UK SRS vs ASRS 2: Data Format Differences Explained

Nov 17, 2025

Explore the key differences between UK SRS and ASRS 2 reporting standards, focusing on data formatting, compliance, and regional climate risks.

UK SRS and ASRS 2 are sustainability reporting standards used in the UK and Australia, respectively. While both aim to improve climate-related disclosures, they differ in how data is formatted and reported. Here's what you need to know:

UK SRS: Focuses on integrating sustainability data into financial reporting. Requires emissions data (Scopes 1, 2, and 3), financial impacts, and governance details in pounds sterling (£). Standard templates ensure uniformity.

ASRS 2: Emphasises machine-readable formats, industry-specific disclosures, and local climate risks (e.g., bushfires). Allows more flexibility in templates and includes detailed transition plans.

Quick Comparison

Feature | UK SRS | ASRS 2 |

|---|---|---|

Currency | Pounds sterling (£) | Australian dollars (A$) |

Template Style | Uniform templates | Flexible, industry-specific templates |

Climate Risks | Global focus | Local risks (e.g., bushfires, floods) |

Transition Plans | Standard documentation | Detailed milestones and resources |

Scenario Analysis | General scenarios | Australian-specific scenarios |

Key takeaway: Firms working across both regions must adjust systems to handle these differences. Automated platforms like neoeco simplify compliance by aligning data formats and generating audit-ready reports for both frameworks.

Understanding UK Sustainability Reporting Standards (ISSB Adoption)

UK SRS Data Format Requirements

The UK SRS framework outlines specific guidelines for how data should be formatted to ensure compliance. These go beyond simple emissions calculations, requiring structured data collection that aligns with financial reporting standards.

Required Data Elements under UK SRS

To meet UK SRS standards, organisations need to capture and format a range of data elements according to strict guidelines. A key focus is on climate-related metrics, such as Scope 1, 2, and 3 emissions measured in tonnes of CO₂ equivalent.

Reports must also quantify the financial impacts of climate risks, provide detailed transition costs, and include scenario analyses. All financial data must be presented in pounds sterling (£), using correct decimal and thousand separators for clarity.

Additionally, governance and strategy aspects must be documented to demonstrate how climate-related risks and opportunities are integrated into organisational decision-making. Forward-looking data - such as science-based targets, transition plans, and resilience assessments - should be presented with clear timelines, measurable milestones, and indicators to track progress.

Finally, organisations should consider the industry-specific codes that help refine data categorisation under UK SRS.

Required Industry Codes

Industry classification is another critical component of UK SRS compliance. While the specific codes are not publicly detailed, sustainability accounting software typically handles these classifications automatically. This ensures organisations are categorised correctly and that their data aligns with the required standards.

These classifications feed directly into the templates used for submitting data, streamlining the reporting process.

Standard Templates and Frameworks

UK SRS relies on standardised templates to ensure consistent and accurate data submissions. Organisations already reporting under frameworks like the Streamlined Energy and Carbon Reporting (SECR) framework can often adapt their existing data structures to meet UK SRS requirements.

Automated compliance platforms play a vital role here, structuring data to fit these templates and reducing the risk of manual errors. For example, neoeco’s approach allows these platforms to stay aligned with frameworks like GHGP, SECR, and UK SRS. This lets accounting firms focus on improving data quality rather than worrying about technical compliance.

ASRS 2 Data Format Requirements

Australia's ASRS 2 framework introduces specific data format rules that differ from the UK's SRS requirements. For organisations managing dual reporting obligations, understanding these differences is critical. Below is an outline of the key disclosure fields required under ASRS 2.

Required Disclosure Fields in ASRS 2

ASRS 2 requires entities to report both financial and non-financial climate-related information in machine-readable formats. This includes:

Quantitative data such as Scope 1, 2, and 3 emissions (measured in tonnes of CO₂ equivalent), energy consumption figures, and the financial effects of climate risks.

Qualitative disclosures covering governance, strategy, and risk management practices. This also includes scenario analyses, which must be presented in standardised tables with detailed assumptions and methodologies clearly documented.

Entities are also expected to provide scenario analysis outcomes in a structured format, outlining financial impacts under different climate scenarios. These disclosures must be transparent, with the assumptions and methodologies used clearly stated.

Additionally, metrics and targets related to climate performance play a key role. Organisations must demonstrate measurable progress against science-based targets, ensuring the information provided is actionable for stakeholders evaluating climate-related financial risks and opportunities.

Industry-Based Disclosure Approach

ASRS 2 employs an industry-specific disclosure approach, allowing organisations to customise certain disclosures based on the climate risks and opportunities most relevant to their sector. While the framework does not mandate the use of SASB Standards, it encourages referencing industry best practices and provides recommended templates and examples.

