CSRD and ISSB: Bridging Global ESG Standards

ESG reporting is no longer optional. Businesses must now navigate two major sustainability frameworks: the CSRD (Corporate Sustainability Reporting Directive), which applies in the EU, and the ISSB (International Sustainability Standards Board), which sets global benchmarks. Here’s what you need to know:

- CSRD requires reporting under double materiality, covering both a company’s impacts on society and the environment, and how sustainability issues affect its financial performance.

- ISSB focuses only on financial materiality, providing data relevant to investors and creditors.

- These frameworks align on financial materiality, making it easier for companies reporting under CSRD to also comply with ISSB standards, particularly for climate-related disclosures.

- A joint guidance issued in May 2024 ensures minimal duplication of effort for companies managing both standards.

For businesses, understanding the scope, timelines, and requirements of these frameworks is vital. The CSRD applies broadly across the EU, with phased implementation starting from the 2024 financial year. Meanwhile, the ISSB’s global standards serve as a baseline for sustainability-related financial disclosures.

Key takeaway: CSRD and ISSB are designed to complement each other, reducing the reporting burden for companies operating across multiple jurisdictions. By leveraging their alignment, organisations can streamline ESG reporting efforts while meeting both regional and global expectations.

1. CSRD (Corporate Sustainability Reporting Directive)

Materiality Approach

One of the standout features of the CSRD is its double materiality framework. This means organisations must report on two aspects: impact materiality - how their operations affect people and the planet - and financial materiality - how sustainability issues pose risks or create opportunities for the business. The definition of financial materiality under the ESRS has been updated to align with the ISSB's approach. Mark Vaessen, Chair of KPMG's Global Corporate & Sustainability Reporting Topic Team, explained:

"Companies should take confidence that the ISSB and EFRAG have agreed on common areas of their climate-related disclosures and highlighted significant alignment."

Now, let’s look at how broadly the CSRD applies across different types of organisations.

Scope and Coverage

The CSRD casts a wide net, applying to large multinationals, listed SMEs, and even emerging startups. It builds on earlier EU sustainability reporting requirements, offering investors and stakeholders a much more detailed view of a company’s environmental and social impacts, which can be assessed using an ESG compliance checker, along with the financial risks posed by climate change. This widened scope is rolled out in phases, which we’ll break down next.

Implementation Timelines

The first wave of companies under the CSRD started collecting data for the 2024 financial year, with their ESRS-compliant reports due in 2025. Commissioner Mairead McGuinness confirmed this timeline, stating:

"The first companies in scope of the Corporate Sustainability Reporting Directive (CSRD) will report against the ESRS in 2025 for the financial year 2024."

To simplify the process, the European Commission introduced a "quick fix" in December 2025 for the first wave of companies and received technical advice for a scaled-down ESRS tailored to SMEs. A stabilised version of this standard for listed SMEs was released on 2 December 2025. These staggered timelines are crucial for businesses aiming to prepare for both CSRD and ISSB reporting.

Alignment and Interoperability

The ESRS has been designed to align closely with the ISSB’s global baseline. A joint guidance document released on 2 May 2024 by EFRAG and the ISSB ensures that companies reporting under the ESRS can meet ISSB climate requirements with minimal additional work. This collaboration strengthens the connection between EU-specific and global reporting standards. However, businesses should pay particular attention to differences in areas like GHG emissions disaggregation and assumptions used in transition plans versus scenario analysis.

2. ISSB (International Sustainability Standards Board)

Materiality Approach

The ISSB takes a different route from the CSRD by focusing solely on financial materiality. Its aim is to provide investors with data about how sustainability risks and opportunities directly affect a company’s financial performance over various time periods. This approach simplifies reporting for businesses by aligning the financial aspects of the CSRD with the ISSB framework, cutting down on duplication. Let’s dive into how the ISSB framework is structured.

Scope and Coverage

The ISSB framework revolves around two key standards: IFRS S1 (General Requirements) and IFRS S2 (Climate-related Disclosures). Additionally, it incorporates SASB standards to provide sector-specific metrics. Compared to the CSRD’s broader scope - spanning 12 sector-neutral standards covering a wide range of ESG topics - the ISSB keeps its focus tighter. While the CSRD is a mandatory EU directive addressing diverse stakeholder needs, the ISSB acts as a voluntary global baseline. Despite these differences, both frameworks align on financial materiality, ensuring consistency in this area.

Alignment and Interoperability

The ESRS integrates the ISSB baseline, making it easier for companies to meet global reporting requirements without significant extra effort. In May 2024, EFRAG and the ISSB issued joint guidance to streamline compliance for climate-related reporting. This means businesses can use a single dataset to satisfy multiple jurisdictions, as long as they include the EU’s required "impact materiality" layer.

