How To Conduct a Double Materiality Assessment

Nov 16, 2025

Learn how to effectively conduct a double materiality assessment, connecting sustainability impacts with financial outcomes for better decision-making.

Double materiality assessments help organisations understand two perspectives: how they affect the world and how the world affects them. This approach evaluates impact materiality (e.g., carbon emissions, labour practices) and financial materiality (e.g., risks or opportunities affecting cash flow). It’s a method that connects sustainability and financial priorities, improving transparency and decision-making.

Key Steps:

Plan: Define scope, align with reporting standards, and map stakeholders.

Collect Data: Use existing financial and operational data to quantify impacts.

Assess Impacts: Apply frameworks like GHGP or SECR to evaluate material topics.

Prioritise: Create a materiality matrix to identify top issues.

Report: Document findings and meet regulatory requirements (e.g., CSRD, ISSB).

Tools like neoeco can simplify the process by linking sustainability metrics to financial data, ensuring compliance and audit readiness. Regular reviews keep assessments relevant and aligned with evolving regulations.

Why it matters: Double materiality helps organisations address sustainability risks and opportunities while improving accountability to stakeholders.

How to Run a Double Materiality Assessment | CSRD & ESRS Aligned Double Materiality | Socialsuite

Step 1: Planning Your Double Materiality Assessment

Getting your double materiality assessment right starts with solid planning. This phase is all about defining the boundaries of your organisation, understanding your stakeholders, and figuring out the data you'll need. Essentially, you're creating the roadmap that will guide the entire assessment process.

Setting Scope and Objectives

Start by outlining the scope of your assessment. This means defining geographical boundaries, operational areas, and the parts of your value chain you’ll include. Remember, it’s not just about your direct operations. For instance, a manufacturing company might find that most of its emissions come from the materials it buys, not the energy it uses.

Your scope should align with the relevant reporting standards. If you're preparing for CSRD compliance, you’ll need to address the sustainability topics detailed in the European Sustainability Reporting Standards. On the other hand, ISSB reporting will require a focus on sustainability risks and opportunities that could influence your company’s value.

"One system for all rules neoeco keeps up with GHGP, SECR and UK SRS, and more so you never have to learn new frameworks."

– neoeco

It’s also vital to connect financial and sustainability data. Using platforms that integrate with your financial systems – whether it’s Xero, Sage, QuickBooks, or a more advanced ERP – can simplify the process by building sustainability metrics directly from your financial data.

Once your scope is clear, the next step is mapping your stakeholders to ensure you capture a range of perspectives on material issues.

Mapping Your Stakeholders

Map out all your stakeholders, both internal (like the board and senior management) and external (such as customers, suppliers, local communities, and regulators). Using an influence-interest matrix can help you prioritise who to engage with more closely. For example, major investors with a strong focus on ESG or industry regulators will likely need direct involvement throughout the process.

Think about how and when to engage each group. Some stakeholders may prefer formal surveys, while others might respond better to workshops or one-on-one interviews. For instance, UK pension funds often send ESG questionnaires to the companies they invest in, offering valuable insights for your assessment.

Keep track of each stakeholder group’s key concerns and preferred communication methods. For example, a local community near your factory might be concerned about air quality and noise, while institutional investors could be more focused on climate-related risks and transition strategies.

Once you’ve identified your stakeholders and their concerns, the next step is to gather the data needed to quantify these impacts.

Gathering Initial Data

Begin with the data you already have. Look at your financial and operational records, such as ledgers, accounts payable, and procurement systems, to understand where your organisation is spending money across different categories.

Operational data is key for calculating impacts. Collect information on energy use, water consumption, waste generation, employee demographics, supplier details, and even customer satisfaction scores. Linking this non-financial data to your financial transactions will give you a complete picture for your assessment.

Benchmarking against industry standards can also provide valuable context. Review materiality assessments from your sector, reports from industry associations, and guidance from regulators to understand how your impacts compare.

"We evaluated multiple ESG tools and felt more confused each time. neoeco cut through the noise - the only platform that connects financials to sustainability with LCA-level accuracy."

– neoeco

Automation can be a game-changer here. By linking transactions to sustainability metrics, you’ll improve accuracy and be better prepared for audits. Make sure your data aligns with recognised frameworks like GHGP, SECR, and UK SRS to stay on track for compliance. Centralising all your data - whether it’s client, project, or numerical information - can help you avoid the chaos of juggling multiple spreadsheets and provide a solid base for your assessment.

Finally, think about how your data collection will support Scope 3 emissions calculations. These indirect emissions often represent a large portion of environmental impacts, especially in service-driven industries.

