CDP Water Security Reporting Guide 2025

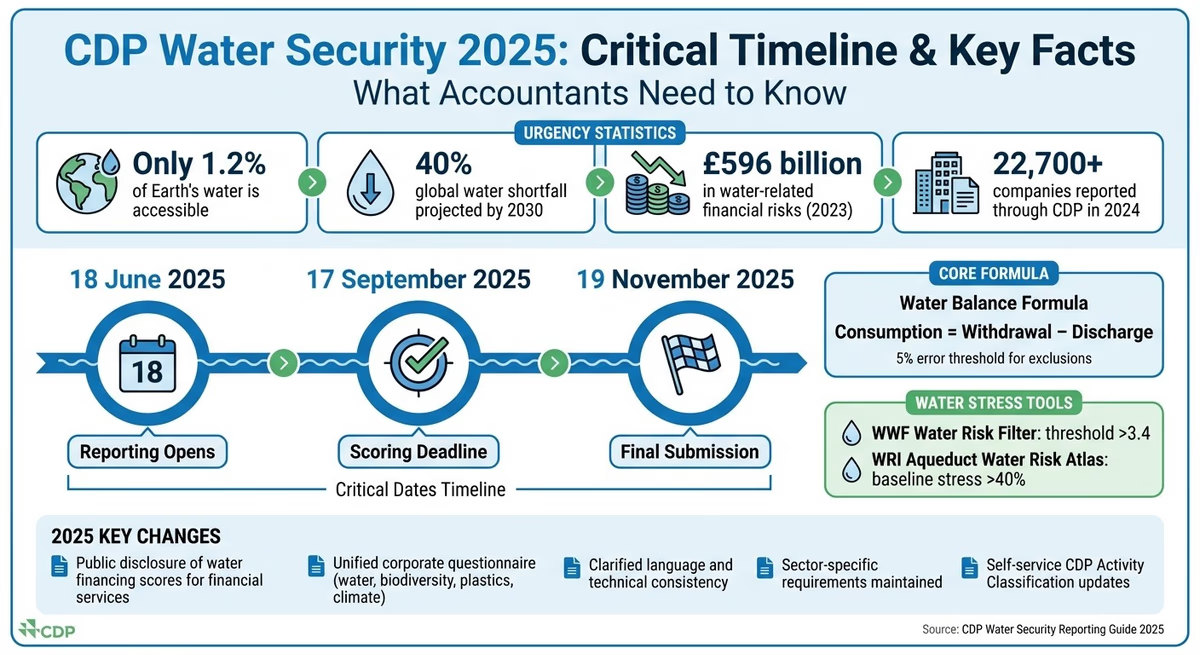

Water is running out, and businesses need to act. The 2025 CDP Water Security framework helps organisations disclose water use, risks, and impacts. With only 1.2% of Earth's water accessible and a projected 40% shortfall by 2030, the stakes are high. In 2024, over 22,700 companies reported through CDP, and the updated framework focuses on clarity, standardised accounting, and sector-specific rules. Key dates to remember:

- 18th June 2025: Reporting opens.

- 17th September 2025: Scoring deadline.

- 19th November 2025: Final submission.

This year introduces public disclosure of water financing scores for financial services and a unified corporate questionnaire covering water, biodiversity, plastics, and climate. Tools like neoeco simplify compliance by linking water data with financial records. The formula for water balance remains: Consumption = Withdrawal – Discharge, with strict rules on exclusions and boundary definitions.

Reporting accurately and on time can prevent financial risks - estimated at £596 billion in 2023 alone - and help organisations meet investor expectations. Here's everything you need to know to prepare effectively.

CDP Water Security 2025 Key Dates and Framework Overview

Navigating Pathways to Water Security and Beyond with CDP ft. Cate Lamb | ESG Decoded Podcast #109

What Changed in the 2025 CDP Water Security Framework

CDP introduced only minor adjustments to the questionnaire and scoring methodology for 2025. The main goal this year is to maintain stability, enabling organisations to track their performance over time without dealing with major structural changes.

Instead of adding new requirements, CDP has concentrated on clarifying existing language and addressing technical inconsistencies. This approach allows organisations to continue using familiar frameworks while benefiting from clearer guidance, making the scoring criteria easier to understand.

A key update for 2025 is the public disclosure of water financing scores for financial services firms for the first time. This reflects growing investor interest in how financial institutions influence water security through their capital allocations.

