ESG Reporting for Investor Relations: A Guide

Investors demand ESG data that integrates seamlessly with financial reporting. This shift is driven by regulatory updates like the UK Sustainability Reporting Standards (UK SRS), which become mandatory for financial years starting in 2026. ESG reporting is no longer just about compliance; it’s about connecting sustainability performance directly to financial outcomes.

Key takeaways:

- Regulatory changes: UK SRS, based on ISSB guidelines, prioritises financial materiality and requires audit-ready ESG data. Companies can use an ESG compliance checker to assess their current alignment.

- Investor focus: ESG factors now influence equity valuations, credit risks, and cost of capital.

- Data integration: Tools like neoeco align ESG metrics with financial systems (e.g., Xero, Sage), ensuring accuracy and transparency.

- Financial impacts: ESG themes, such as carbon pricing and governance practices, directly affect revenue, costs, and enterprise value.

To prepare, firms should prioritise climate-related disclosures, integrate ESG data with financial systems, and ensure reporting aligns with investor expectations. Platforms like neoeco simplify this process, offering transaction-level traceability and compliance-ready outputs.

The Role of Investor Relations in ESG Reporting

Investor Expectations and Regulatory Requirements

Investors today are weaving ESG (Environmental, Social, and Governance) data into their financial analyses, using it to evaluate equity valuations, credit risks, capital costs, and stewardship strategies. When ESG factors directly impact a company’s financial performance, they become critical to investment decisions. This shift means accounting firms must approach ESG disclosures with the same precision and reliability as traditional financial statements.

How Investors Use ESG Data

Investors rely on ESG data in several ways to inform their financial strategies:

- Equity Valuations: ESG data helps quantify sustainability risks and opportunities, which can influence future cash flows and, by extension, share prices.

- Credit Risk Assessments: Factors like environmental liabilities or governance practices are used to gauge the likelihood of default.

- Cost of Capital: ESG performance is factored into risk-based calculations, affecting how much it costs companies to access funding.

- Stewardship and Voting: Institutional investors use ESG metrics to engage with boards on key sustainability issues and to guide shareholder voting decisions.

At the heart of these applications lies the concept of financial materiality. Investors focus on ESG factors that have a tangible effect on financial outcomes, making this a cornerstone of ESG-related regulatory requirements.

Key Regulatory Frameworks for ESG Disclosure

The regulatory environment in the UK is shifting towards frameworks that prioritise investor-focused reporting. Two key standards - IFRS S1 (General Requirements for Disclosure of Sustainability-related Financial Information) and IFRS S2 (Climate-related Disclosures) - form the foundation of this approach. These standards emphasise single materiality, meaning they focus solely on sustainability issues that affect a company’s enterprise value.

Building on these, the UK Sustainability Disclosure Requirements (UK SDR) and UK Sustainability Reporting Standards (UK SRS) will become mandatory for financial years starting in 2026. These frameworks, finalised in late 2025, closely align with the recommendations of the Task Force on Climate-related Financial Disclosures (TCFD), which has already been widely adopted.

For accounting firms, this means moving beyond narrative ESG reporting. The focus is now on providing quantifiable, comparable data that investors can benchmark. Understanding how ISSB reporting integrates into financial strategies is essential for firms preparing their clients for these evolving demands.

| Framework | Materiality Approach | Primary Focus | Compliance Status |

|---|---|---|---|

| IFRS S1/S2 | Single materiality | Enterprise value and investor decisions | Global baseline; UK adoption via UK SRS |

| UK SDR/SRS | Single materiality | Financial impacts on the entity | Finalised late 2025; mandatory from 2026 |

| TCFD | Financial materiality | Climate-related financial risks and opportunities | Widely adopted; integrated into ISSB standards |

Financial Materiality Explained

Financial materiality narrows the focus of ESG reporting to factors that directly impact a company’s cash flows, access to financing, or cost of capital over varying time horizons. Unlike the broader concept of double materiality, which also considers a company’s impact on society and the environment, financial materiality asks a more targeted question: "How does this ESG factor affect our financial performance?"