There’s also ongoing discussion about "equivalence." The European Commission is exploring whether combining ISSB and GRI standards could meet ESRS requirements. This collaboration not only simplifies dual compliance but also strengthens the global alignment of ESG reporting standards. For a deeper dive into how ISSB reporting can enhance a financially integrated strategy, explore the ISSB vs. CSRD data mapping differences.

Navigating Sustainability Reporting: ESRS and ISSB Explained

Advantages and Disadvantages

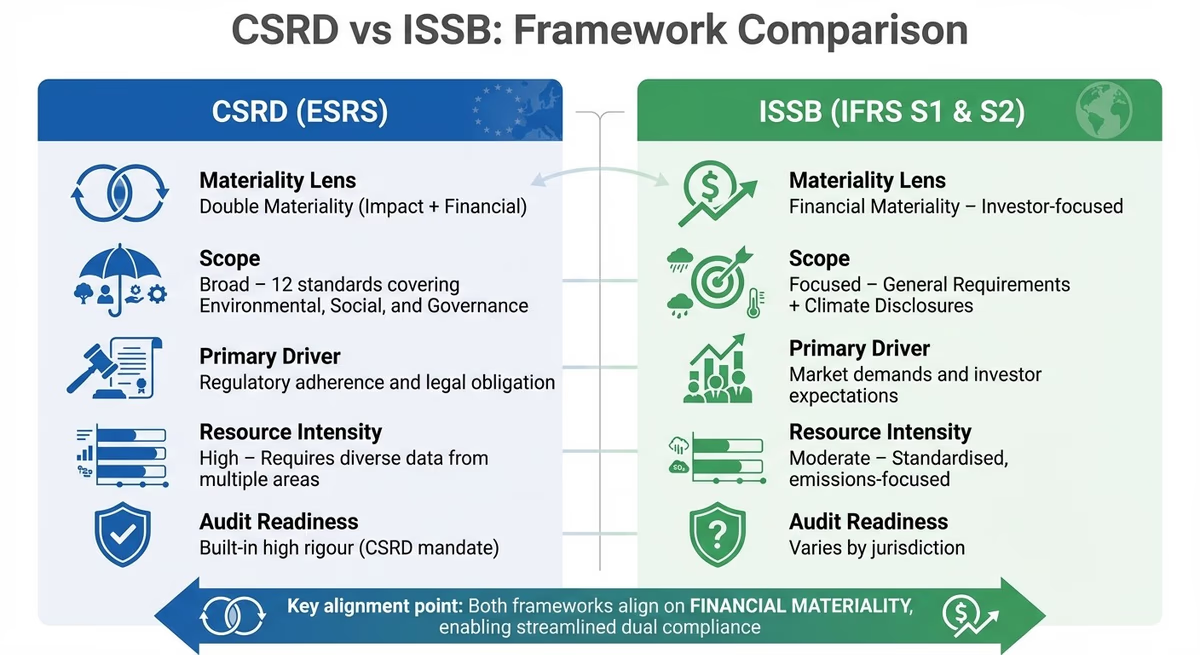

CSRD vs ISSB: Key Differences in ESG Reporting Frameworks

Each framework brings its own strengths and challenges, especially for accountants tasked with navigating dual compliance. The CSRD's double materiality approach vs. ISSB standards offers a more thorough view of ESG transparency, addressing both financial and broader societal impacts. While this approach benefits a wide range of stakeholders, it also demands substantial cross-departmental collaboration, which can stretch resources.

The ISSB framework, on the other hand, focuses on financial materiality, delivering standardised and comparable data tailored to investors. By concentrating on general requirements (IFRS S1) and climate disclosures (IFRS S2), it simplifies reporting. However, its narrower focus doesn't fully address the broader societal and environmental impacts that the CSRD captures.

| Aspect | CSRD (ESRS) | ISSB (IFRS S1 & S2) |

|---|---|---|

| Materiality Lens | Double Materiality (Impact + Financial) | Financial Materiality (Investor-focused) |

| Scope | Broad (12 standards: E, S, and G) | Focused (General + Climate) |

| Primary Driver | Regulatory adherence and legal obligation | Market demands and investor expectations |

| Resource Intensity | High (Requires diverse data from multiple areas) | Moderate (Standardised, emissions-focused) |

| Audit Readiness | Built-in high rigour (CSRD mandate) | Varies; depends on jurisdiction |

This table underscores the balancing act accountants face: capturing comprehensive data for the CSRD while meeting the investor-focused precision of the ISSB.

