How LCA Supports Scope 1, 2, and 3 Reporting

Life Cycle Assessment (LCA) is a method that evaluates the environmental impact of a product or service throughout its entire life cycle. It’s particularly useful for organisations aiming to measure and report greenhouse gas (GHG) emissions under Scope 1, 2, and 3 categories as defined by the Greenhouse Gas Protocol (GHGP). By using detailed data, LCA helps pinpoint where emissions occur, improving precision in reporting and compliance with frameworks like ISSB, SECR, and CSRD.

Key points:

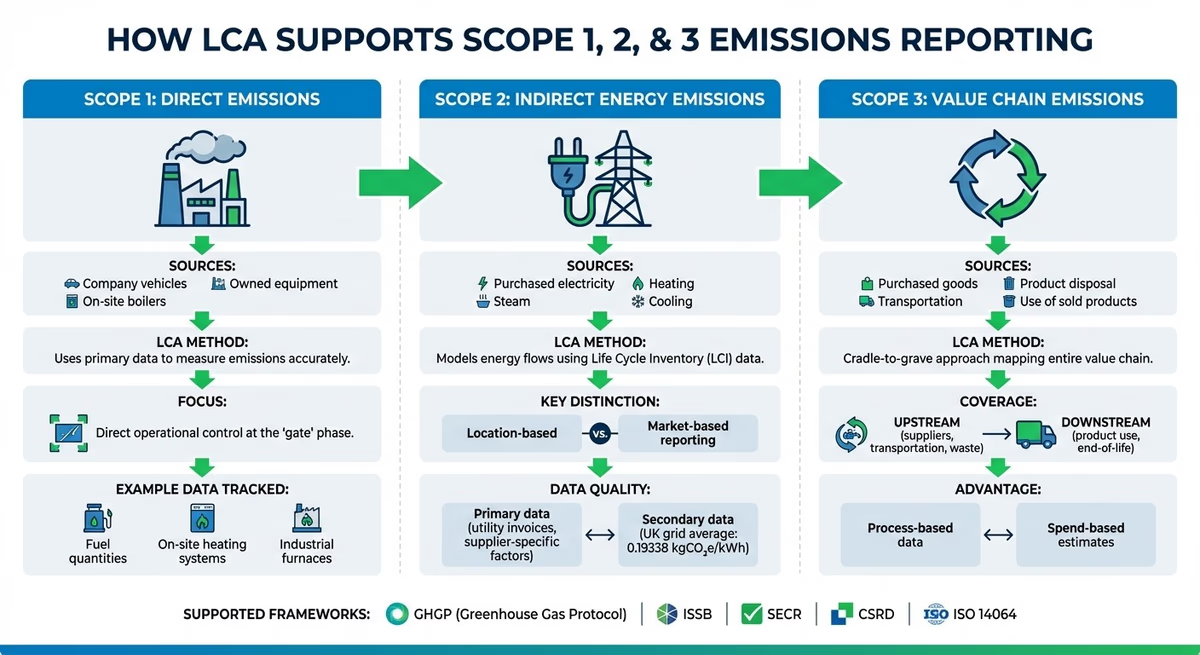

- Scope 1: Direct emissions from owned or controlled sources (e.g., company vehicles, on-site boilers). LCA uses primary data to measure these emissions accurately.

- Scope 2: Indirect emissions from purchased energy (e.g., electricity). LCA models energy flows and distinguishes between renewable and non-renewable sources.

- Scope 3: Indirect emissions across the value chain (e.g., purchased goods, transportation, product disposal). LCA maps these emissions using a cradle-to-grave approach for detailed insights.

LCA integrates seamlessly into emissions reporting frameworks, offering a science-based method to improve data accuracy, identify emission hotspots, and align with global standards for carbon reporting.

How LCA Supports Scope 1, 2, and 3 Emissions Reporting Framework

How LCA Supports Scope 1 Emissions Reporting

Measuring Direct Emissions

Life Cycle Assessment (LCA) provides a detailed, science-backed way to monitor energy and material flows at every step of a process - key for compiling accurate Scope 1 emissions inventories. Instead of relying on estimates, LCA uses primary data directly from company-controlled operations. This involves tracking specific quantities of fuel used by company-run vehicles, on-site heating systems like gas boilers, and industrial furnaces.

For manufacturing, LCA captures precise data on energy consumption and the materials used in production. It also monitors the release of greenhouse gases during chemical production or other industrial processes carried out in owned equipment. This method pinpoints specific "hotspots" in operations where resources are being wasted, enabling precise reduction strategies. Comprehensive LCA databases support the accurate measurement of materials, energy, transport, packaging, and waste.