Updated Water Accounting Criteria

The framework for 2025 continues to prioritise standardised definitions for withdrawal, discharge, and consumption to improve data comparability. Water is considered to cross your organisational boundary when it is used, managed, or incorporated into products by your clients, regardless of location.

Organisations are required to report a full corporate water balance using the formula:

Consumption = Withdrawal – Discharge. This calculation must include all water entering or leaving the management boundary, measured at the point of entry or exit.

Quality-based reporting remains a key focus. Companies must distinguish between fresh surface water (TDS <10,000 mg/l) and brackish or seawater (TDS >10,000 mg/l). This differentiation helps investors gauge exposure to water scarcity risks more accurately.

The framework allows companies to exclude collected rainwater and domestic sewage from discharge volumes, but only if the omission results in less than a 5% error in the water balance. To ensure compliance, organisations must run a trial balance to confirm the exclusion stays within this threshold.

Sector-Specific Requirements

A new self-service feature now allows companies to update their CDP Activity Classification directly through the portal during the disclosure window. This ensures that sector-specific questions align better with actual business activities - a particularly useful update for diversified organisations.

Sector classification applies when an activity accounts for more than 20% of revenue. However, only the primary sector influences scoring. Environmental themes, such as Water Security, are assigned based on Impact Classification, with activities rated as "Critical" or "Very High" automatically receiving the theme.

Certain industries face specific reporting requirements:

- Oil and gas companies must include produced water (moisture extracted with raw materials) in total withdrawal figures, even though this is often excluded in industry-specific reports.

- Mining operations need to report water diversions as both withdrawals and discharges.

- Electric utilities using hydropower must account for river inflow, surface runoff, and precipitation onto reservoir surfaces as withdrawals.

Changes to the Scoring System

The scoring methodology remains unchanged apart from minor wording adjustments. This consistency makes it easier for companies to demonstrate progress across Awareness, Management, and Leadership levels without having to adapt to new benchmarks.

Scoring continues to reward organisations for detailed water balance reporting, adherence to standardised calculations, and the use of recognised water risk tools. Examples include the WWF Water Risk Filter (threshold above 3.4) and the WRI Aqueduct Water Risk Atlas (baseline water stress above 40%) for identifying water-stressed catchments.

The scoring deadline is 17th September 2025, with results available to disclosers starting 10th December. Late submissions won't be scored but can still be disclosed for transparency.

These updates highlight the growing demand for platforms that integrate financial and environmental data. For accounting firms handling clients across various sectors, tools like neoeco - built on financially-integrated sustainability management principles - simplify compliance by linking water reporting directly with financial data, eliminating the need for separate spreadsheets for each environmental theme.

How to Prepare for CDP Water Security Reporting

The 2025 reporting window opens on 18th June, with the scoring deadline set for 17th September. This three-month period is critical for accountants to gather data, verify calculations, and submit disclosures that meet compliance standards. Starting early is especially important for clients managing operations across multiple sites or industries with specific water accounting requirements. A key first step is defining the reporting boundary to ensure all relevant water flows are included.

Align Water Reporting with Financial Boundaries

CDP uses a management boundary approach rather than focusing on physical or legal boundaries. This means water is considered within your client's boundary if it is used, managed, or incorporated into products - even if the activity occurs outside the corporate site.

"Water is considered to have crossed the boundary of an organisation, at either the corporate or site level, when the organisation in any way uses it, comes into contact with it, is required to manage it or when it becomes incorporated into products." - CDP Technical Note on Water Accounting

This definition means you must account for water flows from services like street cleaning or operations at remote sites. To determine whether disclosures should be made at the group level or by individual subsidiaries, refer to CDP's Parent-Subsidiary policy. Deciding this early simplifies data consolidation and ensures a smoother reporting process.

Collect and Verify Water Data

Once boundaries are set, the focus shifts to accurate data collection. Start by gathering volumetric data for water withdrawals, discharges, and consumption. Use the standard formula: Consumption (C) = Total Withdrawal (W) – Total Discharge (D). If discharges exceed withdrawals - for example, when previously stored water is released - a negative consumption value is acceptable.

Water withdrawals must be categorised by source, such as fresh surface water (including rainwater), brackish water, seawater, renewable and non-renewable groundwater, produced water, and third-party sources. Tracking these categories separately ensures precision in reporting.

Identify sites operating in water-stressed areas using tools like the WWF Water Risk Filter (medium risk threshold above 2.6) or the WRI Aqueduct Water Risk Atlas (baseline water stress above 40%). The financial risks tied to water stress are substantial - companies reported $596 billion in water-related risks in 2023 alone. This underscores the importance of conducting thorough risk assessments.

