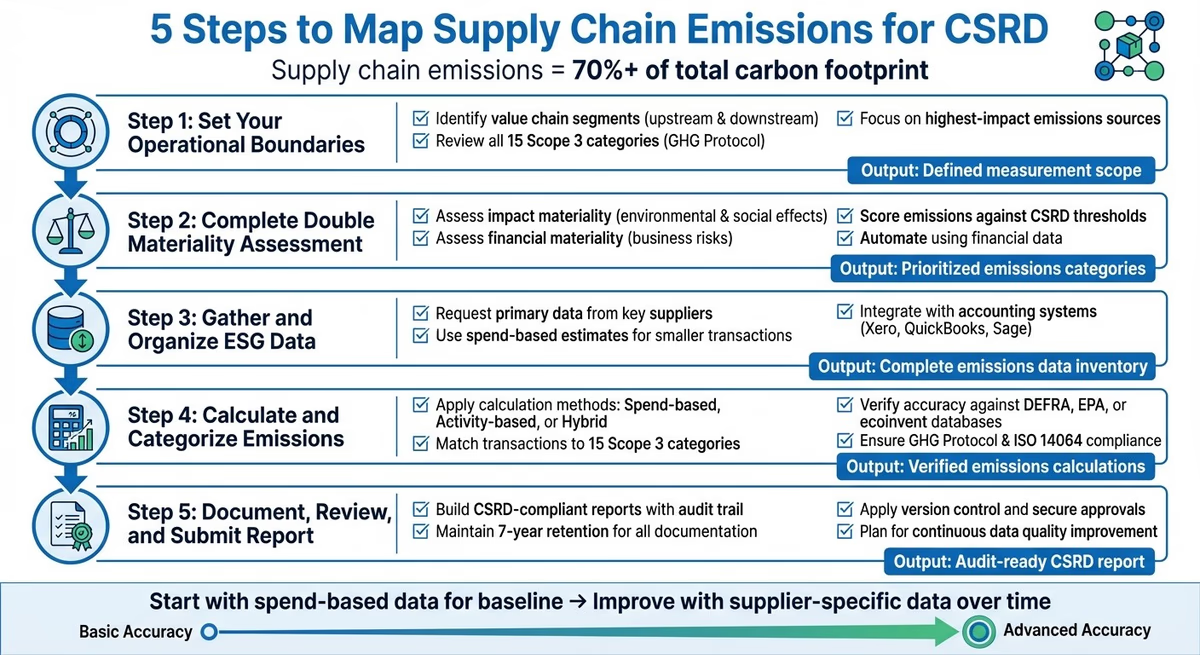

5 Steps to Map Supply Chain Emissions for CSRD

Supply chain emissions make up over 70% of a company’s carbon footprint. Under the Corporate Sustainability Reporting Directive (CSRD), mapping these Scope 3 emissions is mandatory. Here's how you can do it effectively:

- Set Boundaries: Identify which parts of your value chain to measure, focusing on the most impactful Scope 3 categories (e.g., purchased goods, transport).

- Double Materiality Assessment: Evaluate emissions based on how they affect the environment and your business risks.

- Collect ESG Data: Gather precise data from key suppliers or use spend-based estimates for smaller transactions.

- Calculate Emissions: Use spend-based, activity-based, or hybrid methods to quantify emissions for each Scope 3 category.

- Document and Report: Ensure reports are audit-ready, with clear links between data sources and emissions calculations.

Tools like neoeco simplify this process by integrating emissions tracking with financial systems like Xero or QuickBooks, reducing manual work and ensuring compliance. Start with spend-based data for a baseline and improve accuracy over time by collecting supplier-specific information.

5-Step Process to Map Supply Chain Emissions for CSRD Compliance

CSRD and Scope 3: Best Practices for Value Chain Reporting

Step 1: Set Your Operational Boundaries

Start by defining the boundaries of what you’re measuring. This involves pinpointing which parts of your value chain - both upstream and downstream - will be included in your emissions mapping. Focus on the segments that significantly contribute to emissions and align with CSRD compliance requirements. By clearly defining these boundaries, you’ll be better equipped to target the most impactful sources of emissions.

