, firms are under increasing pressure from stakeholders to embrace ESG principles.

For accountants, navigating these diverse industry and regional challenges requires a tailored approach. Tools like neoeco, which blend financial data with established emissions frameworks, can help companies not only stay compliant but also highlight the financial advantages of robust ESG practices.