This focus aligns with both investor priorities and regulatory requirements, pushing companies to link ESG themes directly to financial statements. For accounting firms, this means identifying which ESG factors are financially relevant by analysing industry-specific risks, regulatory pressures, and stakeholder concerns. Successfully integrating ESG data into the financial ledger is key to meeting these expectations and aligning with the emerging regulatory frameworks.

Connecting ESG Performance to Financial Outcomes

Let’s explore how performance in environmental, social, and governance (ESG) areas directly impacts financial results, building on the regulatory framework we’ve already discussed.

Investors are now weaving ESG data into their valuation models, recalculating enterprise value, tweaking discount rates, and refining cash flow projections. For accounting professionals, this highlights the growing importance of understanding how ESG considerations translate into measurable financial outcomes.

How ESG Factors Influence Financial Performance

ESG factors can significantly affect both the balance sheet and income statement. Take carbon pricing, for example. Whether through mechanisms like the UK Emissions Trading Scheme or internal shadow pricing, emissions are converted into tangible costs that directly impact operating margins. High Scope 1 emissions can lead to steep carbon costs, cutting into profitability. On the flip side, boosting energy efficiency can both lower operating costs and reduce carbon intensity - a win-win that investors are quick to notice when evaluating valuation multiples.

Stranded assets also pose a financial risk. Companies with large fossil fuel reserves or carbon-heavy infrastructure may see asset values drop as regulatory changes and market trends make recovery less likely. Fully understanding Scope 3 emissions with activity-based data and their impact across the value chain is essential for quantifying these risks effectively. Let’s dive into how specific ESG themes translate into financial impacts.

Mapping ESG Themes to Financial Statements

ESG themes leave a noticeable mark on financial statements. Climate risks, for instance, can disrupt revenues through market changes and regulatory hurdles, while also driving up capital expenditures for transition-related investments. Governance practices influence financing costs and risk premiums, and social factors can affect labour costs, productivity, and even brand reputation.

| ESG Theme | Financial Statement Impact | Investor Use Case |

|---|---|---|

| Climate risk (physical) | Revenue volatility, asset impairments, increased insurance costs | Scenario analysis, stress testing |

| Climate risk (transition) | Higher operating costs (e.g., carbon pricing), increased capital expenditures, stranded assets | Valuation adjustments, DCF modelling |

| Governance quality | Higher cost of capital, legal provisions, management compensation adjustments | Risk premium calculation, credit assessment |

| Social factors | Increased labour costs, changes in productivity, customer retention shifts | Operating margin analysis, brand valuation |

| Resource efficiency | Lower operating costs (energy, water, waste) and reduced Scope 1/2 emissions | EBITDA margin expansion, ESG scoring |

These impacts aren’t just static; dynamic models can provide even deeper insights into the financial implications of ESG factors.

Scenario Analysis and Carbon Pricing

Scenario analysis is a powerful tool for assessing how different climate pathways might affect financial performance over time. Investors, following TCFD recommendations, often evaluate a range of scenarios - from rapid decarbonisation to slower, more gradual transitions. Each scenario involves varying assumptions about carbon pricing, which directly influences operating costs and capital allocation decisions.

Discount rates also shift in response to ESG risks. Companies lagging in ESG performance often face higher costs of capital, and even small increases in discount rates can significantly reduce enterprise value. To fully integrate these insights, companies need to incorporate ESG factors into their financial planning processes. Using financially-integrated sustainability management approaches, accounting teams can embed these considerations into their frameworks, ensuring ESG factors are analysed with the same precision as traditional financial metrics.

