How Stakeholder Prioritisation Impacts Materiality Assessments

Stakeholder prioritisation is critical for accurate materiality assessments. Without it, organisations risk overlooking important ESG issues and relying on incomplete data. This article explores how to identify and prioritise stakeholders effectively, ensuring double materiality assessments align with evolving regulatory standards like CSRD and ISSB.

Key Takeaways:

- Stakeholder Mapping: Include diverse voices across the value chain - employees, suppliers, communities, and regulators.

- Weighting Stakeholders: Use clear, documented criteria to balance influence and importance, avoiding overemphasis on vocal groups.

- Aligning Priorities: Categorise ESG issues by urgency and relevance, ensuring they meet materiality thresholds for financial and societal impact.

- Consistent Engagement: Establish regular cycles for stakeholder input and use structured data management to maintain accuracy over time.

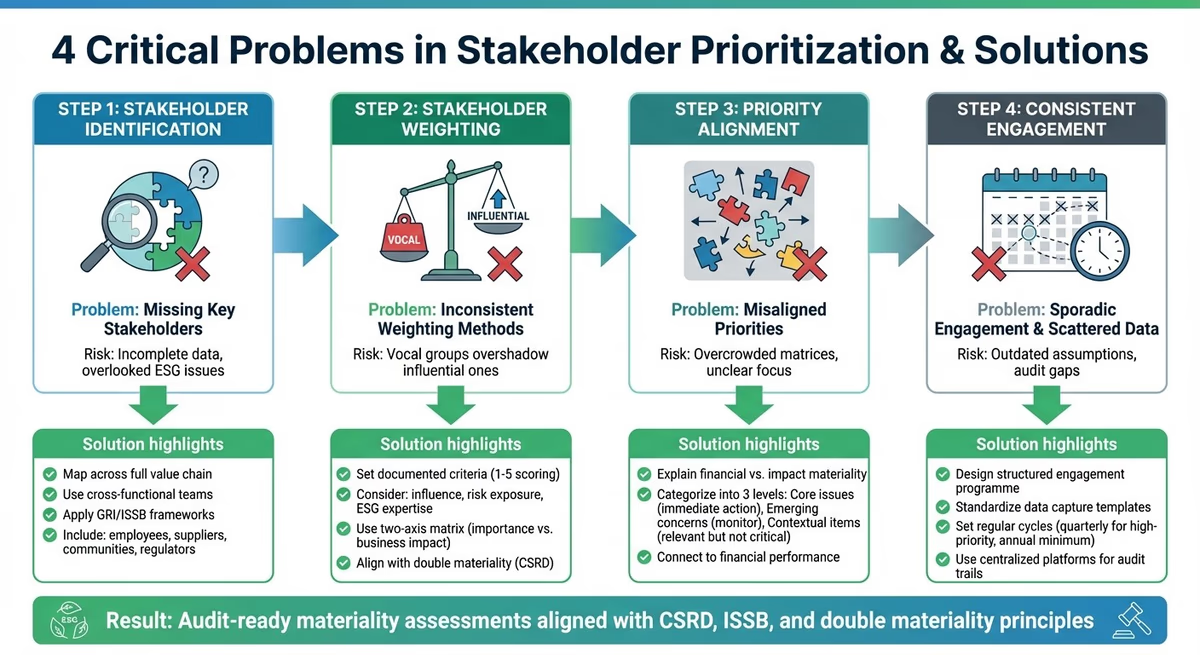

4-Step Framework for Effective Stakeholder Prioritization in Materiality Assessments

ESG webinar: Materiality assessments and stakeholder engagement

Problem 1: Missing Key Stakeholders in the Identification Process

Many organisations make the mistake of focusing solely on investors, major customers, and board members when identifying stakeholders. While these groups are undoubtedly important, this narrow approach leaves out other critical voices. By excluding employees, suppliers, local communities, or regulators, you risk building an ESG strategy on incomplete data. The result? Important issues can go unnoticed until they escalate into reputational or operational problems.

Simply having strong governance isn't enough if the identification process is flawed. For example, if your working group is limited to finance and investor relations, the focus will naturally lean towards financial priorities, leaving social and environmental concerns underrepresented. This is especially problematic when frameworks like CSRD demand a "double materiality" approach. Recognising and addressing this gap is a crucial step in creating a well-rounded ESG strategy.

Map Stakeholders Across Your Value Chain

To address this issue, start by systematically mapping all stakeholder relationships. Create a cross-functional team that includes representatives from finance, HR, operations, and procurement. This diversity helps ensure no stakeholder group is overlooked. Consider the full value chain - upstream suppliers, downstream distributors, employees at all levels, local communities near your operations, and regulatory bodies.