Step 2: Finding and Evaluating Material Impacts

Now that your planning is sorted, the next step is to identify and assess the sustainability issues that could have a major influence on your organisation or society. This involves using the right tools and frameworks to evaluate these potential material topics effectively.

Using Frameworks and Benchmarks

Frameworks are essential for evaluating material topics tied to your operations. For instance, the Greenhouse Gas Protocol (GHGP) is a widely used tool for measuring and managing greenhouse gas emissions. It breaks emissions into three categories: Scope 1 (direct emissions), Scope 2 (indirect emissions from electricity use), and Scope 3 (emissions from the value chain). This breakdown helps organisations understand and address their climate-related impacts more thoroughly.

For organisations in the UK, frameworks like the Streamlined Energy and Carbon Reporting (SECR) and the UK Sustainability Reporting Standards (UK SRS) are particularly relevant. These tools not only help in evaluating energy and carbon emissions but also ensure compliance with reporting requirements.

Another valuable approach is the Life Cycle Assessment (LCA) methodology. This tool evaluates environmental impacts throughout a product's entire life cycle - from raw material extraction to disposal. It provides a comprehensive view, making it easier to assess the severity and likelihood of various impacts as you move forward in the process.

Step 3: Building and Reading the Materiality Matrix

After evaluating your material impacts using the frameworks and benchmarks from Step 2, the next step is to create a materiality matrix. This visual tool helps you identify which topics matter most to your organisation and its stakeholders, serving as a guide for prioritising sustainability efforts and resource allocation.

Creating the Materiality Matrix

Once you've quantified your material impacts, it's time to map them out. The matrix is built by plotting your identified topics on two axes: financial materiality (how these topics affect your organisation's financial performance) and impact materiality (how your organisation affects people and the environment). The goal is to combine financial data with sustainability metrics, ensuring both dimensions are well-represented.

Use the horizontal axis to represent financial impact, such as effects on revenue, costs, or overall performance.

The vertical axis reflects sustainability impact, including effects on people and the environment.

For each topic, assign scores based on stakeholder feedback and internal evaluations. These scores determine where each topic sits on the matrix. Topics that land in the upper right quadrant (high on both axes) indicate your top priorities, while those in the lower left quadrant (low on both axes) may require less immediate focus.

To make this process seamless, integrate your financial data with sustainability metrics using tools like Xero, Sage, or QuickBooks. When building your matrix, consider using report builders or live dashboards that update in real time as new data becomes available. This dynamic setup allows you to track changes in your materiality landscape and adjust your priorities accordingly.

Understanding the Results

Interpreting your materiality matrix is key to making informed decisions about where to focus your sustainability efforts. The matrix doesn’t just show what matters - it highlights why it matters, helping you prioritise actions effectively.

High-priority topics appear in the upper right quadrant, where both financial and impact materiality scores are high. These are areas where your organisation has a significant effect on people or the environment and where sustainability performance directly influences financial outcomes. For example, UK companies might focus on energy efficiency initiatives that cut carbon emissions and operating costs, especially given rising energy prices and SECR reporting requirements.

Topics with high impact materiality but lower financial materiality still demand attention. These include areas like community engagement or biodiversity projects, which may not have immediate financial returns but are crucial for maintaining your organisation's social licence to operate.

The lower right quadrant highlights topics with high financial materiality but lower impact materiality. These could involve regulatory compliance costs or supply chain risks that significantly affect finances without a direct environmental or social impact. These areas often represent business risks that require careful management.

High scores on both axes indicate urgent priorities, while uneven scores suggest areas for targeted action based on either financial risk or stakeholder impact. For organisations aiming to meet ISSB reporting standards, the matrix is an essential tool for linking sustainability risks and opportunities to financial performance. It validates stakeholder insights gathered earlier and provides a clear direction for reporting and planning next steps. This matrix becomes the cornerstone of your reporting and action strategy.

Step 4: Reporting and Next Steps

With your materiality matrix finalised and priorities set, it’s time to turn your assessment into actionable documentation while ensuring you meet regulatory requirements. This step determines if your double materiality assessment can effectively support sustainability reporting.

Recording the Assessment Process

Keep detailed records of every decision and stakeholder input to ensure you're prepared for audits. These records should include decision points, chosen methodologies, and stakeholder contributions that influenced the results. A single, well-organised document capturing your methodology, scoring criteria, and engagement process will simplify audit readiness.

Start by crafting a comprehensive methodology document. This should outline your approach to scoring both impact and financial materiality, referencing frameworks like GRI standards or SASB metrics. Be sure to explain how these frameworks were tailored to your organisation’s needs.