Building Investor-Grade ESG Reporting Frameworks

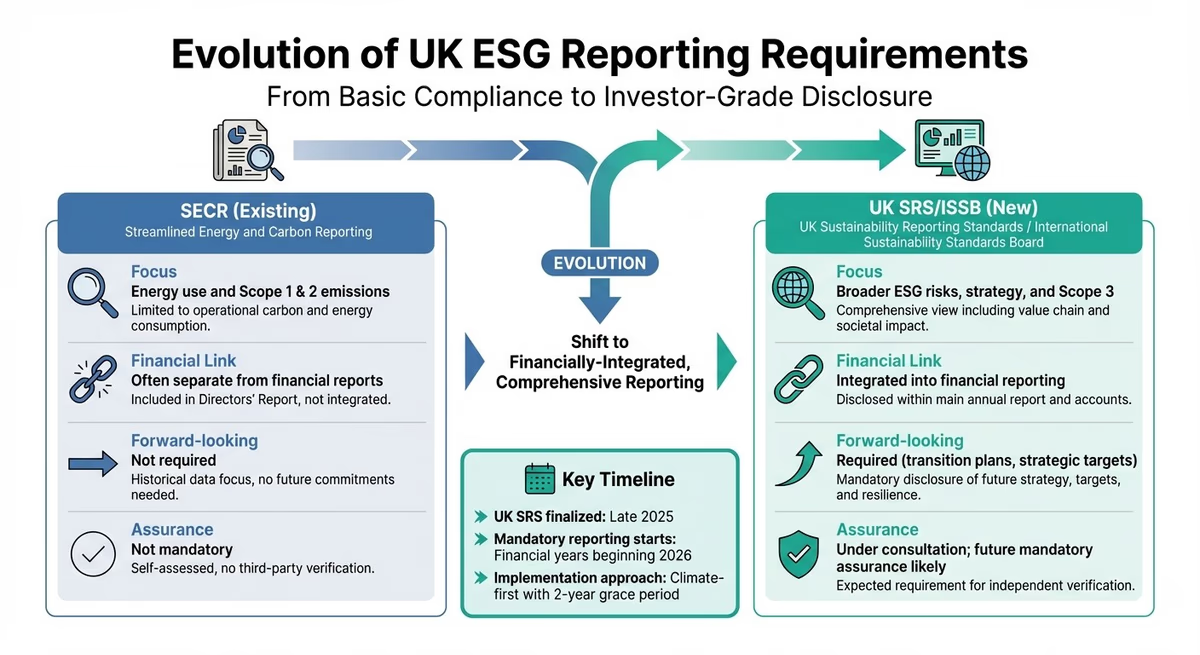

Evolution of UK ESG Reporting Requirements: SECR vs UK SRS/ISSB Standards

As ESG’s role in financial decision-making grows, accounting firms must create frameworks that resonate with investor expectations. The trend towards globally consistent standards - particularly with the International Sustainability Standards Board (ISSB) - demands a shift from simple compliance to producing disclosures that seamlessly align with financial reporting. These emerging standards are paving the way for the essential components of investor-grade ESG reporting.

Core Components of ESG Reporting

Investor-grade ESG reporting revolves around four key elements.

- Financial and double materiality assessments: These focus on identifying sustainability issues that genuinely impact enterprise value.

- Robust Metrics: Beyond carbon intensity, firms need to include governance indicators, forward-looking targets, and detailed transition plans.

- Strategic Disclosures: These outline how ESG risks and opportunities influence business strategies and capital allocation.

- Assurance Processes: While not yet mandatory under SECR, assurance adds credibility and is likely to become a requirement under frameworks like the UK Sustainability Disclosure Requirements (UK SRS) in the future.

The table below highlights how reporting requirements are evolving, moving from basic energy disclosures under SECR to a more comprehensive, financially integrated ESG framework:

| Feature | SECR (Existing) | UK SRS / ISSB (New) |

|---|---|---|

| Focus | Energy use and Scope 1 & 2 emissions | Broader ESG risks, strategy, and Scope 3 |

| Financial Link | Often separate from financial reports | Integrated into financial reporting |

| Forward-looking | Not required | Required (transition plans, strategic targets) |

| Assurance | Not mandatory | Under consultation; future mandatory assurance likely |

Source:

The UK SRS proposes a phased "climate-first" approach, giving companies up to two years to prioritise climate-related disclosures before expanding to other sustainability areas. This gradual implementation provides accounting firms with a roadmap to focus their efforts and build capacity for broader ESG reporting.

