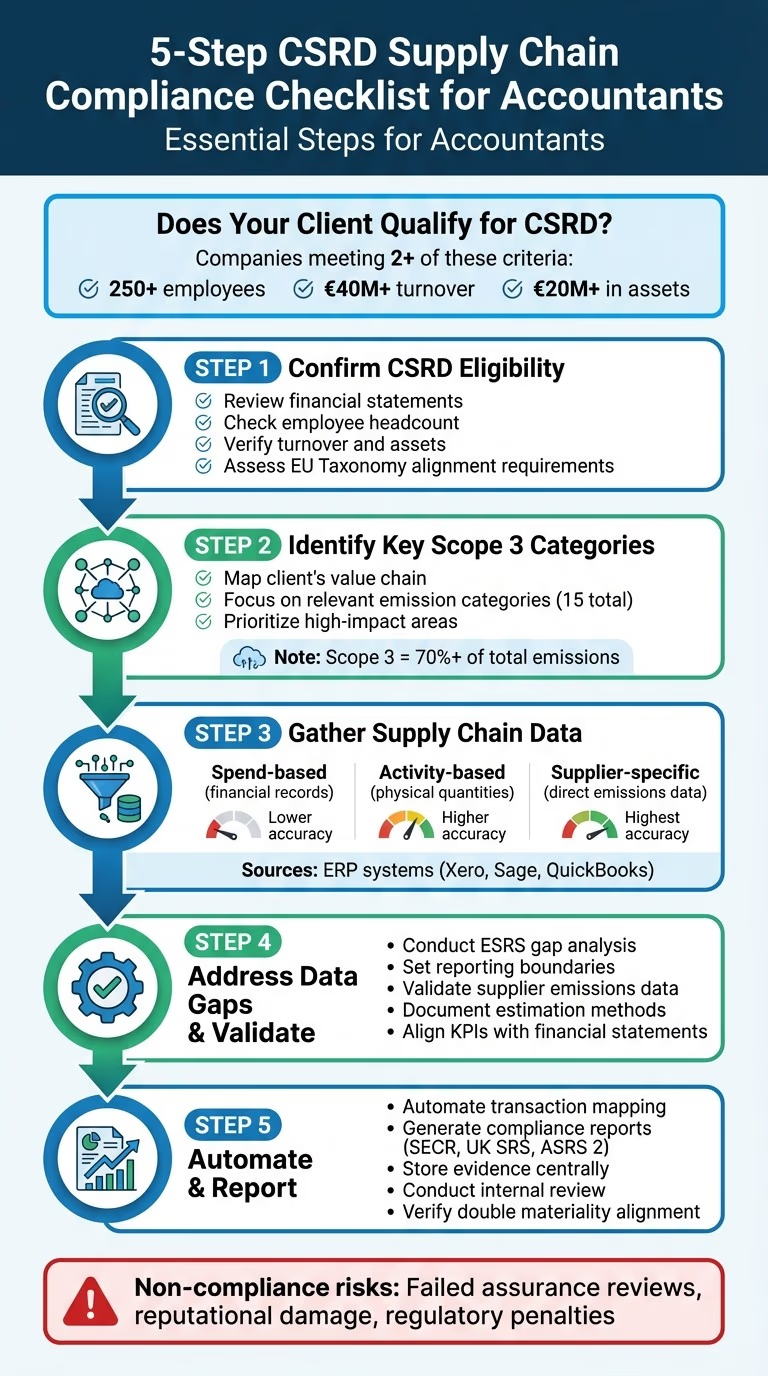

CSRD Supply Chain Reporting: Checklist for Accountants

The Corporate Sustainability Reporting Directive (CSRD) introduces stricter rules for companies operating in the EU to disclose their sustainability impacts. Accountants play a key role in ensuring compliance, particularly with the double materiality principle, which evaluates both the organisation's impact on the planet and how sustainability issues affect the business.

Key points to know:

-

Who needs to comply? Companies meeting at least two of these criteria:

-

250+ employees

-

€40M+ turnover

-

€20M+ in assets

-

-

Focus areas for reporting:

-

Scope 3 supply chain emissions (often over 70% of total emissions).

-

Aligning business activities with the EU Taxonomy (turnover, CapEx, OpEx).

-

-

Steps to prepare:

-

Confirm if your client qualifies under CSRD.

-

Identify key Scope 3 emission categories based on their operations.

-

Gather data (spend-based, activity-based, or supplier-specific).

-

Address gaps in data and validate supplier information.

