IFRS S2 vs Local ESG Standards in Latin America

Latin America is navigating the adoption of IFRS S2, a global framework for climate-related financial disclosures, while balancing local ESG standards. IFRS S2 simplifies reporting by focusing on financial materiality and mandating Scope 1, 2, and 3 emissions disclosures. However, the region faces challenges due to disparities in resources, data infrastructure, and SME readiness.

Key points:

- IFRS S2 is mandatory in Brazil (2026), Costa Rica (2025/2026), and Bolivia (2027). Mexico is still in consultation.

- Local ESG frameworks differ in timelines, assurance requirements, and focus areas, reflecting economic conditions.

- SMEs (99.5% of businesses) struggle with compliance due to limited capacity and data access.

- Technology can ease reporting by integrating financial and sustainability data, crucial as mandatory standards roll out.

Early compliance offers competitive advantages, especially for businesses aiming to attract global investment and remain in supply chains.

Webinar: Introduction to the ISSB´s standards and their implications for Latin American Markets

What is IFRS S2?

IFRS S2 is the International Sustainability Standards Board's framework for climate-related financial disclosures. Officially introduced for voluntary reporting periods starting on 1 January 2024, it aims to simplify reporting by offering a single framework, streamlining processes compared to other standards like TCFD, SASB, and CDP.

Unlike the EU's CSRD, which requires dual materiality (considering both the impact of climate on a company and the company's impact on the climate), IFRS S2 focuses solely on single materiality. This means it mandates disclosure of information that directly affects an entity's cash flows. As the IFRS Foundation explains: "Information is material if omitting, misstating or obscuring that information could reasonably be expected to influence decisions that primary users of general purpose financial reports make".

Core Requirements of IFRS S2

The framework is built around four key pillars, closely aligned with the recommendations from the Task Force on Climate-related Financial Disclosures (TCFD):

| Core Requirement | Description |

|---|---|

| Governance | The systems and processes in place to oversee and manage climate-related risks and opportunities. |

| Strategy | The organisation’s approach to managing climate risks, including transition plans and resilience through scenario analysis. |

| Risk Management | Methods for identifying, assessing, and monitoring climate-related risks. |

| Metrics & Targets | Performance indicators, including Scope 1, 2, and 3 emissions, and progress towards climate targets. |

One of IFRS S2's standout features is the mandatory disclosure of Scope 1, 2, and 3 emissions. These disclosures must follow the Greenhouse Gas Protocol Corporate Standard. By tying sustainability reporting to financial data, the framework highlights how climate risks influence a company’s financial health and operations. For businesses with intricate supply chains, understanding and reporting on Scope 3 emissions is a crucial step towards compliance. Many firms use Life Cycle Assessments to support Scope 3 reporting to ensure data accuracy.

Additionally, IFRS S2 requires companies to conduct climate-related scenario analysis. This includes assessing the resilience of their business strategies against scenarios aligned with the Paris Agreement's 1.5°C goal, a step beyond the 2°C scenarios traditionally recommended by TCFD.