Combining top-down strategic insights with bottom-up operational input is key. This approach helps uncover issues that senior leadership might miss when viewing things from the boardroom.

Use Established Frameworks for Identification

Instead of starting from scratch, use existing frameworks like the GRI stakeholder categories or the stakeholder definitions outlined in ISSB reporting standards (IFRS S1 and S2). These tools provide structured lists of stakeholder types, ensuring no group is overlooked. They also strengthen your process, making it more defensible during assurance reviews.

How neoeco Supports Stakeholder Identification Using Financial Data

For accounting firms, neoeco's transaction-mapping features offer a practical solution. By analysing spend and revenue data from client ledgers, neoeco pinpoints key stakeholder relationships embedded in the numbers. This includes major suppliers, customer segments, and service providers. This financially-driven approach ensures stakeholder identification isn't just a theoretical exercise but is firmly grounded in real business relationships reflected in financial records.

Problem 2: Inconsistent Stakeholder Weighting Methods

After identifying all the relevant stakeholders, the next hurdle is deciding how much influence each group should have. Too often, this process relies on instinct rather than a structured approach. The result? A materiality matrix that may not reflect actual priorities and becomes hard to justify when scrutinised by boards, auditors, or regulators.

Without clear guidelines, there’s a risk of overemphasising vocal groups while underestimating the importance of influential ones. For example, small but outspoken groups might overshadow key suppliers with significant influence. This imbalance can lead to strategic blind spots and damage the credibility of the materiality process.

The Financial Reporting Council (FRC) has highlighted this governance issue. One investor from their research stated:

"It all starts with good governance. The board needs to have a grip on what's material to stakeholders".

Yet, many organisations don’t have documented systems showing how weighting decisions are made, making it hard to satisfy audit committees or external assurance providers. Adopting a structured method for stakeholder weighting is essential for building trust and accountability.

Set Clear Criteria for Weighting Stakeholders

Establish specific, documented criteria to guide stakeholder weighting. These should consider factors like influence on business outcomes, risk exposure, and expertise in ESG matters. For example, a regulator might carry significant weight due to their enforcement powers, while an industry expert could score high on knowledge but lower on direct business impact.

Using a 1–5 scoring framework for each criterion can transform subjective decisions into a transparent, defensible process. To gain board-level support, link stakeholder priorities to key areas like corporate risk, reputation, and long-term value creation. When directors see how stakeholder weighting ties into the company’s risk management and strategic goals, they’re more likely to engage and approve the methodology.

Align Stakeholder Significance with Business Impact

To prioritise effectively, use a two-axis matrix that plots stakeholder importance against business impact. Focus on the top-right quadrant, where the most critical issues intersect.

This approach aligns with double materiality principles under the Corporate Sustainability Reporting Directive (CSRD). It requires organisations to consider both financial materiality (how ESG issues affect company value) and impact materiality (how the company influences the environment and society). For businesses with intricate supply chains, this often means giving weight to Scope 3 emissions, especially when environmental concerns overlap with key supplier dependencies.

Document Weighting Processes for Assurance

Documenting the weighting process is crucial for satisfying audit committees and external reviewers. As noted by the FRC:

"Good practice is for committees to discuss the materiality level set and evaluate this in view of their knowledge of the business to determine its appropriateness, challenging the audit team where necessary".

Your documentation should include the reasoning behind thresholds, the qualifications of those involved, and how conflicts of interest were handled. This level of transparency reassures stakeholders and strengthens the process.

For accounting firms assisting clients, neoeco’s platform offers tools like audit trails and version control. These features ensure the weighting process is consistent, repeatable, and defensible during external assurance reviews, year after year.

Problem 3: Stakeholder Priorities Don't Align with Materiality Frameworks

Even when stakeholders are identified and their input is carefully considered, the result can often be a long and disorganised list of priorities. Without clear thresholds to filter these inputs, materiality matrices risk becoming overcrowded. This not only muddies strategic focus but also makes it harder for boards to allocate resources where they are needed most.

The main challenge lies in the fact that stakeholders tend to prioritise issues from their own perspectives. For example, environmental groups might zero in on climate impact, employees may focus on workplace conditions, and investors often prioritise financial returns. These differing viewpoints don't always align with the double materiality requirements of the CSRD. This misalignment can lead to priorities that are either too broad to act on or disconnected from the factors that drive long-term value. The first step in addressing this is to clarify and align stakeholder concerns with the materiality framework.