This flexibility acknowledges the unique climate challenges faced by different industries. However, it can create complexities for accounting firms working with clients across multiple sectors. Collecting and standardising data for diverse industries often requires adaptable systems to maintain consistency and ensure audit readiness.

Differences from IFRS S2 Baseline

Although ASRS 2 aligns broadly with IFRS S2 standards, it includes notable deviations that impact data formatting. These differences stem from Australia's local regulatory requirements and climate context.

For example, transition plan disclosures under ASRS 2 demand more detailed documentation than IFRS S2. Organisations must provide specific milestones, resource allocation details, and progress indicators. The framework also emphasises the Australian context for scenario analysis, urging entities to consider local climate risks such as bushfires, flooding, and extreme weather events - factors that may not be as relevant elsewhere.

These variations pose practical challenges for multinational companies reporting under multiple frameworks. Organisations operating in both Australia and the UK must adjust their data collection and formatting processes to meet global baseline requirements while addressing the additional Australian-specific elements.

To navigate these complexities, firms need systems capable of managing multiple frameworks simultaneously. Learn more about our approach to managing Scope 3 emissions in real-time with automated compliance platforms that ensure data consistency and maintain audit trails across regions. These tools are essential for meeting the demands of dual reporting obligations, as explored further in the next section.

Key Data Format Differences Between UK SRS and ASRS 2

Expanding on the earlier discussion about data element requirements, this section takes a closer look at the format differences between the two frameworks. Companies will encounter variations in how major data categories - like emissions, financial impacts, governance disclosures, transition planning, and industry classifications - are reported. While some frameworks stick to a more uniform data presentation, others allow for sector-specific adjustments.

Reporting Template Similarities and Differences

Both the UK SRS and ASRS 2 frameworks share an emphasis on machine-readable formats, but their approaches to templates and presentation differ. UK SRS leans towards a uniform format, ensuring consistent data presentation across all reporting entities. On the other hand, ASRS 2 offers more flexibility, allowing templates to be adapted to reflect the specific risks and requirements of different sectors. Additionally, the documentation and audit trail requirements vary between the two frameworks, setting the stage for operational challenges that firms must navigate.

Impact on Accounting Firms

These differences in templates have a direct effect on the challenges accounting firms face. Dual reporting requirements increase the demand for resources and call for specialised training. Manual processes not only raise the risk of errors but also complicate the creation of reliable audit trails. However, integrated platforms can simplify compliance by linking financial data with sustainability metrics and offering built-in audit controls.

Technology plays a crucial role in overcoming these hurdles. Platforms that integrate with financial systems like Xero, Sage, or QuickBooks ensure consistent reporting across frameworks. Tools such as automated data formatting also make it easier to communicate with clients, helping accounting firms confidently address the differing requirements of UK SRS and ASRS 2.

Managing Dual Compliance: Practical Solutions

Accounting firms face the challenge of accurately reporting sustainability data across multiple frameworks. Navigating the differences in data formats between UK SRS and ASRS 2 can be tricky, but with the right strategies and tools, compliance can be handled efficiently while keeping audit readiness intact.

Handling Data Format Differences

The key to managing dual compliance lies in centralising data collection right from the source. By integrating financial ledgers like Xero, Sage, or QuickBooks, firms can streamline data collection, avoiding duplicate data streams. This method ensures sustainability data is derived directly from financial records, minimising discrepancies between frameworks.

Automated mapping tools are essential here. They convert financial data into the required formats for each framework, addressing the challenge of matching identical business activities to differing reporting requirements under UK SRS and ASRS 2. This eliminates the need for manual intervention, saving time and reducing errors.

Using platforms that support multiple reporting standards within a single system can simplify the process even further. A "one system for all rules" approach means firms don’t have to learn separate frameworks for each standard, and it reduces data duplication across various requirements.

