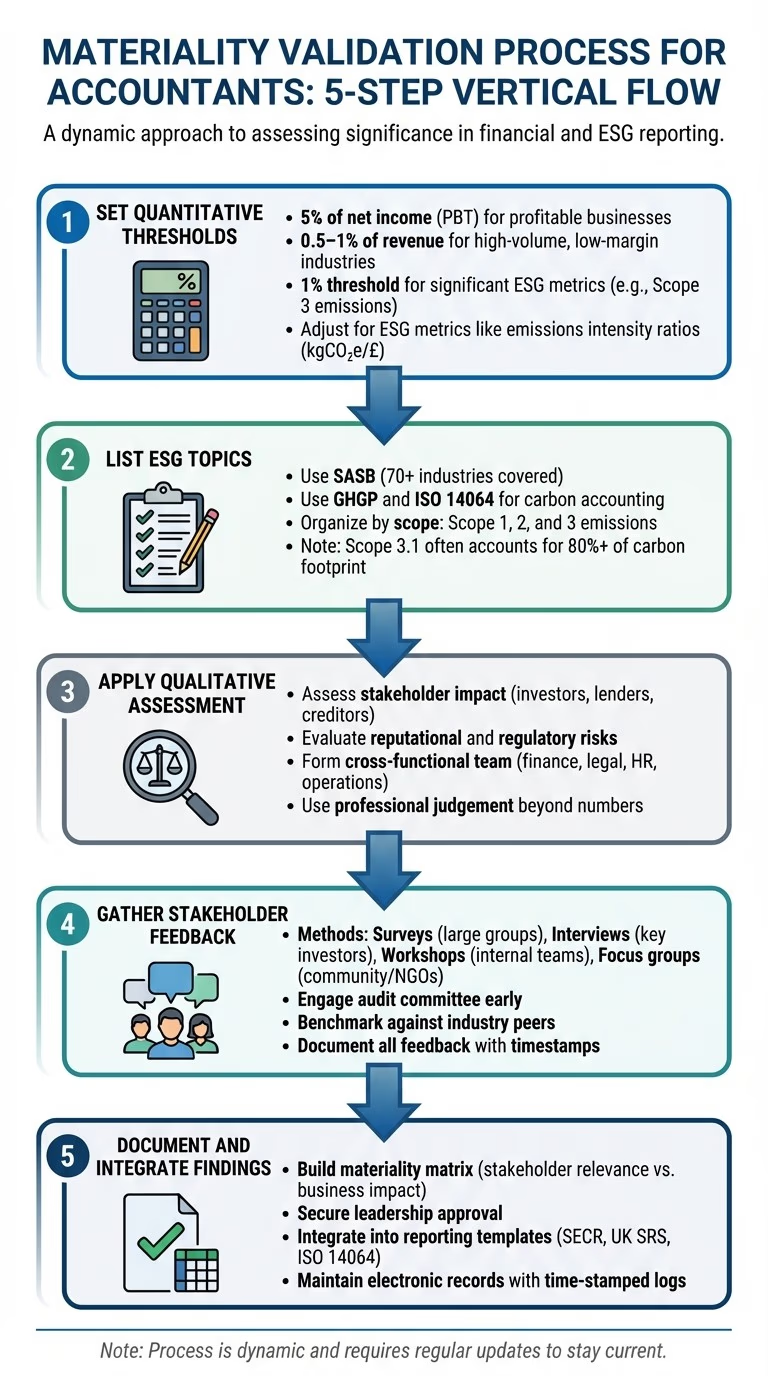

Materiality Validation: 5 Steps for Accountants

Materiality validation ensures that accountants identify ESG (Environmental, Social, and Governance) issues that matter most to investors, lenders, and other stakeholders. It's a mix of setting numerical thresholds and applying professional judgement to assess risks like reputational damage or regulatory issues. The process is dynamic, requiring regular updates to stay current.

Key Steps:

- Set Quantitative Thresholds: Establish financial benchmarks (e.g., 5% of net income) and adjust for ESG metrics like carbon emissions.