"I found the Policy Builder extremely useful at our stage because having a template of a well-conceived policy helps in the standardisation of new practices and ensures that written guidelines are best-in-class." - Jennifer Kaplan, Sustainability Manager

Data reconciliation plays a key role in connecting sustainability impacts to financial performance. By integrating sustainability data directly with your existing financial systems, you can utilise already verified numbers, streamlining the process.

Store all compliance-related files - such as stakeholder feedback forms, scoring worksheets, research materials, and external verification reports - in a secure, centralised location. This ensures easy access and continuous audit readiness.

Before finalising your documentation, validate your findings with leadership to align on the results and gain approval for the next steps.

Checking and Presenting Results

Present your materiality matrix to leadership, linking high-priority topics to business performance. Focus on the upper right quadrant of the matrix to highlight areas with both significant sustainability impacts and financial relevance.

Develop professional, branded reports that feature clear charts and concise commentary. Using your organisation’s logo and colours ensures a polished presentation, making complex materiality relationships easier to understand for non-technical audiences, such as board members or external stakeholders.

Consider using live dashboards to share real-time updates. These tools allow stakeholders to monitor progress as new data becomes available, making it easier to adapt strategies as needed. Dashboards can also display progress across multiple reporting frameworks simultaneously, which is especially helpful for organisations juggling diverse compliance requirements.

To stay organised, use checklists to track the status of tasks - whether they’re completed, in progress, or pending review. This method ensures no steps are overlooked and provides a clear overview of your progress.

Once your results are presented, align them with the relevant reporting standards to complete the assessment process.

Meeting Reporting Standards

Using the data and insights gathered earlier, regulatory compliance involves clearly linking material sustainability topics to financial performance. For example, your double materiality assessment can form the basis for IFRS S1 and S2 disclosures, identifying how sustainability risks and opportunities impact your organisation’s financial position. Explore how ISSB reporting integrates with financial strategies to connect sustainability data with financial performance metrics.

For CSRD compliance, UK companies affected by EU regulations must demonstrate that their assessment addresses both impact and financial materiality. Detailed documentation of your methodology, stakeholder engagement, and integration of material topics into your sustainability strategy will serve as essential evidence.

UK-specific regulations, such as SECR (Streamlined Energy and Carbon Reporting) and alignment with UK Sustainability Reporting Standards (SRS), can be managed using systems that automatically stay updated with reporting rules. This automation reduces the learning curve for teams and ensures your assessment aligns with required disclosures while maintaining consistency across various standards.

Your assessment results should seamlessly integrate into annual reports, sustainability reports, and any sector-specific documentation. For organisations with complex supply chains, be sure to address Scope 3 emissions and social impacts throughout your value chain. Learn more about aligning your Scope 3 emissions management approach with the material topics identified in your assessment.

Finally, treat your double materiality assessment as a dynamic tool. Regular reviews - either annually or when significant business changes occur - will help keep your material topics relevant and reflective of your organisation’s evolving risks and impacts.