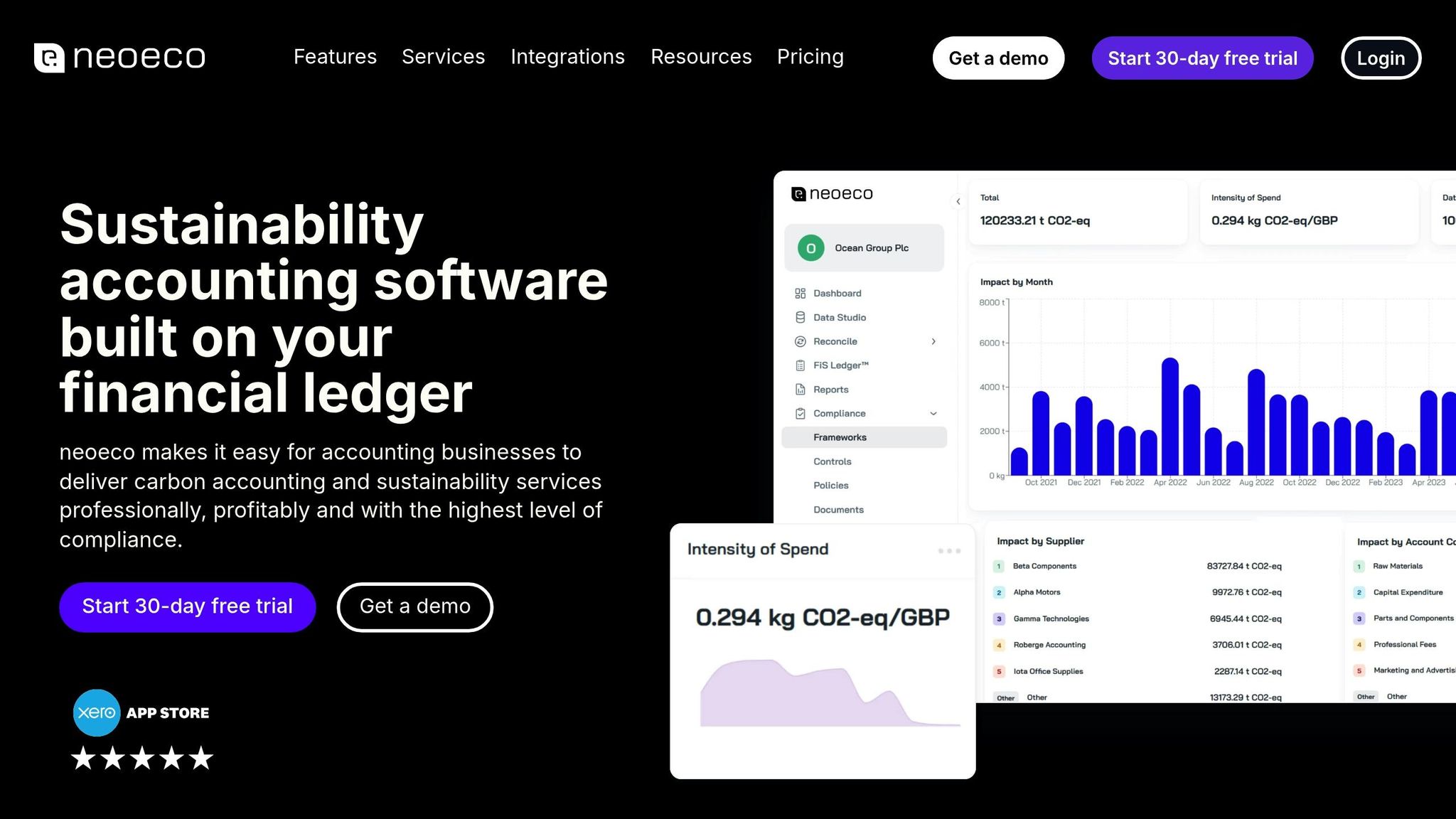

How neoeco Automates Compliance

neoeco takes automation a step further, making dual compliance easier for firms. The platform directly pulls sustainability data from clients’ existing financial ledgers, connecting seamlessly with tools like Xero, Sage, and QuickBooks. This eliminates the need for manual data entry, saving valuable time.

neoeco’s smart matching feature maps ledger entries to Scope 1, 2, and 3 emissions under frameworks like GHGP and ISO 14064. This ensures accuracy when dealing with the specific data format requirements of both UK SRS and ASRS 2.

With compliance-ready templates, neoeco generates reports tailored for UK SRS and ASRS 2 in just minutes. These templates handle format differences automatically, producing professional, branded reports complete with charts and figures. This makes meeting diverse reporting requirements straightforward and efficient.

For firms managing multiple clients, neoeco offers a centralised dashboard that consolidates all carbon and sustainability data. This approach aligns with a financially-integrated sustainability management philosophy, ensuring reporting is based on verified financial data while meeting the unique requirements of each framework.

Maintaining Audit-Ready Compliance

To stay audit-ready across dual frameworks, systematic tracking and evidence management are essential. Audit-ready controls help firms monitor tasks, identify gaps, and flag items for review, ensuring continuous compliance. These controls work hand-in-hand with data mapping to provide a unified approach to managing dual compliance.

Centralised evidence hubs are another crucial tool. They securely store compliance files, policies, and supporting documentation in easily accessible digital repositories. This ensures firms are always prepared for audits, with organised and verifiable audit trails for both UK SRS and ASRS 2.

Modern compliance platforms simplify the audit process even further by offering secure, direct access to reports and evidence. This reduces administrative burdens while maintaining security and data integrity.

Additionally, built-in report builders and policy templates help firms standardise their reporting practices across different standards. This reduces manual effort and ensures consistent, professional results every time.