Explain Different Types of Materiality to Stakeholders

It’s important to help stakeholders understand the distinction between financial materiality (how ESG issues influence a company’s performance) and impact materiality (how a company’s activities affect society and the environment). The CSRD’s double materiality approach requires both perspectives to be considered. However, stakeholders may not always recognise that not every concern meets the thresholds for disclosure or strategic action.

The Financial Reporting Council (FRC) defines material information as that which, "when omitting, misstating, or obscuring it could be reasonably expected to influence the decisions of primary users of financial reporting". This definition can serve as a framework for discussing which topics are truly critical for decision-making.

Categorise Material Topics by Priority Level

Once stakeholder input has been collected, it’s helpful to categorise topics into three priority levels:

- Core issues: These require immediate attention and full disclosure.

- Emerging concerns: These are important to monitor but may not demand immediate action.

- Contextual items: These are relevant but not critical for decision-making.

By plotting these categories on a materiality matrix - where the Y-axis represents stakeholder importance and the X-axis represents business impact - you can focus on the issues in the top-right quadrant. This structured approach not only prevents boards from being overwhelmed but also clarifies management’s priorities. It becomes easier to allocate resources, assign responsibilities, and set measurable goals. This categorisation also sets the stage for linking these priorities to financial outcomes.

Connect Stakeholder Priorities to Financial Performance

Once priorities are clearly categorised, the next step is to tie them to financial performance. This is where aligning stakeholder concerns with materiality frameworks becomes actionable. ESG topics gain more traction when they are connected directly to financial data. For instance, platforms like neoeco can map sustainability priorities - such as Scope 3 emissions from supply chains - to transaction-level financial data. This approach ensures that stakeholder concerns are grounded in measurable business impact, making them more actionable and relevant to decision-makers.

Problem 4: Inconsistent Stakeholder Engagement and Data Collection

When stakeholder engagement is sporadic or limited to a single instance, the reliability of your materiality assessment takes a hit. One-off surveys or isolated interviews might meet compliance requirements, but they don’t reflect how stakeholder priorities evolve over time. Without regular engagement, outdated assumptions can creep in, undermining strategic planning and leaving your organisation unprepared for audits.

Scattered data creates another challenge. When stakeholder input is buried in emails, spreadsheets, or meeting notes, it’s tough to track who said what and when. This lack of organisation wastes time and leaves gaps that auditors are likely to flag, making it harder to document ESG materiality evidence effectively. Researchers often describe this as superficial engagement - efforts that fail to provide the deep insights needed to anchor an ESG agenda in the issues that matter most.

Design a Structured Engagement Programme

To tackle fragmented feedback, put a structured engagement programme in place. Start by mapping out your key stakeholders and scheduling engagement based on their importance. For example, high-priority groups like investors, regulators, and major suppliers might require quarterly check-ins, while others can be engaged annually. Form a cross-functional materiality working group with representatives from finance, operations, sustainability, HR, and procurement to ensure all critical voices are heard.

Incorporate horizon scanning into your process to stay ahead of emerging risks. This could include reaching out to investors, analysing media trends, participating in industry forums, or consulting regulatory updates. Such proactive efforts help you identify risks early, keeping your materiality assessment aligned with both current and future expectations.

Standardise How You Capture and Store Data

Consistency is key when managing stakeholder input. Use a standardised template for all engagement activities - whether they’re surveys, interviews, or workshops. Centralise this data in a single platform like neoeco to ensure everything is easy to track and audit. By using a uniform format, you can quickly compare responses across different stakeholders and over time. Platforms like neoeco also allow you to link stakeholder priorities, such as supply chain emissions, directly to transaction-level financial data, creating a clear audit trail.

Governance oversight is essential here. Audit committees should regularly review your materiality assessment process to ensure it aligns with internal budgets and risk management frameworks. With structured data and an audit trail in place, you can seamlessly integrate these insights into your engagement cycles.

Set Up Regular Engagement Cycles

Once your engagement programme and data processes are in place, establish regular cycles to keep your materiality assessments up to date. Materiality isn’t static - it shifts with market dynamics, regulatory changes, and organisational milestones like acquisitions or expansions. For most organisations, an annual review is the bare minimum, while high-priority stakeholders should be engaged quarterly. Align these cycles with your strategic planning schedules to ensure your board stays informed about evolving stakeholder priorities.