This robust tracking system forms the foundation for integrating LCA into broader emissions management frameworks.

Cradle-to-Gate Boundaries

In addition to measuring direct emissions, cradle-to-gate analysis refines the scope of operational control. This approach examines emissions from raw material extraction all the way to the completion of production and distribution. For Scope 1 reporting, the focus is on the "gate" phase - the transformation stage where the company has direct operational control.

Carbon and compliance: The Scope 1–3 strategy for impact and ESG alignment

How LCA Supports Scope 2 Emissions Reporting

Scope 2 emissions refer to indirect emissions from purchased energy, such as electricity, steam, heating, and cooling. Unlike Scope 1 emissions, which occur directly at an organisation's site, Scope 2 emissions are generated offsite at the facilities of energy suppliers. Life Cycle Assessment (LCA) helps organisations monitor and report these emissions by modelling energy flows and assessing the environmental impact throughout the entire energy supply chain.

LCA achieves this by using Life Cycle Inventory (LCI) data, which captures the energy sources within a grid mix and the proportion of renewable versus non-renewable energy contributing to purchased electricity. By combining precise energy consumption data from utility bills with accurate emission factors, LCA shifts reporting from rough estimates to highly detailed calculations. This level of precision is essential for meeting requirements like the UK's Streamlined Energy and Carbon Reporting (SECR), which mandates large companies to disclose their energy use and related greenhouse gas emissions. Such detailed reporting also helps organisations distinguish between primary and secondary data in their Scope 2 calculations.

Primary vs Secondary Data in Scope 2 Reporting

The quality of Scope 2 reporting largely depends on whether the data used is primary or secondary. Primary data is sourced directly from energy suppliers and includes metered readings, utility invoices, or supplier-specific emission factors tied to an organisation's actual energy contract. Secondary data, on the other hand, relies on national or regional averages, such as the UK's 2023 grid average of 0.19338 kgCO₂e per kWh.

| Factor | Primary LCA Data | Secondary Data |

|---|---|---|

| Source | Directly measured from utility providers or on-site meters | Based on national/regional grid averages |

| Accuracy | High – reflects the specific energy mix purchased | Moderate to Low – uses generalised assumptions |

| Traceability | High – linked to specific contracts and invoices | Lower – less specific to actual energy consumed |

| Audit Readiness | Excellent – meets strict standards like ISSB reporting and CSRD | Limited – requires further validation |

| Impact | Captures specific improvements in energy procurement | Misses organisation-specific improvements |

"Primary data is (highly) specific and accurate raw data that's directly collected/measured from main sources." – Ecochain

Using primary data ensures that renewable energy procurement is accurately reflected, rather than relying on general grid averages. This distinction is crucial for demonstrating real progress in reducing carbon emissions. The following section explains how energy source modelling can enhance Scope 2 reporting further.

Energy Source Modelling

LCA provides a detailed evaluation of grid emissions, distinguishing between renewable sources like wind and solar, and non-renewable sources such as coal and natural gas. This enables organisations to use two reporting methods: location-based and market-based.

- The location-based method relies on the national average grid mix, reflecting the physical carbon intensity of the local power grid, regardless of the energy supplier or tariff.

- The market-based method uses supplier-specific data or "residual mix" data to account for the emissions tied to the electricity an organisation chooses to purchase, such as green tariffs supported by Renewable Energy Guarantees of Origin (REGOs). Residual mix data adjusts for renewable energy claims, ensuring no double-counting of green energy.

For transparency, organisations should report both location-based and market-based Scope 2 emissions. If supplier-specific data isn’t available for market-based reporting, residual mix factors should be used instead of the national average to avoid underestimating emissions.

How LCA Supports Scope 3 Emissions Reporting

Life Cycle Assessment (LCA) has already proven its value in tackling Scopes 1 and 2 emissions. Now, it’s stepping up to address the intricate challenges of Scope 3 emissions.

Scope 3 emissions are notoriously difficult to measure because they fall outside an organisation's direct control. They cover everything from extracting raw materials to the disposal of products. LCA simplifies this complexity by taking a cradle-to-grave approach, mapping the entire value chain. This method evaluates environmental impacts from the sourcing of materials all the way to the product’s end-of-life. Unlike activity vs spend-based methods, LCA uses process data to identify specific suppliers, materials, or processes that are driving emissions the most.

This level of detail allows organisations to move beyond compliance and take proactive steps to cut emissions. For instance, by tracking a shift from diesel to electric vehicles, businesses can set realistic targets and measure progress effectively. Such insights are vital for managing Scope 3 emissions across intricate supply chains.