Integrating ESG into Financial Reporting

Once the core components are established, the next step is embedding ESG data directly into financial disclosures. The value of investor-grade ESG reporting lies in its ability to connect ESG metrics with financial data. For example, firms should align ESG categories with ledger accounts, ensuring that every emission figure or sustainability metric can be traced back to a specific financial transaction.

By linking ESG metrics to financial drivers, such as connecting carbon intensity to revenue, mapping energy costs to operating expenses, or tracking capital expenditure on transition projects, firms can ensure that ESG data is accurate, auditable, and reflective of overall business performance. This integration strengthens the credibility of ESG disclosures while providing a clearer picture of how sustainability efforts impact financial outcomes.

Using neoeco for ESG Reporting

For firms looking to streamline ESG reporting, neoeco offers an automated solution that leverages existing financial data. Operating seamlessly on platforms like Xero, Sage, and QuickBooks, neoeco maps transactions to recognised emissions categories, including those under GHGP, ISO 14064, and national frameworks.

The platform’s Sustainability Ledger monitors over 90 impact factors using life cycle assessment (LCA) methodology, ensuring transaction-level traceability. Built-in audit controls provide a live checklist that highlights completed, missing, or review-ready items. Compliance-ready templates enable firms to generate reports in minutes. For those preparing for ISSB reporting, neoeco delivers a financially integrated approach that aligns with investor expectations. By eliminating spreadsheets and manual data conversions, it ensures accurate, finance-grade carbon data and audit-ready reports, transforming ESG reporting from a compliance task into a strategic financial tool. This approach not only builds investor confidence but also aligns with the integrated reporting standards discussed earlier.

Strengthening Investor Relations Through ESG Reporting

ESG reporting has become a powerful way for businesses to align their sustainability goals with their overall strategy, helping to foster trust with investors. By weaving ESG data into financial communications, companies can highlight how their sustainability efforts contribute to long-term value, manage ESG risks, and influence decisions about capital allocation. This integration strengthens the foundation for meaningful conversations with investors.

Improving Investor Communications

Clear and effective communication with investors is essential, and ESG metrics play a key role in achieving this. Incorporating ESG data into annual reports, investor presentations, and bond documentation signals that sustainability is not just a side project but a core part of the financial strategy. For instance, showcasing how carbon reduction goals, energy efficiency investments, or supply chain improvements enhance operational performance and profitability makes the connection tangible. Linking renewable energy investments to cost savings is a practical example of this. Similarly, including ESG metrics in sustainability-linked bond documents demonstrates that financing terms are tied to measurable outcomes. This approach transforms ESG reporting into a central element of investor discussions, rather than a separate disclosure.

Building Credibility with Integrated ESG Data

To build trust with investors, ESG data must be consistent, reliable, and ready for audit. This reduces the risk of greenwashing and supports meaningful analysis over time. Investors are increasingly focused on whether ESG claims are backed by solid evidence, especially as sustainability-linked financial instruments gain popularity. Transaction-level ESG data ensures accuracy and provides a clear picture of performance trends. By offering this level of detail, companies can show year-on-year progress, pinpoint areas for improvement, and reassure investors that their disclosures reflect real business activities. This transparency strengthens the connection between sustainability initiatives and financial outcomes.

neoeco and Financially-Integrated Sustainability Management

neoeco takes ESG governance and reporting to the next level with its Financially-Integrated Sustainability Management (FiSM) approach. By operating directly on financial ledgers, neoeco ensures that every ESG metric is tied to a specific transaction, bridging the gap between financial and sustainability data. The platform’s built-in audit controls and ready-to-use templates enable companies to produce high-quality, investor-grade reports quickly, while maintaining the rigour needed for assurance processes. This integrated approach not only boosts investor confidence but also equips businesses to adapt to evolving regulatory requirements. By aligning financial and ESG reporting, companies can meet compliance demands while earning investor trust through clear, data-backed disclosures.