Global Adoption of IFRS S2

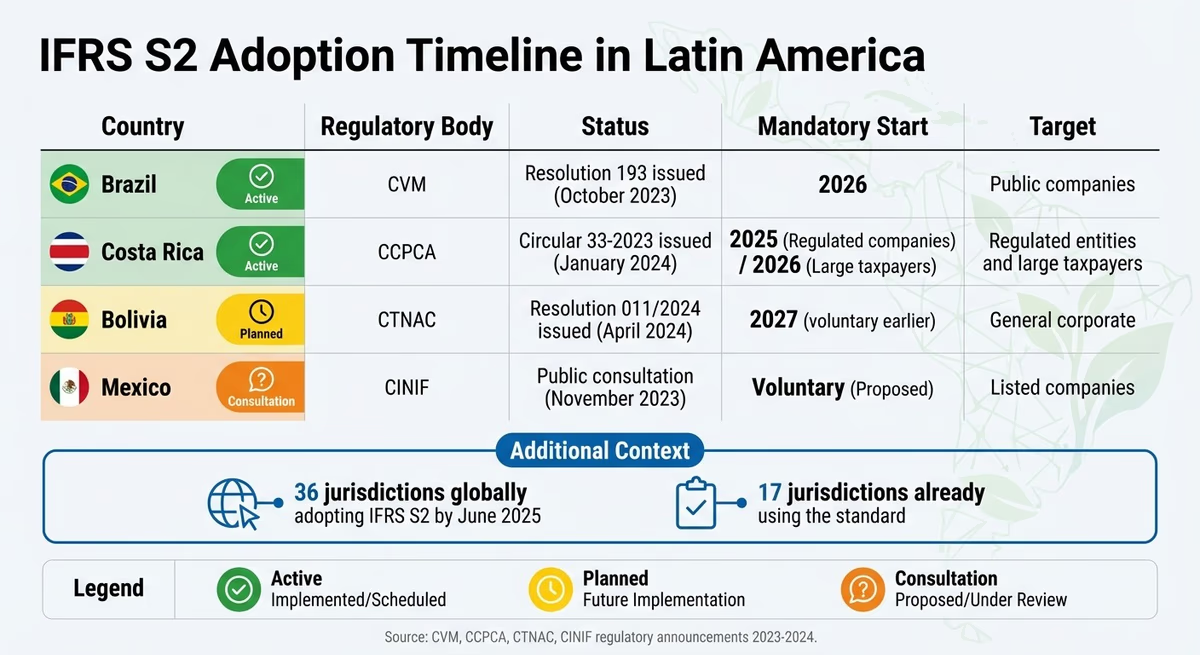

By June 2025, IFRS S2 had gained traction in 36 jurisdictions worldwide. Among these, 17 jurisdictions, including the UK, Brazil, Chile, and Mexico, have already adopted or are actively using the standard. Another 16 jurisdictions, such as China, Japan, Canada, and several Latin American nations (e.g., Bolivia, Costa Rica, and El Salvador), are in the process of implementing it.

The framework is steadily evolving from a voluntary guideline to a mandatory standard. In July 2023, the International Organisation of Securities Commissions (IOSCO) endorsed both IFRS S1 and S2 standards, underscoring strong global regulatory backing.

Lia Nicholson, Director of Sustainability at Terrascope, remarked: "IFRS S2 is now seen as the floor, not the ceiling, of climate disclosure".

This growing endorsement highlights how regulators are embedding IFRS S2 into national laws, making it obligatory for certain companies to comply. This trend is particularly noticeable in Latin America, where countries are integrating the framework into their ESG regulations. Next, we’ll explore how regional ESG frameworks in Latin America measure up against these global standards.

ESG Standards in Latin America

IFRS S2 Adoption Timeline and Status Across Latin America

Latin America is moving towards mandatory frameworks aligned with IFRS S2. Instead of creating entirely new standards, countries are either implementing the ISSB frameworks - IFRS S1 and S2 - directly or adjusting them to match their local priorities. This shift provides the foundation for exploring specific national approaches.

The rollout begins with public or regulated entities and gradually extends to larger taxpayers. This phased implementation acknowledges the capacity challenges in the region, where many organisations lack the technical infrastructure, trained personnel, and financial resources needed to produce reliable sustainability data.

Country-Specific ESG Frameworks

Several countries in the region have already established regulatory timelines. In October 2023, Brazil's capital markets regulator (CVM) issued Resolution 193, requiring public companies to adopt IFRS Sustainability Disclosure Standards starting from 1 January 2026.

The Brazilian Ministry of Finance and CVM stated: "The ISSB's Standards can help strengthen Brazilian capital markets by enhancing transparency around sustainability-related risks and opportunities and facilitate companies attracting capital and global investments".

Costa Rica has opted for a phased approach. In January 2024, the Institute of Chartered Accountants of Costa Rica (CCPCA) introduced Circular 33-2023, mandating adoption for regulated companies by 2025 and for large taxpayers by 2026. Meanwhile, Bolivia’s standard-setting body (CTNAC) issued Resolution 011/2024 in April 2024, officially adopting ISSB Standards with mandatory compliance beginning in 2027, though earlier voluntary adoption is allowed. Mexico’s standard-setter (CINIF) initiated public consultations in November 2023 but has yet to establish a mandatory timeline.

| Country | Regulatory Body | Adoption Status | Mandatory Start Date |

|---|---|---|---|

| Brazil | CVM | Resolution 193 issued | 2026 (Public companies) |

| Costa Rica | CCPCA | Circular 33-2023 issued | 2025 (Regulated), 2026 (Large taxpayers) |

| Bolivia | CTNAC | Resolution 011/2024 issued | 2027 (Voluntary earlier) |

| Mexico | CINIF | Public consultation | Voluntary (Proposed) |

When it comes to ESG reporting, the region shows notable disparities. By late 2024, 87% of listed companies in Colombia were reporting ESG information, compared to 62% in Mexico and just 44% in Argentina. However, external assurance remains limited - only 21% of ESG reports in Colombia and 34% in Mexico undergo external verification, far below France's 96%. Additionally, only 46% of businesses across Latin America have a formal sustainability policy or strategy.