-

Automate reporting processes for accuracy and efficiency.

-

Non-compliance risks include failed assurance reviews, reputational damage, or regulatory penalties. Tools like neoeco can simplify data collection, mapping, and reporting, helping accountants deliver reliable, finance-grade sustainability reports.

5-Step CSRD Supply Chain Compliance Checklist for Accountants

Assess CSRD Requirements and Supply Chain Scope

Check Client CSRD Eligibility

Before diving into supply chain data, it's crucial to confirm whether your client falls under the Corporate Sustainability Reporting Directive (CSRD). This directive is set to affect over 50,000 businesses across the EU, but not every organisation will qualify.

To determine eligibility, compare the following criteria with your client's most recent financial statements and headcount records. If they meet at least two of these thresholds, they are subject to CSRD requirements:

| CSRD Eligibility Criteria | Threshold Value |

|---|---|

| Employee Count | More than 250 employees |

| Net Turnover | Over €40 million |

| Balance Sheet Total | Over €20 million |

If your client qualifies, keep in mind that compliance goes beyond emissions reporting. They’ll also need to align with the EU Taxonomy (EUT), which involves linking business activities to financial metrics like turnover, capital expenditure, and operational expenditure. This adds a layer of complexity that requires careful planning.

Once eligibility is confirmed, your next step is to identify the key Scope 3 emissions categories relevant to the client.

Identify Scope 3 Supply Chain Emissions

Supply chain emissions, which fall under Scope 3, are often the largest contributor to a company’s overall carbon footprint - frequently accounting for more than 70% of total emissions. The Greenhouse Gas Protocol breaks Scope 3 into 15 categories, covering both upstream (e.g., suppliers, raw materials, business travel) and downstream activities (e.g., product use, disposal, investments).

To get started, map out your client’s value chain and focus on the Scope 3 categories that are most relevant to their operations. For instance:

- Manufacturing businesses often see their biggest emissions stemming from upstream activities like raw material sourcing or supplier processes.

- Software companies may find higher emissions tied to employee commuting or cloud computing services.

Rather than trying to cover all 15 categories immediately, prioritise the ones that have the greatest impact on the client's specific business model. This targeted approach ensures meaningful progress without overwhelming resources.

Additionally, set clear boundaries for reporting, which should include emissions from second and third-tier suppliers. For more guidance, explore how ISSB reporting can integrate these disclosures into a cohesive financial strategy.

Gather Supply Chain Data

Required Data Types for Scope 3 Emissions

Once you've identified the key Scope 3 emission categories, the next step is collecting the right data to measure them effectively.

Accurate supply chain reporting starts with gathering data across all 15 Scope 3 categories. Focus on the categories that have the biggest impact on your client's carbon footprint. Pay particular attention to purchased goods and services, upstream and downstream transport, and the use of sold products. The data you’ll need typically falls into three types:

- Spend-based: Financial records detailing supplier spend.

- Activity-based: Physical quantities, such as tonnes of materials, litres of fuel, or kilometres travelled.

- Supplier-specific: Emissions data provided directly by suppliers.

Start with spend-based data from existing ERP systems like Xero, Sage, or QuickBooks. As you build stronger relationships with suppliers, transition to activity-based vs spend-based emission methods for more precise reporting.

| Calculation Method | Data Source | Accuracy Level | Best Use Case |

|---|---|---|---|

| Spend-based | Financial records/spend | Lower | Initial assessments and less critical categories |

| Activity-based | Quantities (tonnes, kWh, km) | Higher | Pinpointing major "hotspots" and advanced cycles |

| Hybrid | Combination of spend and activity | Moderate-High | Balancing data availability with precision |

Data in the table is adapted from.

Data Collection Methods

To begin, extract spend-based data from your accounting software (e.g., Xero, Sage, QuickBooks). Use this information to apply average emission factors from recognised databases like the UK DEFRA Database, US EPA, or ecoinvent. This approach works well for initial screening of less impactful categories.

For areas with a higher carbon footprint, switch to activity-based data. This involves gathering physical quantities - such as tonnes of materials, kilowatt-hours, or kilometres - and converting these into CO₂e using specific emission factors. This method provides a clearer picture of emissions in critical areas.

When possible, incorporate direct emissions data from suppliers. As transparency within the supply chain improves, suppliers can offer precise emissions figures, reducing the need for estimates. Tools like Scope 3 emissions management can help automate the mapping of transactions to recognised emissions categories, streamlining the entire process.