- List ESG Topics: Use frameworks like SASB and GHGP to identify relevant issues, focusing on areas such as Scope 3 emissions.

- Apply Qualitative Assessment: Evaluate risks like legal compliance and stakeholder concerns that go beyond numbers.

- Gather Stakeholder Input: Use surveys, interviews, and workshops to ensure alignment with stakeholder priorities.

- Document and Integrate Findings: Create a materiality matrix, secure leadership approval, and include results in reporting templates.

5-Step Materiality Validation Process for Accountants

ESG webinar: Materiality assessments and stakeholder engagement

Step 1: Set Quantitative Materiality Thresholds

Quantitative thresholds establish a numerical foundation for identifying material ESG data. This method works much like financial audits: select a benchmark, apply a percentage, and use the resulting figure to differentiate what’s material from what isn’t. The next step is to define specific financial benchmarks to determine these thresholds.

Choose Financial Benchmarks

Focus on financial measures that matter most to investors, lenders, and creditors. For businesses turning a profit, use profit before tax (PBT), typically set at 5% of net income. In industries with high volume but slim margins, a threshold of 0.5–1% of revenue might be more appropriate. For companies with significant physical assets, using total or net assets as the benchmark makes sense.

For not-for-profit organisations, materiality should be assessed in both absolute and relative terms. Align this with the auditor’s disclosed materiality. This ensures consistency between ESG thresholds and financial audits, reducing potential confusion.

Adjust Thresholds for ESG Metrics

Once financial benchmarks are established, refine the thresholds to suit ESG data. For instance, when conducting carbon accounting under GHGP or ISO 14064, use emissions intensity ratios like kilograms of CO₂ equivalent per pound of revenue (kgCO₂e/£) to link emissions to financial outcomes.

Qualitative factors can also influence the thresholds. For ESG metrics that draw significant stakeholder attention - such as Scope 3 emissions, which often account for over 80% of a company’s total carbon footprint - a 1% threshold may be more appropriate. The Australian Accounting Standards Board (AASB) explains this clearly:

"The presence of a qualitative factor lowers the thresholds for the quantitative assessment. The more significant the qualitative factors, the lower those quantitative thresholds will be".

This approach means that factors like regulatory risks, reputational concerns, or related party transactions can justify stricter thresholds, even if the quantitative data alone appears minor.

Step 2: List Potential Material ESG Topics

After setting quantitative thresholds, the next step is to create a thorough list of material ESG topics. This helps refine your materiality assessment by narrowing down specific environmental, social, and governance (ESG) issues. Using established frameworks can ensure you cover all the key areas effectively.

Use Frameworks to Identify ESG Topics

Start by consulting the Sustainability Accounting Standards Board (SASB). SASB provides industry-specific guidance on the ESG issues that matter most to investors, covering over 70 industries. For carbon accounting, frameworks like the Greenhouse Gas Protocol (GHGP) and ISO 14064 are essential. These tools categorise emissions systematically and align with ISSB reporting requirements and UK SRS standards.

When dealing with Scope 3 emissions, supplier-specific data is often unavailable. To fill these gaps, use lifecycle assessment (LCA) databases such as ecoinvent or the US EPA. These resources help approximate missing data while maintaining a defensible audit trail. If you’re exchanging Scope 3 data with suppliers, the PACT V2 standard (WBCSD) offers a structured format consistent with GHGP methodology.

Once you’ve identified ESG topics, organise them by scope to better understand their impact.

Organise Topics by Scope and Impact

After compiling potential topics, sort them into categories to clarify their relevance. For greenhouse gas emissions, use the three-scope model:

- Scope 1: Direct emissions from sources the organisation owns or controls, such as company vehicles or on-site fuel combustion.

- Scope 2: Indirect emissions from purchased electricity, steam, heating, and cooling.

- Scope 3: All other indirect emissions across the value chain, including upstream and downstream activities.

Pay special attention to Scope 3.1 (Purchased Goods and Services), as this often accounts for more than 80% of a company’s total carbon footprint. These emissions should be reported as "cradle-to-gate", covering the supply chain from raw material extraction to final delivery. Remember to include non-CO₂ gases in your assessment, as they can have a significant impact. For instance, Nitrous Oxide has 273–310 times the global warming potential of CO₂, while Methane is similarly impactful.