One practical benefit is the interoperability of these frameworks. Their alignment makes dual compliance more manageable. In many cases, starting with the ESRS is a smart move, as it already incorporates the ISSB baseline while addressing additional ESG topics. For organisations aiming to integrate financial and sustainability data effectively, exploring financially-integrated sustainability management can reduce duplicate data efforts.

The biggest challenge, however, is resource allocation. The CSRD's detailed requirements demand extensive coordination across departments, offering clear legal goals but at a high operational cost. Meanwhile, the ISSB's more flexible approach can create variability as investor expectations evolve. To navigate these complexities, accountants can rely on the joint guidance set for release in May 2024. This guidance will help identify overlapping requirements and minimise redundant work.

Conclusion

The interplay between CSRD and ISSB presents a practical and strategic way forward for businesses navigating sustainability reporting. These frameworks are not at odds but instead complement each other: CSRD prioritises stakeholder transparency through double materiality assessment, while ISSB zeroes in on investor-focused financial materiality. For accountants handling clients across multiple jurisdictions, the good news is that these frameworks are designed to work in harmony. As Mairead McGuinness, Commissioner for Financial Services at the European Commission, aptly stated:

"It is important that reporting frameworks in different jurisdictions are interoperable with each other to reduce the reporting burden for EU companies".

This interoperability is not just an aspirational goal; it’s embedded into the frameworks themselves. For example, the concept of financial materiality is aligned between ESRS and ISSB. Companies reporting under ESRS E1 (Climate Change) often find that they’ve already addressed most of ISSB's IFRS S2 climate disclosure requirements with minimal additional effort. This alignment helps businesses avoid duplicating data collection efforts or maintaining separate reporting systems.

A strong data infrastructure is key to navigating these frameworks effectively. Tools like neoeco simplify the process by automatically mapping financial transactions to recognised emissions categories under standards like GHGP, ISO 14064, SECR, and UK SRS. By integrating seamlessly with platforms such as Xero, Sage, or QuickBooks, these tools eliminate manual data conversions and errors, while producing audit-ready reports that comply with both CSRD and ISSB requirements. This kind of integration makes the dual reporting process far more manageable.

Starting with overlapping areas - such as climate disclosures and GHG emissions - and then expanding to include CSRD's additional social and governance elements can significantly ease the resource burden while ensuring compliance.

Ultimately, treating ESG data with the same level of precision and integration as financial reporting transforms compliance into a strategic advantage. With the right systems in place, managing CSRD and ISSB requirements becomes less of an administrative challenge and more of an opportunity to strengthen organisational resilience and transparency.

FAQs

What distinguishes the CSRD from the ISSB reporting frameworks?

The Corporate Sustainability Reporting Directive (CSRD) and the International Sustainability Standards Board (ISSB) frameworks serve different purposes and operate under distinct principles, making them stand apart in terms of focus, scope, and regulatory approach.

The CSRD is an EU regulation with legal authority, requiring companies to report on double materiality. This means organisations must disclose not only the financial risks they face but also their broader impact on society and the environment. It applies to a wide range of businesses operating within the EU and is designed to inform regulators, local communities, and other stakeholders. On the other hand, the ISSB framework is a voluntary global standard. It emphasises single materiality, focusing solely on sustainability-related financial risks and opportunities, tailored primarily for investors.

While there is growing alignment between the two frameworks when it comes to climate-related disclosures, the CSRD's detailed ESG reporting requirements and its enforceable nature distinguish it from the ISSB's more flexible, investor-focused approach. Essentially, the CSRD targets comprehensive compliance within the EU, whereas the ISSB caters to global financial markets.

How do the CSRD and ISSB standards work together to streamline ESG reporting?

The CSRD (Corporate Sustainability Reporting Directive) and ISSB (International Sustainability Standards Board) work together to streamline ESG reporting for businesses. Their collaboration ensures that essential areas, like climate-related disclosures, are based on consistent principles. This approach minimises redundancy and simplifies the process for companies adhering to both frameworks.

By aligning these standards, organisations can address both global and EU-specific sustainability requirements more efficiently. This shared framework allows businesses to create detailed, reliable ESG reports that meet multiple regulatory expectations without requiring significant extra effort.

When will the CSRD and ISSB standards take effect?

The rollout of the ISSB standards is set to align with the European CSRD timelines, with phased adoption anticipated to start in early 2026 across both the UK and EU. Initial ISSB standards were published back in June 2023, with additional guidance on interoperability expected to follow throughout 2024 and 2025.

This synchronisation is designed to make compliance easier for organisations working across various jurisdictions, promoting consistency between global ESG reporting frameworks and those specific to the EU.