Identify Data Gaps and Validate Information

Analyse Supply Chain Data Gaps

Start by mapping the client’s value chain to pinpoint where data might be missing. This involves setting clear reporting boundaries - defining organisational limits and examining how upstream suppliers and downstream customers interact. This step ensures you know exactly where to focus your efforts.

Next, conduct an ESRS gap analysis. Compare the client’s current ESG data to the topics required under CSRD. Pay special attention to high-emission areas identified in your double materiality assessment. This ensures resources are prioritised in areas that will make the most difference.

Make sure sustainability KPIs align with financial statements. EU Taxonomy figures need to match key financial metrics like turnover, CapEx, and OpEx. This integrated approach not only improves accuracy but also prepares the data for the independent limited assurance reporting required by CSRD. Using tools like neoeco’s ISSB reporting features can help bridge the gap between financial and sustainability data, making the process smoother.

With data gaps identified, the next step is validating supplier emissions data to ensure audit readiness.

Validate Supplier Emissions Data

Establish strict criteria for validating supplier emissions data. This step is crucial, as CSRD disclosures must be both human-readable and machine-readable with digital tagging.

Focus on high-emission suppliers first. Require them to provide detailed documentation of their calculations, methodologies, and assumptions. If supplier data isn’t available, clearly document your estimation methods and emission factors. Ensure these are traceable back to recognised sources, such as the UK DEFRA Database, to maintain credibility.

Supplier performance should be monitored and reassessed regularly. As transparency across the supply chain improves, you can move from initial spend-based estimates to more precise activity-based data and, eventually, to supplier-specific emissions figures. This phased approach balances the need for immediate compliance with the goal of long-term accuracy. By doing so, clients can meet CSRD requirements while laying the groundwork for more reliable reporting in the future.

Automate Supply Chain Mapping and Reporting with neoeco

Automate Supply Chain Transaction Mapping

neoeco integrates directly with popular financial systems like Xero, Sage, or QuickBooks, using AI to categorise each purchase under the correct emissions category. This eliminates the need for manual data entry, cumbersome spreadsheets, or second-guessing which supplier expenses align with specific Scope 3 categories.

With its Sustainability Ledger, neoeco tracks over 90 impact factors per transaction, adhering to GHGP and ISO 14064 standards. This method, called Financially-integrated Sustainability Management (FiSM), applies the same level of precision and audit standards to ESG metrics as financial records. As your clients refine their data quality, neoeco allows a transition from general spend-based estimates to more precise activity-based metrics, ensuring compliance with the detailed requirements of CSRD by aligning materiality with financial risk.

This automated process not only simplifies mapping but also sets the stage for streamlined report generation.

Generate Compliance Reports

Once transactions are mapped, neoeco can instantly produce SECR, UK SRS, and ASRS 2 reports. These reports meet CSRD technical standards, ensuring they are easy to read for both humans and machines.

A live checklist keeps track of progress in real time, highlighting completed tasks, missing information, and items ready for review. This built-in system ensures nothing is overlooked during the year-end reporting process. Plus, as UK and Australian regulatory frameworks evolve, neoeco automatically updates its reporting formats, saving your team the hassle of manual compliance tracking.

Store Data and Evidence in One Place

After reports are generated, neoeco helps consolidate all necessary documentation to ensure audit readiness.

The Policy and Evidence Hub serves as a central repository, storing supplier communications, methodologies, and supporting documentation. This creates a clear and transparent audit trail that auditors can access directly, simplifying the entire process and ensuring everything is in one place for review.

Review and Finalise Supply Chain Disclosures

Conduct Internal Review and Risk Assessment

Before submitting your CSRD disclosures, it’s crucial to carry out an internal audit to spot any gaps or inconsistencies in your data. Under CSRD, third-party assurance for sustainability disclosures is mandatory, meaning auditors will closely examine both the data itself and how it was compiled.

Form a dedicated CSRD task force, bringing together teams from finance, procurement, and sustainability. Their job? To align key performance indicators (KPIs) with financial statements. Any discrepancies here could trigger concerns.

Pay close attention to suppliers or categories that carry notable environmental or social risks. Use scenario analysis to estimate the potential financial impact these risks could have.

Before publishing your disclosures, secure approval from executives. This includes sign-off on your goals, strategies for mitigating risks, and detailed action plans.

Once your internal audit and risk assessment are complete, make sure your disclosures meet the double materiality requirements fully.