Conclusion

Stakeholder prioritisation isn’t just about ticking boxes - it’s the foundation of a solid materiality assessment. By systematically mapping stakeholders across your value chain, applying clear weighting criteria, and aligning with established frameworks, you can focus on the ESG issues that truly impact performance, risk, and reputation. This ensures your materiality matrix captures both stakeholder priorities and business relevance, giving your board and auditors confidence in your approach. It’s a method that supports sustainable reporting across your organisation.

One of the biggest hurdles for organisations is maintaining consistency in engagement cycles and turning stakeholder insights into reliable, finance-grade data. That’s where neoeco steps in. By operating directly on your financial ledger, neoeco connects stakeholder priorities - like supply chain emissions - to transaction-level data. This creates an audit-ready trail that complies with GHGP, ISO 14064, and UK SRS standards. Say goodbye to spreadsheets and manual processes, and rely on precise, finance-grade carbon data instead.

For accounting firms, this opens up the opportunity to deliver well-structured materiality assessments that integrate seamlessly with clients’ financial reporting. Whether you’re working with SMEs or larger private companies, neoeco equips your firm to meet the rising demand for sustainability management that’s fully integrated with financial systems. Learn more about financially-integrated sustainability management designed for accountants.

When done right, stakeholder prioritisation becomes a strategic advantage, not just a compliance task. It helps identify emerging risks, allocate resources wisely, and show investors that your organisation understands what matters most. Through structured engagement, standardised ESG data collection, and smart technology, stakeholder insights are transformed into actionable strategies that deliver long-term value.

FAQs

How can organisations effectively identify all relevant stakeholders for a materiality assessment?

To identify all relevant stakeholders, organisations should start with a well-organised mapping process. First, outline the purpose and scope of the materiality assessment. Then, create a list of key groups, splitting them into internal stakeholders - like board members, employees, and finance teams - and external ones, including investors, regulators, customers, suppliers, local communities, and NGOs. A stakeholder-mapping matrix can be a helpful tool to visualise each group's level of influence and impact, ensuring no essential perspectives are missed.

Validation plays a crucial role here. Use a combination of quantitative and qualitative methods, such as surveys, interviews, and focus groups, to ensure the stakeholder list is thorough. Documenting this process is equally important, as it provides transparency and allows senior leadership to review and approve the approach.

Specialist tools can make this process even smoother. For instance, sustainability accounting platforms like neoeco can integrate directly with financial data, helping organisations keep accurate, up-to-date stakeholder records. These tools also link transactions to established sustainability frameworks, simplifying stakeholder management. By combining a structured approach, meaningful engagement, and the right technology, organisations can ensure their stakeholder identification process is both thorough and reliable.

How can stakeholders be prioritised effectively during a materiality assessment?

Balancing hard data with thoughtful judgement is key when prioritising stakeholders during a materiality assessment. Start by identifying the main groups involved - this typically includes investors, employees, customers, suppliers, local communities, and regulators. Evaluate their influence, impact, legitimacy, and urgency, considering both their power over your organisation and how your actions affect them.

To organise these insights, assign each stakeholder a score based on criteria like their strategic importance (e.g., their influence on your reputation or access to funding) and the relevance of the ESG issues they highlight (such as carbon emissions or labour conditions). Make sure this scoring aligns with the purpose of your assessment, whether you’re focusing on financial outcomes (single materiality) or broader societal impacts (double materiality). Referencing regulatory frameworks like ISSB, CSRD, or SECR can help keep your process compliant.

Lastly, validate your findings by engaging directly with stakeholders through methods like surveys or interviews. This step ensures you capture any emerging issues or concerns. A clear and structured approach like this not only supports financial priorities but also aligns with wider sustainability objectives.

How does engaging with stakeholders regularly improve materiality assessments?

Regularly engaging with stakeholders can significantly enhance materiality assessments by offering timely, practical insights that help validate and sharpen an organisation's understanding of key ESG issues. By using methods like surveys, workshops, or digital platforms, businesses can pinpoint the issues that matter most while minimising the chance of missing critical concerns. This approach also helps counteract internal biases by bringing in a mix of external perspectives.

As stakeholder priorities shift - whether due to regulatory updates, changing investor expectations, or community needs - consistent engagement, whether annually or quarterly, ensures the materiality matrix stays relevant and actionable. The insights gathered can then be transformed into clear ESG goals, such as setting carbon-reduction targets or boosting local hiring efforts, aligning the assessment with both financial and societal outcomes.

Tools like neoeco make this process even smoother. By integrating directly with financial ledgers, they automate data collection and link it to recognised emissions categories. This not only cuts down on manual work but also improves accuracy and generates audit-ready reports, freeing organisations to focus on making informed decisions that drive meaningful change.