Mapping Value Chain Emissions

LCA offers a complete view of emissions by analysing both upstream and downstream activities. Upstream activities include things like purchased goods and services, capital goods, fuel-related activities, transportation, and waste generated during operations. Downstream activities focus on product processing, the use of sold products, and their eventual disposal or recycling.

Instead of relying solely on financial spending data, LCA digs deeper, using detailed information about product components and processes to calculate emissions. This approach helps organisations pinpoint emission hotspots, such as energy-intensive manufacturing processes from specific suppliers. By combining primary data from suppliers with secondary LCA database information, it ensures accuracy . This comprehensive mapping helps organisations align Scope 3 categories with specific LCA stages, paving the way for targeted interventions.

Scope 3 Categories and LCA Stages

Each Scope 3 category corresponds to a particular stage of the LCA framework, enabling businesses to focus their efforts where they can make the most impact. This alignment provides actionable insights, helping organisations prioritise areas with the greatest environmental and financial benefits. Here’s how LCA stages connect to common Scope 3 categories:

| Scope 3 Category | Relevant LCA Stage | Key Insights Provided by LCA |

|---|---|---|

| Purchased Goods & Services | Raw Material Acquisition / Production | Identifies high-impact materials and supplier-specific process efficiencies |

| Capital Goods | Production | Tracks emissions tied to manufacturing machinery and infrastructure |

| Upstream Transportation | Transportation & Distribution | Evaluates the impact of logistics choices (e.g., electric vs. diesel vehicles) and route efficiency |

| Waste Generated in Operations | End-of-Life / Waste Management | Measures the environmental impact of disposal methods like landfill vs. recycling |

| Use of Sold Products | Use Phase | Calculates energy and resource consumption during the product’s functional life |

| End-of-Life Treatment | Disposal / Recycling | Highlights the benefits of circular business models and recyclability |

Integrating LCA into Scope 1-3 Reporting Frameworks

Incorporating Life Cycle Assessment (LCA) into Scope 1-3 reporting frameworks can significantly enhance the accuracy and reliability of your emissions data. By aligning LCA practices with established standards like the Greenhouse Gas Protocol (GHGP) and ISO 14064, organisations can integrate these methods into existing systems without requiring a complete overhaul. This approach ensures compliance while focusing on greenhouse gas (GHG) emissions reporting.

The integration is effective because Scope 3 GHG accounting essentially represents a specific application of LCA - narrowed down to greenhouse gas emissions rather than a broader environmental impact analysis. This makes it possible to apply LCA’s detailed value chain analysis within the confines of carbon reporting requirements. For organisations with intricate supply chains, this method provides the clarity needed to pinpoint emission hotspots without overloading the process with extraneous data.

Steps for Integrating LCA

To bridge the gap between data collection and compliance, follow these key steps:

- Define goals and scope: Align your LCA boundaries with GHGP's Scope categories. For Scopes 1 and 2, a cradle-to-gate boundary is typically sufficient, covering direct emissions and purchased energy. Clearly define your functional unit - whether it applies to a product, service, or corporate activity - and specify which GHGs you’ll track (usually CO2e).

- Collect life cycle inventory (LCI) data: Quantify inputs and outputs for each stage of the lifecycle. For Scopes 1 and 2, rely on primary data such as fuel bills, electricity invoices, and direct operational measurements. For Scope 3, combine primary supplier data with secondary sources like Environmental Product Declarations (EPDs) or LCA databases. The GHGP Product Standard lets you focus on major emitters, avoiding the need for exhaustive inventories of every product or activity.

- Convert LCI data into CO2e: Use appropriate Global Warming Potential (GWP) factors, ensuring you document the source and date of these factors to meet GHGP standards. This step helps identify emission hotspots across your value chain, whether in raw material extraction, manufacturing, or product use.

- Interpret and report results: Disclose any exclusions, assumptions about data quality, and the reasoning behind your boundary decisions. Incorporate product-level LCA findings into your corporate Scope 3 calculations and ensure biogenic and non-biogenic emissions are reported separately as required. For organisations aligning with ISSB reporting, this phase is crucial in demonstrating the financial implications of climate-related risks.

Common Challenges and Solutions

While LCA integration offers clear advantages, it also presents practical challenges, particularly in data collection and consistency.

- Incomplete Scope 3 data: This is a frequent issue. Begin with high-impact categories, such as purchased goods or upstream transportation, and disclose any exclusions. The GHGP allows organisations to prioritise key emission sources and use averaged data where primary data isn’t available, as long as exclusions are clearly documented. Over time, expand your coverage to include more categories.