Verify Double Materiality Alignment

After your internal review, take the next step by ensuring your reporting aligns with double materiality principles.

Double materiality is at the heart of CSRD compliance. It requires you to address two perspectives: how your supply chain activities impact people and the planet (Impact Materiality) and how sustainability factors influence your business performance (Financial Materiality).

To meet these standards, map your entire value chain to establish clear reporting boundaries. Apply materiality thresholds to pinpoint which supply chain impacts, risks, and opportunities are significant enough to disclose. This process involves consulting stakeholders and making decisions based on solid evidence.

Finally, assess your supply chain activities against EU Taxonomy criteria. Confirm that your economic activities contribute meaningfully to environmental objectives while ensuring they "Do No Significant Harm".

CSRD and Scope 3: Best Practices for Value Chain Reporting

Conclusion

Under the CSRD, organisations that meet thresholds of 250 employees, €40 million turnover, or €20 million in total assets are required to map their value chain and report material impacts using the double materiality approach. Non-compliance could lead to mandatory third-party assurance reviews. These measures are essential for ensuring both regulatory compliance and audit readiness.

Traditional approaches, like relying on manual spreadsheets or scattered records, can take weeks or even months, often leading to duplication and errors. neoeco offers a smarter alternative. By integrating directly with financial ledgers such as Xero, Sage, and QuickBooks, it maps transactions to recognised emissions categories under GHGP and ISO 14064. The result? Audit-ready, finance-grade reports delivered in just minutes.

For accounting firms, this creates an opportunity to expand into sustainability services without disrupting existing workflows.

The checklist steps covered earlier - from determining CSRD eligibility to validating supplier data and conducting internal reviews - are the foundation of effective supply chain reporting. However, achieving speed and precision hinges on using the right tools. With financially-integrated sustainability management, you're not merely meeting compliance requirements - you’re positioning your firm as a trusted adviser in sustainability.

Starting with your clients' financial data, you can pave the way for a seamless journey to full CSRD compliance.

FAQs

What does double materiality mean in CSRD reporting?

Double materiality is central to the Corporate Sustainability Reporting Directive (CSRD), pushing companies to evaluate sustainability from two distinct angles.

The outside-in perspective focuses on how environmental and social factors - like climate change or human rights issues - affect a company’s financial performance. On the flip side, the inside-out perspective looks at how the company’s own actions impact the environment and society, such as through greenhouse gas emissions or resource consumption.

For accountants, this involves more than just crunching numbers. It’s about identifying and quantifying these impacts throughout the value chain, tying them directly to financial metrics, and ensuring the methods used can stand up to an audit. Tools like neoeco make this process far more manageable. By automating data collection, mapping impacts, and generating reports that align with CSRD standards, these tools help simplify compliance and streamline reporting.

What’s the best way for companies to collect Scope 3 emissions data effectively?

To gather dependable Scope 3 emissions data, begin by mapping your value chain. This includes all upstream and downstream activities categorised under recognised areas such as purchased goods, transportation, use-phase, and end-of-life. Clearly outline your reporting boundaries and focus on areas with the greatest impact. Engaging suppliers early is key - ask for primary data (e.g., actual emissions from specific activities), as this is the most precise and ready for audits. When primary data isn’t accessible, rely on secondary data like industry averages or published emission factors, and aim to improve the accuracy of this data over time.

To make the process easier, consider automating data collection by connecting sustainability metrics directly to your financial transactions. Tools that align emissions categories with your financial ledger can map these transactions to standards such as GHGP, ISO 14064, and UK SECR. This approach produces accurate, audit-ready reports while eliminating manual effort. Maintain a clear record of all data sources, methodologies, and assumptions to uphold transparency and compliance.

Take a step-by-step approach: start with secondary data to create a broad overview, then gradually shift to collecting primary data for the most significant emissions. As your supplier relationships strengthen and automation tools refine your processes, your data will improve in accuracy and reliability, helping you efficiently meet CSRD’s Scope 3 reporting requirements.

What are the consequences of failing to comply with the CSRD?

Failing to meet the requirements of the CSRD (Corporate Sustainability Reporting Directive) can have serious repercussions. These include financial penalties, potential legal challenges, and damage to your organisation's reputation. Beyond the immediate risks, non-compliance can shake investor confidence and even restrict access to important markets.

For accounting firms, compliance goes beyond simply dodging fines. It's about preserving trust and credibility with clients and stakeholders. Transparent and precise reporting not only satisfies regulatory demands but also signals a genuine commitment to sustainability efforts.