The 15 Scope 3 Categories Explained

The GHG Protocol breaks Scope 3 emissions into 15 categories that cover the entire lifecycle of a product, from raw material extraction to disposal.

- Upstream categories include activities like purchased goods and services, capital goods, upstream transport, waste generated during operations, and business travel.

- Downstream categories cover everything that happens after your product leaves your control, such as downstream transport, processing of sold products, use-phase energy consumption, end-of-life treatment, and investments.

"The Scope 3 Standard is the only internationally accepted method for companies to account for these types of value chain emissions." - GHG Protocol

For each client, identify which categories are most relevant. For instance, a manufacturing company might find that purchased goods and upstream transport dominate their emissions, while a financial services firm may need to focus on investments. The key is to systematically review all 15 categories and then narrow your focus to the ones that are most relevant to your operations.

Identify Your Highest-Impact Emissions Sources

Concentrate your reporting on categories that have a material impact. Start by using spend-based data and industry-average emission factors to identify high-impact areas or "hotspots." These are the categories where emissions are most concentrated and where your efforts will have the greatest effect.

"The goal is not to cover everything at once." - CarbonAccounting.uk

Once you’ve identified these high-impact categories, shift to collecting primary data - such as direct measurements from suppliers - for these specific areas. This ensures you’re audit-ready in the areas that matter most, while keeping the initial mapping process manageable. By focusing your resources on the most material categories, managing Scope 3 emissions becomes a more practical and effective process. For more insights, visit Managing Scope 3 emissions.

Step 2: Complete Your Double Materiality Assessment

Now it’s time to figure out which emissions sources are most relevant under CSRD. The double materiality approach outlined by CSRD requires you to assess two key aspects: the financial impact of emissions on your business and the effect your business has on the environment and society. When it comes to supply chain emissions, this means identifying which Scope 3 categories pose the biggest risks to your clients and prioritising those with the largest overall impact. This targeted evaluation connects your operational boundaries to actionable insights, laying the groundwork for what comes next.

Score Emissions Against CSRD Thresholds

Start by revisiting the 15 Scope 3 categories you identified in Step 1 and evaluate them against CSRD's materiality criteria. Since Scope 3 emissions often represent 70–90% of a company's total carbon footprint, it’s crucial to focus on high-impact areas like purchased goods and logistics, using the guidelines provided by the GHG Protocol. Your evaluation should cover two dimensions: impact materiality (how your client’s activities affect the climate and communities) and financial materiality (how climate risks could influence your client’s operations, reputation, or profitability). For instance, a manufacturing client that relies on suppliers with high carbon emissions may face regulatory challenges and reputational risks if those suppliers don’t decarbonise. Make sure to document your scoring process and supporting evidence for assurance purposes.

Automate Assessment Using Financial Data

Once you’ve completed the scoring, streamline the process by automating the assessment. Instead of manually gathering data from suppliers, use your clients’ financial transactions to estimate emissions. The spend-based calculation method is a practical approach: it multiplies spending in each category by average emission factors, giving you a quick way to pinpoint high-impact areas before requesting detailed data from suppliers.

Platforms like neoeco simplify this process by directly integrating with accounting tools like Xero, Sage, or QuickBooks. These tools map ledger transactions to the 15 Scope 3 categories, following standards such as the GHGP and ISO 14064. By automating spend-based estimates, the platform eliminates the need for spreadsheets and manual data handling. It also highlights materiality hotspots, making it easier to engage with suppliers where it matters most. This method, rooted in financial data, aligns with ISSB reporting principles and ensures your materiality assessment is both accurate and auditable.

Step 3: Gather and Organise Your ESG Data

With Scope 3 emissions accounting for over 70% of a business's carbon footprint, it's essential to take a methodical approach to collect data from suppliers, logistics partners, and other third parties. Start by focusing on the high-impact areas identified earlier, and work on gathering reliable data to calculate emissions in line with CSRD standards. This step builds on the groundwork laid during your assessments in Step 2.