- Data quality issues: Many organisations face errors when relying on manual spreadsheets or generic accounting software, which often lack the specificity needed for emissions mapping. Specialised platforms can solve this by automating the connection between financial transactions and emissions categories. For example, neoeco simplifies this process by integrating directly with financial ledgers, mapping transactions to recognised emissions categories under GHGP and ISO 14064. This eliminates manual conversions and makes Scope 3 tracking a seamless extension of financial processes. Learn more about Scope 3 emissions.

- Overly complex LCAs: For carbon reporting, there’s no need to assess every environmental impact - just GHG emissions. This focus streamlines the process. Use hybrid methods, combining primary data for direct operations with secondary data for upstream and downstream activities. As your data collection improves, gradually shift towards more primary data to enhance precision and meet audit requirements.

- System boundary subjectivity: Inconsistent boundaries across reporting periods can undermine credibility. Address this by clearly documenting your boundary decisions from the outset, referencing GHGP and ISO 14064 guidance. If boundaries need to change due to business expansion or regulatory updates, document the reasoning and adjust prior periods where material differences occur. This transparency builds trust with auditors and stakeholders while ensuring consistent reporting over time.

Conclusion

Life Cycle Assessment (LCA) plays a crucial role in ensuring accurate carbon reporting, particularly when dealing with Scopes 1, 2, and 3 emissions. It provides the scientific framework needed to address data gaps, especially in Scope 3 reporting, where estimates often fall short. By shifting from spend-based to activity-based data, LCA enables precise, traceable emissions reporting - exactly what frameworks like ISSB and CSRD now demand. This level of accuracy turns vague estimates into dependable carbon accounts that can withstand scrutiny.

Traditional tools like spreadsheets or generic accounting software simply can’t handle the complexity of mapping financial transactions to specific emissions categories. That’s where specialised platforms step in. neoeco, for example, integrates seamlessly with financial systems like Xero, Sage, and QuickBooks. This automation links financial transactions directly to recognised emissions categories under frameworks like the Greenhouse Gas Protocol (GHGP) and ISO 14064, cutting out manual errors and ensuring compliance with standards like ISSB reporting, SECR, and UK SRS.

By combining LCA with financial systems, businesses gain more than compliance - they unlock strategic insights. For accounting firms, this is a game-changer. Embedding LCA principles into your clients' financial processes allows you to go beyond compliance, offering actionable insights to identify emissions hotspots, monitor progress, and drive reductions. This approach, known as Financially-integrated Sustainability Management, bridges the gap between finance and sustainability, helping future-proof both your clients and your practice.

The outcome? Carbon reporting that not only meets regulatory demands but also supports smarter decision-making. By focusing on high-impact areas and using primary data, your firm can deliver clear, actionable insights while positioning itself as a leader in sustainability advisory.

FAQs

How does life cycle assessment (LCA) enhance the accuracy of Scope 1 emissions reporting?

Life cycle assessment (LCA) plays a key role in improving the precision of Scope 1 emissions reporting. It provides a thorough, science-driven analysis of the direct emissions linked to an organisation's operations. By pinpointing areas with high emissions and ensuring accurate data collection, LCA gives businesses a clearer picture of their direct greenhouse gas (GHG) emissions.

This method ensures that reporting adheres to established frameworks, producing dependable, audit-ready data that aids in meeting compliance requirements and advancing sustainability objectives.

What is the difference between primary and secondary data in Scope 2 emissions reporting?

When it comes to Scope 2 emissions reporting, primary data refers to information gathered directly from specific sources, like electricity meter readings or energy supplier invoices. This type of data is highly precise and directly linked to the actual energy consumed, making it more reliable and traceable.

In contrast, secondary data relies on estimates or generalised figures when direct measurements aren't accessible. Examples include regional grid averages or industry-standard benchmarks. While secondary data can fill in the gaps, primary data is typically the better choice due to its accuracy and dependability.

How does life cycle assessment (LCA) help organisations manage Scope 3 emissions effectively?

Life cycle assessment (LCA) offers organisations a science-based approach to navigating the complexities of Scope 3 emissions. It evaluates environmental impacts throughout a product’s entire lifecycle - starting from raw material extraction and ending with disposal. Given that Scope 3 emissions often form the bulk of a company’s carbon footprint and are tied to intricate supply chains, LCA provides precise, activity-specific insights to enhance both accuracy and reliability.

By pinpointing emissions hotspots within value chains, LCA helps organisations work more closely with suppliers, streamline processes, and meet the requirements of frameworks such as the GHG Protocol, CSRD, and ISSB. Additionally, automation tools that integrate with LCA can make tasks like data collection, validation, and tracking more straightforward, enabling organisations to better manage and reduce their Scope 3 emissions.