Sector-specific requirements must also be addressed. For instance, oil and gas companies need to include "produced water" in their withdrawal figures, while mining operations must report water diversions as both withdrawals and discharges. Missing these sector-specific details is a common compliance issue.

Managing Exclusions

Certain exclusions are permitted by CDP, such as collected rainwater and domestic sewage from discharge volumes, but only if excluding them results in a water balance error of less than 5%. Always re-check calculations to ensure exclusions don’t exceed this threshold.

Clearly document all exclusions. For activities outside the defined management boundary, provide explanations in the disclosure. Poor documentation is a frequent stumbling block - only 103 companies (roughly 2% of respondents) made the CDP Water Security "A List" in 2023, often due to incomplete or inconsistent records.

For extraction industries, double-check that water classifications - like "produced" and "entrained" water - are consistent with CDP guidelines. Misclassifications can lead to non-compliance and missed scoring opportunities.

Common Mistakes and How to Avoid Them

Accurate CDP disclosures hinge on avoiding common pitfalls, particularly when it comes to documentation and alignment with reporting frameworks. In 2023, incomplete documentation alone kept 103 companies - 2% of respondents - from earning a spot on the CDP Water Security "A List". Key issues often include improperly defining organisational boundaries and neglecting to document exclusions thoroughly. Let’s dive deeper into how missing exclusion details and framework misalignment can hinder compliance efforts.

Missing Exclusion Details

One critical area to watch is the exclusion of certain water flows, such as collected rainwater or domestic sewage. If these exclusions cause the water balance error to exceed 5%, they must be included in calculations. This 5% threshold is non-negotiable, as exceeding it can compromise the accuracy of your reporting.

Documentation issues are another common stumbling block. As Bogdana Marinova, Senior Water Advisor at Waterplan, points out:

"The process of collecting data from sites is highly time-consuming, often involving data that comes in different timelines and formats."

To address this, standardising data collection across all facilities is crucial. Aligning this process with financial reporting cycles not only avoids last-minute rushes but also ensures your records are audit-ready. Beyond exclusions, ensuring consistency with other ESG frameworks is another significant challenge.

Misalignment with Other ESG Frameworks

CDP water disclosures must align with broader ESG frameworks like CSRD, ISSB, and GRI standards. One frequent issue is boundary discrepancies. While CDP uses a "management boundary" approach - covering water used, managed, or incorporated into products, even beyond physical sites - other frameworks often rely on legal entity boundaries.

Materiality approaches can also vary. CDP employs dual-perspective materiality (financial and environmental), CSRD requires double materiality, and GRI focuses on stakeholder impacts. To navigate these differences, organisations should conduct a gap analysis to identify deviations in water management boundaries relative to CDP requirements. Cross-referencing the CDP Technical Note on Water Accounting with GRI Standards and ISO 14046:2014 can help ensure consistent definitions of terms like "freshwater", "brackish water", and "produced water".

For companies juggling multiple reporting frameworks, adopting a ESG-accounting data integration approach can simplify compliance and streamline data collection across standards.

Software for CDP Water Security Reporting

Manually managing water disclosures across multiple sites is a risky and time-consuming process. The 2025 CDP framework introduces stricter requirements, including precise boundary definitions, consistent water accounting methods, and sector-specific calculations for factors like produced water and diversions. For accounting firms juggling these demands alongside frameworks like CSRD, ISSB, and GRI, adopting a financially integrated approach can prevent duplication and reduce errors. This highlights the growing need for a unified digital solution to streamline the process.

How neoeco Supports Water Security Reporting

neoeco bridges the gap between financial transactions and recognised standards like GHGP, ISO 14064, SECR, and UK SRS. By aligning water data with financial and management boundaries to align ESG data with ISSB standards, it helps minimise discrepancies caused by CDP's "management boundary" approach. This integration supports the broader goal of unifying financial and environmental reporting.

The platform automatically applies the 2025 CDP formula (C = W - D), factoring in sector-specific details such as produced water in the oil and gas industry and water diversions in mining. By automating these calculations, neoeco removes the need for manual reconciliations, helping organisations meet the 17th September 2025 deadline efficiently. Companies managing water-intensive supply chains can also benefit from the same transaction-level precision.