Request Primary Data from Key Suppliers

Begin by reaching out to your most impactful suppliers - those flagged during your materiality assessment. Primary data is critical for achieving the accuracy and traceability required for audit-ready reporting, particularly in areas with significant emissions, such as manufacturing, freight, and raw materials. To streamline the process, create a standard data request template aligned with GHGP and ISO 14064 guidelines. Include key fields like measurement methods, emission factors, and uncertainty levels to ensure consistency and compliance with CSRD standards.

But don’t stop at simply sending out templates. Offer support to your suppliers by clarifying reporting requirements and providing guidance. You could even use tools like supplier scorecards or offer incentives such as favourable contract terms for those who consistently deliver accurate and timely data. This approach not only improves the quality of the data but also strengthens partnerships and underscores your commitment to reducing emissions across the value chain.

Use Financial Transactions to Automate Data Collection

While primary data is ideal, gathering it from every supplier can be challenging - especially for smaller transactions. For these cases, spend-based estimates can be a practical alternative. Simply multiply spending in a specific category (e.g., £50,000 spent on packaging) by average emission factors to generate quick estimates. This method allows you to cover all 15 Scope 3 categories and identify areas where primary data collection should be prioritised.

Platforms like neoeco can simplify this process by integrating directly with accounting tools like Xero, Sage, and QuickBooks. These tools map financial transactions to the 15 Scope 3 categories defined by the Greenhouse Gas Protocol, removing the need for manual spreadsheets and minimising the risk of errors. By combining spend-based data for broad coverage with activity-based data for high-impact areas, you can efficiently build a detailed emissions inventory. This financial integration ensures your data is complete, audit-ready, and backed by a clear link between financial records and carbon calculations.

Here’s a quick comparison of primary and spend-based data approaches:

| Factor | Primary Data (Activity-Based) | Secondary Data (Spend-Based) |

|---|---|---|

| Source | Supplier-specific measurements | Financial records and industry averages |

| Accuracy | High (specific and precise) | Moderate to low (based on assumptions) |

| Effort | High (requires supplier input) | Low (uses existing data) |

| Audit Readiness | Excellent (meets strict standards) | Limited (may need further validation) |

| Best Use Case | High-emission hotspots | Broad mapping of all Scope 3 categories |

Step 4: Calculate and Categorise Your Emissions

Once you've gathered your data, the next step is to convert it into measurable carbon emissions. This requires precise calculations that adhere to established standards like the GHG Protocol Corporate Value Chain Standard and ISO 14064. Using recognised emission factors tied to your financial records can simplify compliance and ensure accuracy, creating a solid foundation for the calculation and categorisation process.

Calculate Emissions for Each Scope 3 Category

The GHG Protocol outlines three main methods for calculating emissions: spend-based, activity-based, and hybrid. Here's how they work:

- Spend-based calculations: These use an average emission factor applied to financial spend (e.g., kg CO2e per £ spent). This method works well for initial assessments or less critical categories.

- Activity-based calculations: These rely on physical data, such as the weight of materials or litres of fuel used. They offer greater precision and are particularly useful for high-impact categories like Category 1 (Purchased Goods) or Category 4 (Upstream Transport).

- Hybrid approach: This combines supplier-specific data with spend estimates, offering a balance of coverage and accuracy. It's often the best choice for achieving detailed and reliable results.

Platforms like neoeco can automate this process by matching financial transactions from systems like Xero, Sage, or QuickBooks with the 15 Scope 3 categories. By integrating directly with your financial records, these tools ensure calculations align with the rigour of financial reporting.

| Scope 3 Category | Common Calculation Method | Data Source Examples |

|---|---|---|

| Cat 1: Purchased Goods | Hybrid (Supplier data + Spend) | Procurement records, supplier carbon reports |

| Cat 4: Upstream Transport | Activity-based (Distance/Weight) | Logistics logs, fuel usage from carriers |

| Cat 11: Use of Sold Products | Activity-based (Energy intensity) | Product specs, estimated usage hours |

| Cat 5: Waste in Operations | Activity-based (Waste type/Weight) | Waste management receipts, disposal method logs |

Verify Accuracy and Compliance

Once you've calculated your emissions, it's essential to verify their accuracy and ensure they meet audit standards. Verification involves confirming that all calculations are traceable and consistent, supported by a clear audit trail. This includes version control, change logs, and metadata like dates of creation and modification.