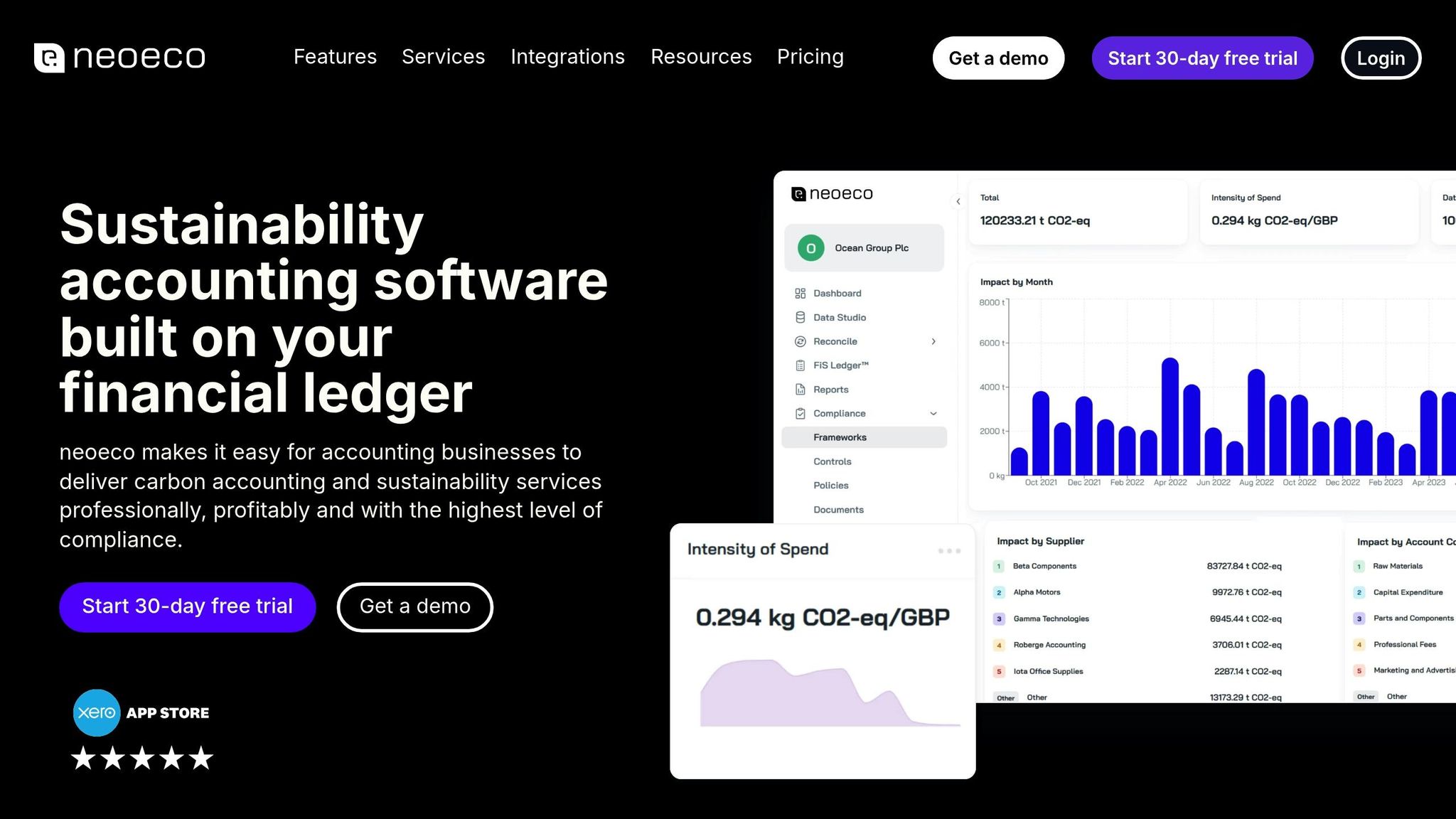

Using neoeco for Financial and Sustainability Data Integration

Integrating financial and sustainability data is crucial for effective double materiality assessments. These assessments demonstrate how environmental and social impacts tie directly to business performance. Yet, relying on disconnected spreadsheets and manual data entry can disrupt audit readiness and compliance.

This is where neoeco steps in. The Financially-integrated Sustainability Management (FiSM) platform merges sustainability reporting with your existing financial ledger. By doing so, it creates a unified view that links impact and financial materiality, rather than treating ESG data as a separate entity.

How neoeco Supports Double Materiality Assessments

neoeco simplifies double materiality assessments with its Smart matching feature, which automates data connections to deliver accurate and audit-ready metrics.

The platform integrates with financial tools like Xero, Sage, and QuickBooks, ensuring sustainability metrics are grounded in verified financial data. It consolidates all client, project, and numerical data into one central hub, eliminating the need for spreadsheets and providing ready-to-use documentation for audits.

For UK organisations juggling various reporting frameworks, neoeco ensures compliance with standards such as the Greenhouse Gas Protocol (GHGP), Streamlined Energy and Carbon Reporting (SECR), and UK Sustainability Reporting Standards (UK SRS). The platform generates reports tailored to these frameworks, sparing teams from mastering the technical specifics of each. This consistency ensures double materiality assessments meet current regulatory expectations without constant adaptation.

neoeco also offers robust audit-ready controls, including a policy and evidence hub that stores compliance files and provides auditors with easy access to supporting documentation.

"I found the Policy Builder extremely useful at our stage because having a template of a well-conceived policy helps in the standardisation of new practices and ensures that written guidelines are best-in-class." - Jennifer Kaplan, Sustainability Manager

The platform’s professional reporting tools quickly produce clear, integrated performance metrics, making it easier to communicate complex materiality insights to board members and external stakeholders.

Benefits for Accounting Firms and CFO Teams

neoeco’s features bring tangible advantages for both accounting firms and CFO teams. For accounting firms, the platform opens doors to sustainability advisory services while maintaining the compliance standards clients expect. It enables firms to handle carbon accounting and sustainability reporting with the same precision applied to financial reporting.

For CFO teams, neoeco bridges sustainability data with financial planning and analysis. This alignment supports the financially-integrated sustainability management approach required for modern double materiality assessments, connecting material topics directly to business performance metrics.