Beyond emissions, incorporate social and governance topics into your list. Use frameworks like SASB or GRI to build a comprehensive "longlist" of ESG issues before narrowing them down.

Step 3: Apply Qualitative Assessment

Once you've set thresholds and identified ESG topics, the next step is to evaluate them qualitatively. This approach helps uncover issues that go beyond numerical limits and assess their potential impact on stakeholders. As one non-executive director told the FRC:

"Materiality is not just a mechanical thing that you add up for misstatements".

A qualitative assessment takes into account the nature of a transaction, the specific context of your client's business - such as its industry and geographic location - and the potential for reputational or regulatory consequences.

Assess Stakeholder Impact

Start by examining how each ESG topic could influence your client's key stakeholders, including investors, lenders, and creditors. For example, a related-party transaction involving carbon offsets might seem minor financially, but it could carry significant weight if it raises questions about governance or potential conflicts of interest. Similarly, if your client operates in an industry where peers report Scope 3 emissions but your client does not, this omission could suggest that management is overlooking a critical risk.

To avoid missing important qualitative issues, form a cross-functional team with members from finance, legal, HR, operations, and procurement. Engage your internal legal or compliance teams to stay updated on relevant regulations. Benchmarking against industry peers can also help confirm whether your client's focus aligns with broader market expectations. If your client employs financially-integrated sustainability management, as promoted by neoeco, this process becomes smoother since finance and sustainability teams already share the same framework.

Use Professional Judgement

Applying professional judgement is vital when determining materiality for non-financial risks like reputation or compliance. Qualitative factors - such as a regulatory breach or a sudden shift in market trends - can lower the quantitative threshold for what is deemed material. For instance, if your client risks fines under SECR for underreporting emissions, that threat is material regardless of the fine's size, as it could damage investor trust and regulatory standing.

Monitoring public sentiment and peer reporting regularly can help identify emerging reputational risks. Use a combination of approaches: a "top-down" strategy to align with board-level goals and a "bottom-up" strategy to capture operational risks identified by staff. This method goes beyond a mere "tick-box" exercise, offering a more comprehensive view of the business. It allows you to uncover risks that could impact long-term value creation . Finally, gather direct feedback from stakeholders to refine your assessment further.

Step 4: Gather Stakeholder Feedback

After completing your qualitative analysis, it's time to gather feedback from stakeholders. This step is crucial for ensuring that the ESG topics you've identified align with what matters most to those affected. As an investor explained to the Financial Reporting Council (FRC):

"The board needs to have a grip on what's material to stakeholders".

To get a well-rounded perspective, bring together a cross-functional team that includes representatives from finance, operations, legal, HR, and sustainability. The FRC highlights that this collaborative approach acts as a "completeness check", helping to connect different viewpoints and reducing the chance of overlooking important issues.

Engage the audit committee early in the process. Their role in overseeing materiality validation mirrors their responsibilities in financial audits, ensuring robust governance and challenging findings where necessary. Additionally, benchmarking against industry peers can reveal which stakeholder groups competitors prioritise and what topics they disclose. If your organisation falls under frameworks like CSRD that require double materiality, you’ll need to broaden your consultations. This means assessing both how ESG issues impact the company and how the company affects society and the environment. For companies using financially‐integrated sustainability management, this alignment is often smoother since finance and sustainability teams already operate under a shared framework. Ultimately, this feedback process enhances your qualitative analysis, ensuring a thorough and well-rounded review.

Methods for Collecting Feedback

Different stakeholders require different engagement approaches. Here’s how to tailor your methods:

- Surveys: Ideal for reaching large groups like employees and customers, offering quantitative data and broad coverage.

- Interviews: Best for key investors and regulators, providing deeper qualitative insights and fostering stronger relationships.

- Workshops: Useful for internal teams and subject-matter experts, as they highlight interdependencies and promote strategic alignment.

- Focus groups: Effective for engaging community groups and NGOs, helping to understand specific societal or environmental impacts.