Start by cross-checking your emission factors against trusted databases such as UK DEFRA, US EPA, or ecoinvent. For spend-based methods, make sure the emission factors are appropriate for the specific industry or product category. For activity-based data, verify supplier figures with supporting documents like energy bills, logistics records, or waste disposal receipts.

Automation tools can help minimise errors. For instance, neoeco offers features that identify inconsistencies or deviations from expected patterns, ensuring data is categorised correctly under GHG Protocol and ISO 14064 standards. By linking carbon data to your financial records, these tools provide a transparent, science-backed approach that meets CSRD's audit requirements. This method, known as Financially-integrated Sustainability Management (FiSM), ensures your emissions data is as dependable and verifiable as your financial accounts.

Step 5: Document, Review, and Submit Your Report

The final step in producing a CSRD-compliant report is ensuring your documentation is thorough and audit-ready. Strong documentation is the backbone of reliable sustainability disclosures. External reviewers must be able to trace every emission figure back to its source with clear evidence. This level of transparency not only ensures compliance but also sets the stage for ongoing improvements in data quality.

Building CSRD-Compliant Reports

A CSRD-compliant report should include a detailed double materiality assessment, clearly define relevant Scope 3 categories, and differentiate between primary and secondary data sources. Aligning your reporting with established frameworks like the Greenhouse Gas Protocol for emissions classification and ISO 14064 for technical verification is crucial.

Make sure to highlight any limitations in your data, such as the use of spend-based estimates, and explain why these methods were necessary. This transparency helps maintain trust with regulators and stakeholders. Tools like neoeco offer pre-structured templates designed for CSRD compliance. These templates can pull data directly from financial systems like Xero, Sage, or QuickBooks, making it easier to produce audit-ready reports.

| Documentation Category | Required Evidence | Retention Period |

|---|---|---|

| Stakeholder Identification | Contact lists, relationship mapping, materiality justification | 7 years |

| Engagement Planning | Methodologies, timelines, framework alignment documents | 7 years |

| Survey/Interview Data | Questionnaires, transcripts, attendance logs, consent forms | 7 years |

| Validation Evidence | Cross-checks, discrepancy resolutions, approval records | 7 years |

| Change Management | Version logs, modification records, approval workflows | 7 years |

To maintain an audit trail, apply strict version control for all data modifications. Secure senior-level approval using digital signatures before submission, and ensure all final data is validated by a director. Use centralised systems that allow auditors secure, controlled access to your documentation.

Enhancing Data Quality Over Time

Submitting your first CSRD report is just the beginning. Use it as a baseline to refine your processes for future reporting. Over time, aim to improve the quality of your data. For example, cross-check supplier responses against public records or previously collected data to identify inconsistencies. Where secondary data was used this year, collaborate with key suppliers to secure primary data for the next reporting cycle, especially in high-impact areas like purchased goods or upstream transport.

Regularly reviewing data with suppliers and standardising collection templates can help streamline the process and improve accuracy. Incorporating these steps into your annual compliance calendar reduces the workload while ensuring steady progress in data reliability. Platforms like neoeco can assist by tracking improvements in data quality, flagging areas where estimates are still in use, and identifying suppliers that require closer engagement.

Conclusion

Tracking supply chain emissions for CSRD compliance can be straightforward when approached systematically. By focusing on five key steps - setting boundaries, assessing materiality, gathering data, calculating emissions, and documenting findings - you can transform compliance into a strategic opportunity. It’s worth noting that Scope 3 emissions often account for over 70% of a company’s total carbon footprint, so prioritising the most significant categories is a smart starting point.