You can explore neoeco with a 30-day free trial, available on flexible monthly plans.

Conclusion: Managing UK SRS and ASRS 2 Compliance

Bringing together the strategies we've explored, managing compliance with both UK SRS and ASRS 2 requires a clear, streamlined approach that balances accuracy and efficiency. The key lies in reconciling the differences between these frameworks while leveraging the right systems to simplify the process.

Key Points to Remember

One of the most important steps is establishing a single source of truth for your sustainability data. By integrating with financial tools like Xero, Sage, and QuickBooks, you can ensure consistency and avoid the pitfalls of manual data entry.

Automation plays a vital role in addressing the format differences between UK SRS and ASRS 2. Tools with smart matching capabilities can automatically connect financial transactions to the correct emissions categories, saving time and reducing the risk of errors. This ensures that business activities are represented accurately across both frameworks.

For audit-ready compliance, it's crucial to maintain systematic tracking and centralised evidence. Features like evidence hubs and built-in audit controls make it easier to provide documentation and explain calculation methods when auditors come knocking. This level of preparation is invaluable for meeting the requirements of both frameworks.

An integrated system simplifies training, reduces data duplication, and ensures consistent reporting. These benefits not only address current challenges but also pave the way for adapting to future standards.

Preparing for Future Reporting Standards

The world of sustainability reporting is changing fast, and businesses must adopt tools and processes that can keep up. Platforms that update automatically to reflect new standards help firms stay compliant without the need for constant manual adjustments or additional training.

This proactive approach ties back to the earlier discussion on managing diverse regulatory demands. Integrated sustainability reporting isn't just a trend - it's the future. By building sustainability metrics directly from financial data, firms can prepare for the evolving standards and align with the growing focus on financially-integrated strategies that bridge traditional accounting with sustainability reporting.

Platforms like neoeco exemplify this approach, offering support for multiple frameworks within a single system. With automatic updates for both UK and Australian compliance requirements, these tools allow firms to concentrate on client value rather than getting bogged down in technical compliance work. Plus, their seamless integration with financial systems ensures that sustainability reporting becomes a natural extension of everyday accounting practices.

As reporting standards shift towards greater integration, firms that invest in the right technology today will be better equipped for tomorrow. By choosing platforms that address current needs while anticipating future demands, accounting firms can build practices that not only meet regulatory requirements but also grow alongside their clients and the broader industry landscape.

FAQs

How can organisations comply with both UK SRS and ASRS 2 reporting requirements effectively?

Navigating the gap between UK SRS and ASRS 2 reporting standards can feel like a daunting task, especially when juggling the demands of dual compliance. These frameworks often require different data formats, which makes precision and uniformity absolutely critical.

neoeco takes the stress out of this process by automatically aligning financial transactions with recognised emissions categories under standards like UK SRS and ASRS 2. By directly integrating with financial data, it eliminates the hassle of manual data conversions or spreadsheet wrangling. This streamlined approach ensures compliance is not only efficient but also free from errors, allowing accounting firms to confidently produce accurate, audit-ready sustainability reports.

How can automation simplify managing data format differences between UK SRS and ASRS 2?

Automation is crucial for managing the challenges posed by the differing data formats of UK SRS and ASRS 2. With neoeco, transactions are automatically aligned with recognised emissions categories, ensuring they meet the standards of frameworks like GHGP, ISO 14064, SECR, UK SRS, and ASRS 2.

By replacing spreadsheets and manual data conversions, neoeco provides precise, finance-grade carbon data and reports that are audit-ready. This approach not only saves time but also minimises the risk of errors, enabling accounting firms to handle sustainability reporting with greater ease and reliability.

Why should firms address local climate risks in their sustainability reporting, and how do these considerations vary between the UK and Australia?

Tackling local climate risks is a crucial part of sustainability reporting. It ensures companies consider the specific environmental challenges and regulatory demands of the regions they operate in. For instance, in the UK, sustainability reporting often centres around frameworks like the UK SRS and SECR. These frameworks focus on key areas such as carbon emissions, energy consumption, and aligning with the country's net-zero targets.

In contrast, Australian reporting tends to highlight issues like water scarcity, bushfires, and extreme heat - climate risks that are particularly pressing in that region. These differences underline the importance of tailoring reports to address region-specific priorities while maintaining compliance with local regulations.

For companies operating in both countries, this dual compliance can be streamlined with tools like neoeco. By integrating directly with financial data, neoeco maps transactions to recognised frameworks such as UK SRS and ASRS 2. This not only simplifies the reporting process but also ensures the creation of accurate, audit-ready reports that reflect local climate concerns - without the need for tedious manual adjustments. It’s an efficient way to meet diverse regulatory requirements while staying focused on regional environmental priorities.