Choose methods that suit the stakeholder group’s role. For instance, when validating Scope 3 emissions, interviews with major suppliers and customers might provide more actionable insights than a general survey.

Record Feedback for Audit Trails

Documenting stakeholder feedback isn’t just a regulatory requirement; it also shows that your ESG priorities are grounded in real-world concerns.

Keep detailed records of pre-engagement plans, engagement outcomes, data validations, and change management logs, all with clear timestamps. Store these materials electronically in a secure format with time-stamped records.

This level of documentation ensures you can demonstrate to auditors and regulators that your materiality validation process was thorough, transparent, and aligned with stakeholder priorities.

Step 5: Document and Integrate Findings

Once you’ve gathered feedback from stakeholders, the next step is to organise your findings into a format that’s ready for auditing. This involves creating a materiality matrix, obtaining leadership approval, and embedding your conclusions into the relevant ESG reporting templates. These steps form the groundwork for the next stages: building the materiality matrix and integrating findings into your reports.

Start by assembling a cross-organisational working group that includes key representatives from finance, operations, and sustainability teams. This group plays a crucial role in validating the matrix findings against internal risk registers, budgets, and feedback from investors at AGMs. Additionally, involve your audit committee to review and challenge the assessment to ensure it aligns with your organisation’s strategic goals. As one investor told the FRC:

"What's material today might change in 12- or 24-months' time. You can't just work off your old materiality assessment, it needs to be current".

When presenting your findings, frame them as risk management and reputation-related issues rather than mere compliance. This approach can help secure leadership buy-in by showing how validating materiality protects the organisation’s financial health and public trust. For organisations where finance and sustainability teams already operate under a shared framework, achieving this alignment tends to be more straightforward.

Build a Materiality Matrix

A materiality matrix is a visual representation that maps ESG topics based on their relevance to stakeholders (Y-axis) and their impact on the business or financial performance (X-axis). Topics in the top-right quadrant are typically the highest priority.

If your organisation is subject to frameworks requiring double materiality - such as CSRD - your matrix should reflect both perspectives. Single materiality focuses on how ESG issues impact financial performance, while double materiality considers how the company affects society and the environment. This dual approach ensures you’re addressing both internal financial risks and broader societal impacts. Use data from internal risk registers, budgets, and investor feedback to validate the placement of each topic on the matrix.

Add Findings to Reporting Templates

After validating your matrix and securing leadership approval, integrate these findings into your reporting frameworks. For UK-based organisations, this often involves incorporating the results into SECR, UK SRS, or ISO 14064 reports. Make sure to clearly document any changes that stemmed from re-evaluations and include industry-specific factors that influenced your conclusions. This detailed documentation not only meets regulatory requirements but also provides auditors with a clear and transparent record of how materiality judgements were made. To enhance security and accessibility, maintain electronic records with time-stamped logs, ensuring your documentation is both organised and audit-ready.

Quantitative vs Qualitative Materiality Validation

When it comes to materiality validation, both quantitative and qualitative methods bring unique strengths to the table, offering a well-rounded approach to assessing risks. Quantitative validation relies on numerical benchmarks - like a percentage of net income, assets, or revenue - to sift through data efficiently. This method provides an objective and auditable process, making it ideal for handling large datasets. However, it might miss smaller items that, despite their size, pose major reputational or legal risks, such as instances of fraud or regulatory breaches.

On the other hand, qualitative validation prioritises the context and nature of an issue over its size. It examines factors like stakeholder concerns, legal obligations, and emerging ESG risks that aren't always visible in the numbers. For example, qualitative analysis can lower quantitative thresholds when significant risks are involved. A related party transaction or a shift in industry trends might still be deemed material even if it falls below the typical 5% threshold. This is especially relevant for ESG topics, such as Scope 3 emissions data, where qualitative insights are critical. For organisations managing Scope 3 emissions across client portfolios, combining both approaches ensures that no material issue is overlooked. Together, these methods lay the groundwork for a robust and audit-ready materiality validation process.