For accounting firms handling multiple clients, relying on manual spreadsheets quickly becomes impractical. Tools like neoeco simplify the process by integrating with platforms like Xero, Sage, and QuickBooks. This integration automates the mapping of transactions to established emissions categories under GHGP and ISO 14064 standards. The result? No more manual data entry, fewer errors, and audit-ready reports produced in days instead of weeks.

Compliance templates are kept up to date for CSRD, SECR, and UK SRS regulations, ensuring your clients stay aligned with shifting requirements. With full traceability from transactions to final reports, auditors can easily access clear and consistent evidence. Standardised data templates further enhance accuracy and efficiency.

To get started, use spend-based data for an initial baseline, then gradually shift to activity-based data for more precise reporting. This step-by-step approach makes sustainability reporting manageable for businesses of all sizes, from SMEs to larger private firms. Not only does this improve accuracy, but it also gives firms a competitive edge under CSRD guidelines. Curious about the benefits of financially-integrated sustainability management? Learn more here and see how it can future-proof your clients and your practice.

FAQs

What are the key challenges in mapping Scope 3 emissions for CSRD compliance?

Mapping Scope 3 emissions for CSRD compliance isn’t straightforward. The main hurdle? The data comes from sources beyond a company’s direct control. Suppliers often provide incomplete or inconsistent information, making it tough to create a reliable, audit-ready dataset. On top of that, the wide range of Scope 3 categories - like purchased goods, product use, and end-of-life - means data needs to be collected from multiple points across the value chain, adding even more layers of complexity.

A key decision companies face is choosing between primary data (supplier-specific) and secondary data (industry averages or estimates). Primary data offers greater accuracy and traceability but demands considerable time and resources to gather. On the other hand, secondary data is quicker and easier to access, but it’s less precise and might not meet the CSRD’s strict audit standards. Finding the right balance between these two approaches is crucial.

Another challenge lies in integrating emissions data into a single, verifiable system. Relying on manual processes, like spreadsheets, increases the risk of errors and makes it harder to prove compliance. Automation tools, such as neoeco, offer a solution by linking emissions data directly to financial transactions. This not only improves accuracy but also ensures the reporting is scalable and audit-ready.

What is double materiality, and how does it affect supply chain emissions reporting under CSRD?

Double materiality, a core element of the EU Corporate Sustainability Reporting Directive (CSRD), requires businesses to evaluate two critical aspects: their environmental and social impacts, and the financial risks these impacts pose to the organisation. This dual perspective shifts supply chain emissions, often referred to as Scope 3 emissions, from a peripheral issue to a central focus in sustainability reporting.

For accounting firms, this means a broader approach to data collection. They need to account for high-impact suppliers - those whose activities result in notable environmental or social consequences, as well as those posing material financial risks. To achieve this, precise mapping of transactions to established emissions categories, such as those outlined by the Greenhouse Gas Protocol (GHGP) or ISO 14064, is crucial. By embedding double materiality into their processes, firms can deliver audit-ready Scope 3 inventories that not only comply with regulations but also enhance risk management and reveal pathways for sustainable growth.

What are the advantages of using spend-based data for calculating initial supply chain emissions?

Using spend-based data, which taps into the value of purchases recorded in a company’s financial ledger, offers a fast and cost-efficient method to estimate Scope 3 emissions. Since this information is already stored in accounting systems, businesses can establish a baseline without the hassle of sourcing detailed, supplier-specific activity data - something that’s often tricky to obtain. This approach helps accountants pinpoint major emission hotspots, lay the groundwork for gathering more precise data later on, and confidently meet early CSRD reporting deadlines.

By automatically linking spend transactions to recognised emissions factors (like GHGP or ISO 14064), this method removes the need for manual spreadsheets, cutting down on errors and seamlessly integrating carbon metrics into financial reporting. Tools such as neoeco simplify the process further by transforming every pound spent into reliable, audit-ready carbon data. This makes adhering to frameworks like CSRD, SECR, and UK SRS both straightforward and efficient.