Conclusion

ESG reporting has become a cornerstone of investor relations. Today’s investors expect sustainability data to match the precision and transparency of financial statements. They rely on this information to evaluate risk, allocate resources, and assess long-term value. This requires robust ESG materiality evidence to support every claim. For accounting firms, this evolution presents both a challenge and an opportunity: the chance to act as trusted advisors who connect financial performance with sustainability outcomes.

The growing demand for reliable ESG metrics calls for a more structured, financially integrated approach. By linking sustainability data directly to financial transactions, these metrics become not only verifiable and auditable but also meaningful. This ensures the delivery of ESG data that meets audit standards. With the UK SRS final standards anticipated by late 2025 and mandatory reporting likely starting for financial years beginning in 2026 or 2027, firms have limited time to prepare clients for compliance while also bolstering investor trust.

Platforms like neoeco simplify ESG reporting by connecting every financial transaction to recognised emissions categories, ensuring data is audit-ready. This forms the basis of Financially-Integrated Sustainability Management (FiSM) - a framework designed to align financial and sustainability reporting, helping both clients and firms stay ahead of the curve.

The initial focus should be on climate disclosures. The two-year grace period under UK SRS provides a valuable opportunity to refine carbon reporting before expanding into other areas of sustainability. By prioritising a climate-first strategy and using tools that integrate ESG data with financial systems, accounting firms can enhance investor confidence, navigate evolving regulations, and position themselves as leaders in sustainability assurance. This integrated approach cements ESG reporting as a powerful asset in investor relations.

FAQs

How will the UK Sustainability Reporting Standards affect businesses from 2026?

From 2026, the UK Sustainability Reporting Standards (UK SRS) will take over from the SECR framework, introducing stricter requirements for companies to submit detailed climate and sustainability reports aligned with ISSB standards. These disclosures will play a key role in helping investors and lenders assess risks, identify financing opportunities, and monitor performance.

What’s changing? These new standards won’t just affect large corporations - they’ll also extend to SMEs and their supply chains starting in late 2025. The goal is to enhance transparency and hold businesses accountable, ensuring they’re ready to meet the rising demand for sustainability-focused reporting.

What is financial materiality, and why is it important in ESG reporting?

Financial materiality, often called single materiality within the ISSB framework, focuses on how ESG factors influence a company’s financial performance. This includes metrics like cash flow, costs, and overall valuation. The goal here is to ensure that ESG disclosures remain relevant to investors, showing how sustainability risks and opportunities directly impact financial outcomes. This approach aligns with standards such as IFRS S1 and S2.

To determine financial materiality, companies typically assess ESG topics that hold financial relevance. This involves gathering stakeholder input and analysing how these issues might affect revenue, costs, risks, and asset values. By weaving these findings into financial reports, businesses give investors a transparent view of how sustainability efforts shape long-term value creation.

Accounting firms can simplify this process using tools like neoeco. This platform connects transaction data to recognised emissions categories and ties ESG metrics directly to financial statements. The result? Accurate, compliant, and audit-ready disclosures that not only meet regulatory standards but also strengthen investor confidence.

How can businesses seamlessly integrate ESG data into their financial systems?

Integrating ESG data into financial systems means weaving sustainability metrics directly into accounting processes, rather than treating them as separate reports. By using frameworks like ISSB, SASB, or GRI, businesses can link ESG factors with financial performance, giving investors a clearer understanding of how sustainability drives long-term value. This approach also helps meet UK-specific standards such as SECR and the Sustainability Reporting Standards (SRS).

Platforms that automatically match financial transactions to recognised emissions categories - like GHGP or ISO 14064 - make this task much easier. Tools such as neoeco can connect effortlessly with accounting software like Xero, Sage, or QuickBooks. This removes the need for manual data input while ensuring precise, finance-grade carbon reporting. To streamline this process, businesses should prioritise standardising data collection, automating supplier data (including Scope 3 emissions), and embedding ESG metrics into routine financial reports. This not only simplifies compliance but also builds trust with investors.