Tailored for UK accounting firms, neoeco caters to SMEs, large private companies, and organisations reporting under voluntary standards. By leveraging existing financial systems, teams can manage sustainability reporting seamlessly, avoiding workflow disruptions or the need for extensive retraining.

Real-time dashboards offer insights into emissions and performance trends, supporting continuous updates to materiality assessments. This feature is especially useful for organisations with complex supply chains, enabling them to track Scope 3 emissions and related social impacts across their value chains.

Additionally, neoeco generates branded client reports with professional formatting, ensuring consistent presentation of materiality findings across annual reports, sustainability disclosures, and sector-specific documents.

Conclusion: Main Points for Double Materiality Assessment

To wrap up the key steps for an effective double materiality assessment, it all comes down to thoughtful planning, engaging stakeholders, and combining financial and sustainability data seamlessly.

Start by defining a clear scope and setting precise objectives. Then, map out your stakeholders to ensure you capture a wide range of perspectives on your organisation’s environmental and social impacts. This step is crucial for understanding the broader implications of your operations.

The next step is to evaluate impacts thoroughly. Use established frameworks to assess the severity and likelihood of these impacts. This quantitative approach not only ensures compliance with regulations but also makes the assessment more grounded in measurable outcomes. Stakeholder input adds another layer, ensuring the results align with real-world expectations and concerns.

A materiality matrix is a useful tool here, helping to link sustainability priorities directly to financial performance. It’s a visual way to highlight what matters most.

Document everything - methodologies, stakeholder feedback, and data sources. This keeps your organisation audit-ready, meeting both UK and international standards. It also lays the groundwork for future assessments, showing a commitment to continuous improvement in sustainability.

One of the most impactful developments is the integration of financial and sustainability data. By adopting a financially-integrated sustainability management approach, organisations can align ESG metrics with financial performance, creating a more cohesive strategy.

For UK-based accountants, using specialised platforms can eliminate the risks tied to manual data handling by directly connecting with financial systems. Regular updates to these insights ensure compliance with changing regulations and evolving stakeholder expectations. This transforms the assessment from a mere compliance exercise into a strategic tool for guiding sustainable investments and managing risks.

It’s important to remember that double materiality assessments aren’t a one-off task. Organisations that embed these into their ongoing strategic planning can build stronger sustainability strategies and foster deeper relationships with stakeholders.

Ultimately, this process becomes a strategic compass, enabling organisations to act decisively in the face of shifting market and regulatory demands. Done right, it provides the solid evidence needed for confident and informed sustainability management.

FAQs

What is the difference between impact materiality and financial materiality in a double materiality assessment?

Impact materiality looks at the ripple effects an organisation's actions have on the world around it - whether that's the environment, society, or other external groups. This perspective digs into areas like carbon emissions, biodiversity loss, or issues of social fairness, highlighting the broader consequences of business activities.

Financial materiality, in contrast, zooms in on how sustainability-related factors impact an organisation's financial outcomes. This could include things like shifting regulations, changing market demands, or dwindling resources - anything that might influence revenue, costs, or the value of assets.

A double materiality assessment brings these two views together. It ensures organisations consider their external impacts while also keeping an eye on the risks and opportunities that could shape their financial future.

How can organisations keep their double materiality assessments relevant and aligned with changing regulations?

To keep double materiality assessments relevant and aligned with changing regulations, organisations should focus on regular updates and active stakeholder engagement. This means revisiting materiality factors periodically to account for shifts in regulatory requirements, market dynamics, and societal expectations.

Accurate and current data collection plays a crucial role in understanding both financial and sustainability impacts. Organisations should align their reporting efforts with globally recognised standards like ISSB (IFRS S1 & S2) and CSRD to ensure compliance and maintain trustworthiness.

Platforms like neoeco, a Financially-integrated Sustainability Management (FiSM) tool, can make this process more straightforward. By integrating financial and sustainability data, automating reporting, and ensuring adherence to key standards, such tools equip organisations to navigate an ever-changing regulatory landscape with confidence.

What is the role of stakeholders in a double materiality assessment, and how can organisations engage them effectively?

Stakeholders are essential to a double materiality assessment, offering valuable perspectives on both the financial implications and the environmental, social, and governance (ESG) impacts of an organisation's actions. Their feedback helps pinpoint the issues that matter most to the business and its responsibilities towards society and the environment.

To engage stakeholders effectively, organisations can:

Identify key groups: These might include investors, employees, customers, suppliers, and local communities.

Use methods like surveys, interviews, or workshops to understand their views.

Ensure transparent communication about how their input will influence decisions and reporting.

By involving stakeholders in this way, organisations can create a more thorough assessment that meets both regulatory demands and stakeholder expectations.