Beyond these timelines, local adaptations present further challenges and distinctions from IFRS S2.

How Local Standards Differ from IFRS S2

Latin American countries are adjusting IFRS S2 to better reflect local economic conditions.

Julian Costábile, Partner of the Sustainability Department at SMS Latinoamérica, explained: "Just like with the International Financial Reporting Standards (IFRS), the implementation of these sustainability guidelines will vary between countries. Some will adopt them directly, whilst others will adapt them to their local realities".

One of the biggest hurdles is the region’s SME landscape. Small and medium enterprises make up 99.5% of businesses in Latin America, accounting for 60% of total employment and contributing 25% to regional GDP. These businesses often operate in a "survival mode", focusing on staying afloat rather than addressing complex issues like Scope 3 emissions.

Another significant challenge is the lack of data infrastructure. Many companies are forced to rely on benchmarks and protocols from developed markets, such as the United States, due to the absence of local resources. This can result in inaccurate comparisons and unfair evaluations of companies operating under vastly different conditions. To address this, countries are working on industry-specific adaptations that align with local regulations and economic realities while maintaining consistency with the ISSB reporting framework.

IFRS S2 vs Local ESG Standards: Key Differences

IFRS S2 sets a global baseline for climate-related disclosures. However, Latin American countries are tailoring its implementation to suit their specific economic contexts. These variations influence how businesses prepare reports and compete for international investment.

Differences in Scope and Applicability

IFRS S2 is designed for entities producing general-purpose financial reports, focusing on climate-related risks and opportunities that impact financial outcomes. In contrast, local regulations in Latin America are adopting phased approaches, targeting specific sectors. Here's how some countries are rolling out these requirements:

- Brazil: CVM Resolution 193 mandates IFRS S1 and S2 for public companies starting in 2026.

- Costa Rica: Circular 33-2023 requires compliance for regulated entities by 2025, with large taxpayers following in 2026.

- Bolivia: Resolution 011/2024 sets a 2027 start date but allows voluntary early adoption.

- Mexico: The CINIF is still in public consultation, leaving reporting voluntary for now.

| Country | Target Entities | Mandatory Start | Current Status |

|---|---|---|---|

| Brazil | Public companies | 2026 | Resolution 193 issued |

| Costa Rica | Regulated entities | 2025 | Circular 33-2023 issued |

| Costa Rica | Large taxpayers | 2026 | Circular 33-2023 issued |

| Bolivia | General corporate | 2027 (voluntary early adoption) | Resolution 011/2024 issued |

| Mexico | Listed companies | Voluntary (proposed) | Public consultation stage |

One major hurdle is the lack of robust data infrastructure. IFRS S2 assumes access to reliable metrics and benchmarks, but many Latin American firms depend on international protocols that may not align with local conditions. For example, a manufacturing company in Argentina might face challenges in calculating Scope 3 emissions due to insufficient supplier data systems.

Mandatory vs Voluntary Reporting

Another key difference lies in the shift from voluntary to mandatory reporting. While IFRS S2 acts as a global benchmark, local regulators determine the pace of its adoption. Currently, only 46% of Latin American businesses have a formal sustainability strategy, and in Mexico, just 25% publicly disclose ESG practices. In contrast, Colombia leads with 51% of companies sharing ESG information, even without a formal IFRS S2 mandate.

Assurance requirements also vary. Brazil and Mexico are introducing phased verification, starting with limited assurance and moving to reasonable assurance over 2–3 years. On the other hand, voluntary local reporting often lacks formal audit processes. For instance, while 87% of listed companies in Colombia disclose ESG data, only 21% undergo external assurance, compared to 96% in France.

"IFRS S2 is now seen as the floor, not the ceiling, of climate disclosure", said Lia Nicholson, Director of Sustainability at Terrascope.

Mexico's approach adds complexity for private companies. Unlike the investor-focused IFRS S2, Mexico's NIS B-1 requires private firms to disclose 30 specific indicators in the footnotes of audited financial statements. This means even smaller private entities must report sustainability data starting with fiscal years beginning 1 January 2025. Such variations highlight the challenges of integrating global standards with local frameworks.

Integration with Existing Local Frameworks

Latin American nations are blending existing standards with the ISSB framework. For example, Brazil uses CBPS 01 and 02 to implement IFRS S1 and S2, while Chile relies on NCG 461, which aligns with TCFD and SASB, before transitioning to mandatory IFRS S2 in 2026.

This approach helps reduce "reporting fatigue" since many companies already follow frameworks like the Global Reporting Initiative. Instead of duplicating efforts, local standards are designed to build on current practices.