Benefits and Limitations of Each Method

| Method | Key Metrics | Benefits | Limitations | ESG Examples |

|---|---|---|---|---|

| Quantitative | % of Net Income, % of Total Assets, Revenue thresholds | Efficient, objective, and provides a clear audit trail | May miss small but critical risks, like fraud | Carbon emissions (tCO₂e), water usage (litres) |

| Qualitative | Legal risk, reputational impact, stakeholder concern | Captures emerging non-financial risks | Can be subjective and harder to measure consistently | Human rights due diligence, board diversity, brand trust |

A practical approach often starts with a quantitative baseline - say, 5% of net income - followed by a qualitative review to flag items that fall below numerical thresholds but carry significant contextual weight. Documenting the rationale behind these judgements is vital, ensuring that the audit trail clearly reflects why certain items were deemed material. It's also crucial to avoid treating financial and sustainability materiality as separate entities. Investors increasingly expect a unified view, showing how ESG risks influence long-term value.

Conclusion

Materiality validation is all about balancing numbers with professional judgement. It’s a process that blends quantitative thresholds with qualitative insights. The steps - defining numerical benchmarks, identifying ESG topics, applying qualitative analysis, gathering stakeholder input, and documenting everything - help create a process that’s ready for audit. As the Australian Accounting Standards Board (AASB) explains:

"Making materiality judgements involves both quantitative and qualitative considerations. It would not be appropriate for the entity to rely on purely numerical guidelines or to apply a uniform quantitative threshold".

Even small numerical discrepancies can require attention when qualitative risks are involved. This approach ensures that numerical data and professional judgement work together effectively.

Modern tools make applying these principles much easier. For example, neoeco simplifies the process by automatically mapping transactions to recognised emissions categories under major frameworks. Instead of manually handling data, you get real-time, finance-grade carbon data that updates alongside client ledgers. With its built-in Policy & Evidence Hub, your audit trail stays intact. So, when qualitative decisions arise - like a sudden increase in a supplier’s Scope 3 emissions - you’ll have the documentation to back your judgement. This kind of integration strengthens the five-step process and ensures it runs smoothly.

FAQs

How do quantitative and qualitative methods work together in materiality validation?

When it comes to materiality validation, using both quantitative and qualitative methods ensures a balanced and comprehensive approach.

Quantitative methods rely on hard data - think financial thresholds or emissions figures. These provide a clear, objective way to identify and prioritise material issues. By focusing on measurable criteria, organisations can assess risks with consistency and precision.

On the other side, qualitative methods bring in the human element. This includes expert judgement, feedback from stakeholders, and contextual analysis. These methods shine a light on aspects that might not be easily measured but are still crucial due to their relevance, potential impact, or strategic value.

By blending these two approaches, organisations can tackle both the tangible risks and the more nuanced concerns of stakeholders. This combination leads to a well-rounded materiality validation process that supports smarter, more informed decisions.

Why is stakeholder feedback important in ESG materiality assessments?

Stakeholder feedback plays a key role in ESG materiality assessments by helping organisations pinpoint and prioritise the issues that are most important to their stakeholders. This process also sheds light on factors that can influence long-term value creation. Through tools like surveys, meetings, and consultations, organisations can confirm and fine-tune the material topics identified during their assessment.

Such feedback offers insights that go beyond numbers, emphasising the qualitative significance of specific issues or potential risks on the horizon. Factoring in stakeholder perspectives ensures that ESG disclosures stay relevant and credible while meeting stakeholder expectations. This approach builds trust and promotes transparency in reporting.

Why is it necessary to update materiality assessments regularly?

Keeping materiality assessments current is crucial for organisations aiming to address the most pressing environmental, social, and governance (ESG) issues. These assessments ensure that decision-making stays aligned with shifting risks, emerging opportunities, and evolving stakeholder expectations. Factors like new regulations, market dynamics, and societal shifts can all influence priorities over time.

Regular updates to these assessments allow businesses to zero in on areas that create lasting value, stay compliant with changing standards, and refine their sustainability strategies. This forward-thinking approach not only aids in making well-informed decisions but also bolsters resilience in an ever-changing business landscape.