Audit-Ready Reports and Documentation

neoeco goes beyond automated reporting to simplify audit processes. The Policy & Evidence Hub consolidates all essential documentation - like site-level water meter readings, boundary definitions, and exclusion justifications - into a single, easily accessible repository. This eliminates the chaos of email chains, while live checklists track completed, pending, and review-ready tasks. Auditors are given secure, read-only access, ensuring full traceability and accuracy in line with ISO 14064 or ISSA 5000 standards.

For added convenience, neoeco generates branded client reports with automatic cross-references to ISSB reporting requirements. This ensures water disclosures align with IFRS S1 and S2 materiality assessments. For organisations adopting Financially-integrated Sustainability Management (FiSM), this unified approach allows water security data to flow seamlessly from the same ledger used for carbon accounts, management reports, and statutory filings.

Summary

The 2025 CDP Water Security framework introduces stricter boundary definitions, standardised water accounting practices, and sector-specific calculation rules. Accountants are required to consistently apply the formula C = W - D, confirm water-stressed areas using tools like the WRI Aqueduct Water Risk Atlas, and ensure exclusions are managed to maintain a water balance error margin below 5%. With the scoring deadline set for 17th September 2025, firms must adopt efficient strategies to meet these requirements while balancing other frameworks such as CSRD and aligning ESG data with ISSB.

These updates emphasise the growing importance of digital solutions to handle complex reporting demands. Managing 85 questions across 12 modules manually is simply unfeasible, especially when working with multiple clients. This is where neoeco becomes a game-changer for accounting firms. By aligning water data with financial reporting boundaries and automating sector-specific calculations, the platform minimises errors and significantly reduces reconciliation time. Its Policy & Evidence Hub consolidates all key documentation - meter readings, boundary definitions, and exclusion justifications - into a single, audit-ready repository. Additionally, live checklists provide real-time progress tracking.

Taking this a step further, neoeco offers an integrated approach by combining water and carbon disclosures on a single platform. Its Financially-integrated Sustainability Management (FiSM) system ensures water data flows directly from financial ledgers, delivering finance-grade accuracy without reliance on manual spreadsheets.

With £596 billion at stake due to water-related risks and a projected 40% global water shortfall by 2030, transparency and compliance in reporting are non-negotiable. Accountants who embrace a financially integrated approach can produce audit-ready reports that satisfy CDP standards while meeting broader investor expectations, positioning their firms as trusted advisers in an increasingly regulated environment.

FAQs

How does the CDP Water Security framework affect financial institutions?

The CDP Water Security framework urges financial institutions to assess, report, and manage risks tied to water scarcity, shifting regulations, and other water-related issues. It also encourages identifying opportunities linked to sustainable water practices, meeting increasing demands from capital markets for clear and transparent water-risk reporting.

By engaging with these guidelines, financial institutions can gain a deeper understanding of their water-related risk exposure, make more informed decisions, and show accountability to their stakeholders. Additionally, the framework helps organisations align with global sustainability standards, ensuring their operations are prepared for future challenges.

What challenges do companies face when aligning CDP water reporting with other ESG frameworks?

Companies often struggle to align their CDP water reporting with other ESG frameworks due to differences in definitions, boundaries, and how materiality is approached. For instance, CDP defines water-stressed areas at the catchment level, which might not match the geographic scopes used in frameworks like ISSB, CSRD, or GRI. These discrepancies in calculation methods and terminology can make it tough to reconcile data and maintain consistency.

A key challenge is managing impact materiality (prioritised by CDP and GRI) alongside financial materiality (emphasised in ISSB and CSRD). Many organisations adopt multiple reporting standards, which often results in duplicated efforts and an increased administrative burden. Without an efficient system, consolidating metrics such as water quantity, quality, and risk ratings across different frameworks can turn into a laborious and error-prone task.

For UK-based accounting firms, tools like neoeco offer a way to simplify this process. This finance-integrated sustainability platform automatically maps financial data to recognised water-related categories and generates audit-ready reports. By doing so, neoeco reduces manual effort, ensures compliance with CDP, ISSB, CSRD, and GRI frameworks, and improves both efficiency and accuracy.

Why is accurate water balance reporting important for managing financial risks?

Accurate water balance reporting plays a key role in helping organisations pinpoint serious water-related risks, including floods, shortages, or potential regulatory challenges. By tackling these issues head-on, businesses can reduce the likelihood of supply chain interruptions and steer clear of expensive fines or penalties.

Beyond regulatory compliance, this approach strengthens financial security by supporting smarter resource allocation and more effective long-term planning.