However, Scope 3 reporting remains a challenge. Larger corporations depend on data from smaller suppliers, many of whom lack the resources to provide it.

"The variability in economic, environmental, and social conditions makes direct adoption challenging. Therefore, it is expected that some countries will adjust these standards to reflect their realities while maintaining the essence of the global requirements", explained Julian Costábile, Partner of the Sustainability Department at SMS Latinoamérica.

Technology is playing a critical role in addressing these gaps. Businesses adopting ISSB reporting need systems that integrate financial and sustainability data seamlessly. This is especially important as regulators move toward mandatory external assurance, requiring audit-ready documentation and clear data trails. Specialized sustainability accounting software can help firms bridge this gap by connecting financial and ESG data on a single ledger.

Alignment Opportunities and Implementation Challenges

Where IFRS S2 and Local Standards Align

IFRS S2 was designed as a "global baseline", allowing Latin American countries to build on its framework by adding local requirements without compromising the core international standards. This approach naturally creates opportunities for alignment, as IFRS S2 incorporates well-established frameworks like the Task Force on Climate-related Financial Disclosures (TCFD) and SASB Standards.

The most noticeable convergence is in the areas of climate risk disclosures and greenhouse gas reporting. Both frameworks require organisations to report on Scope 1, 2, and 3 emissions, assess climate risks, and provide governance disclosures. For instance, Brazil is updating its regulatory framework to implement IFRS S2 while maintaining existing local practices. Similarly, other countries in the region are preparing to align their standards in anticipation of mandatory adoption.

The ISSB has also introduced "proportionality measures" to assist entities with limited resources. Its "undue cost or effort" clause allows companies to rely on reasonable and supportable information when identifying risks or measuring emissions. This flexibility is particularly helpful for Latin American firms, many of which lack advanced data systems or locally relevant benchmarks. However, despite these alignment opportunities, significant implementation hurdles remain.

Implementation Challenges in Latin America

While alignment with IFRS S2 offers potential benefits, implementation in Latin America faces considerable challenges. One of the biggest issues is the lack of capacity and expertise, with a notable shortage of trained sustainability professionals who can produce reliable, high-quality data.

"Without the right human capital, the implementation of sustainability standards will be superficial", said Julian Costábile, Partner of the Sustainability Department at SMS Latinoamérica.

The numbers highlight the problem: only 46% of Latin American businesses have a formal sustainability policy, and 30% cite the generation and monitoring of key performance indicators (KPIs) as a major challenge. While half of the businesses in the region now employ a dedicated Head of Sustainability, many still lack the broader teams necessary for comprehensive sustainability reporting.

Another issue is the lack of local data and benchmarks. Many organisations depend on international guidelines, such as US-based SASB protocols, which may not fully address the unique circumstances of Latin American markets. Small and medium-sized enterprises (SMEs) face even greater difficulties.

"In less developed regions, many SMEs operate in 'survival mode.' Their primary concern is staying operational, even when facing severe economic difficulties and an unfavourable context", noted Costábile.

This situation poses risks across the value chain. Large corporations rely on SME suppliers for Scope 3 emissions data, yet only 13% of SMEs globally have adopted sustainability strategies. Without adequate support, these smaller businesses could find themselves excluded from international supply chains.

How Technology Simplifies Compliance

Technology offers a practical solution to many of these challenges, helping bridge the gaps in expertise and capacity while enabling the creation of consistent, verifiable sustainability data. For accounting firms working with Latin American clients, integrating financial and sustainability information is becoming essential, especially as regulators move towards mandatory external assurance.

Platforms like neoeco, which focus on financially-integrated sustainability management, address this need by linking sustainability metrics directly to financial systems. This integration eliminates manual data collection and conversion, allowing organisations to produce audit-ready ESG disclosures using their existing financial infrastructure.

The automation of KPI tracking and reporting becomes even more critical as countries shift from voluntary to mandatory sustainability reporting. Brazil, for example, will require compliance with ISSB standards starting in 2026, while Costa Rica is phasing in adoption from 2025. Scalable technology solutions are key, enabling firms to adapt without proportional increases in staffing or costs.

For large companies working with SME suppliers, technology also plays a crucial role in knowledge sharing. Digital tools can guide smaller suppliers through the reporting process, ensuring data quality without requiring extensive training or resources.

Conclusion

Key Takeaways for Businesses

Latin American businesses face the dual challenge of aligning with IFRS S2 standards while also meeting local ESG requirements. IFRS S2 serves as a global benchmark but allows for regional adaptations, creating opportunities to harmonise climate risk disclosures and greenhouse gas reporting with international expectations.

"Those companies that manage to get a head start in adopting the new IFRS S1 and S2 standards will have a significant competitive advantage, not only in terms of compliance, but also in their ability to attract investment and enhance their reputation", says RSM Latin America.

This framework translates into specific, time-sensitive regulations across the region. Countries with mandatory adoption deadlines highlight the urgency of early compliance. Businesses that act now will position themselves for long-term success. Currently, only 46% of Latin American companies have formal sustainability policies in place. Early adopters will not only stand out in local and global markets but also address regulatory challenges and data infrastructure gaps, which are critical for sustained resilience.

For SMEs, the stakes are even higher. Non-compliance could mean exclusion from global supply chains - a significant risk, considering SMEs make up 99.5% of businesses in the region. Larger corporations are increasingly demanding sustainability data from their suppliers. As Julian Costábile puts it, ESG reporting should be seen as a "business case" for resilience and opportunity.

Next Steps: Using Technology for Compliance

To meet these complex requirements, businesses need advanced, integrated reporting systems. Latin America faces a notable capacity gap, with a shortage of trained professionals and outdated data infrastructure. This makes technology not just helpful but essential. With 30% of businesses identifying KPI generation and monitoring as a primary challenge, manual processes simply cannot keep up as reporting becomes mandatory.

Platforms like neoeco offer a solution by integrating sustainability metrics with financial systems. These tools eliminate the need for manual data collection and ensure audit-ready reports that align with both IFRS S2 and local standards. For accounting firms working with Latin American clients, adopting such platforms allows them to provide professional sustainability services without the need for additional staff or increased costs.

The clock is ticking on mandatory reporting. Businesses that invest in robust data systems and the right technology now will be better prepared to meet regulatory demands. More importantly, they’ll be in a stronger position to attract international investment, which increasingly depends on transparent and comparable ESG data.

FAQs

What are the key differences in compliance timelines between IFRS S2 and local ESG standards in Latin America?

The IFRS S2 standard sets a universal compliance start date of 1 January 2025. This means that any organisation adopting the ISSB baseline will need to begin mandatory reporting from that point onwards.

On the other hand, ESG standards in Latin America operate on a country-specific timeline. Some nations in the region have already introduced national frameworks requiring earlier disclosures, while others are still in the process of finalising their regulations. In these cases, compliance deadlines may stretch into 2025 or even 2026. This staggered rollout mirrors the differing speeds at which countries are adopting these standards.

In essence, while IFRS S2 enforces a single global deadline, Latin American countries are taking a more gradual and locally tailored approach to implementing ESG standards.

What are the main challenges for SMEs in Latin America when complying with IFRS S2 climate-related disclosures?

Small and medium-sized enterprises (SMEs) in Latin America are facing tough hurdles when it comes to meeting IFRS S2 compliance. Limited resources, fragmented local ESG regulations, and a lack of in-house expertise are some of the key challenges holding them back. For many SMEs, issues like governance and data collection - both essential for meeting the standard’s detailed requirements, such as reporting on Scope 1, 2, and 3 emissions - are especially difficult to tackle.

A recent survey revealed that fewer than half of SMEs in the region have formal sustainability policies in place. Many don’t have dedicated sustainability leads or systems to track ESG-related metrics. Building the necessary infrastructure, training employees, or hiring external consultants often comes with a price tag that’s out of reach for businesses already operating on tight budgets. The situation is further complicated by the disconnect between local ESG frameworks and IFRS S2, making it even harder for SMEs to justify the steep initial investment required for compliance.

This mix of limited resources, regulatory uncertainty, and high costs has created a significant roadblock for SMEs in Latin America trying to adopt IFRS S2.

How can Latin American businesses use technology to comply with IFRS S2 requirements?

Technology plays a key role in helping Latin American businesses comply with IFRS S2 Climate-related Disclosure requirements. This standard calls for companies to integrate climate-related governance, strategy, risk management, and metrics into their financial reporting. With the right digital tools, businesses can simplify the processes of data collection, analysis, and reporting, making compliance far more manageable.

Sustainability accounting software is a game-changer here. These platforms can pull transaction-level data directly from accounting systems like Xero, Sage, or QuickBooks and categorise emissions using established frameworks such as GHGP and ISO 14064. They also offer real-time tracking of climate metrics, built-in risk assessments aligned with IFRS S2, and the ability to generate audit-ready reports. By leveraging these tools, businesses can minimise manual work, enhance data accuracy, and meet IFRS S2 requirements efficiently - all while staying focused on advancing their sustainability goals.