How Financial Data Powers Sustainability Reporting

Financial data is the backbone of sustainability reporting. It links expenses like energy bills or freight costs directly to emissions under frameworks like GHGP, SECR, and ISO 14064. By integrating sustainability metrics into financial systems, businesses can create accurate, audit-ready reports while saving time and reducing errors. This method, called Financially-Integrated Sustainability Management (FiSM), automates data collection and maps transactions to emissions categories in real time.

Key Takeaways:

- FiSM Approach: Uses financial tools (e.g., Xero, Sage) to streamline emissions reporting.

- Compliance: Aligns with standards like SECR, UK SRS, and ISSB.

- Automation Benefits: Cuts manual errors, ensures accuracy, and speeds up reporting.

- Controls: Applies financial principles (accuracy, completeness, consistency) to sustainability data.

- Metrics Integration: Combines emissions data with financial reports for better decision-making.

This approach not only simplifies compliance but also helps businesses track emissions, set reduction targets, and align sustainability goals with financial performance.

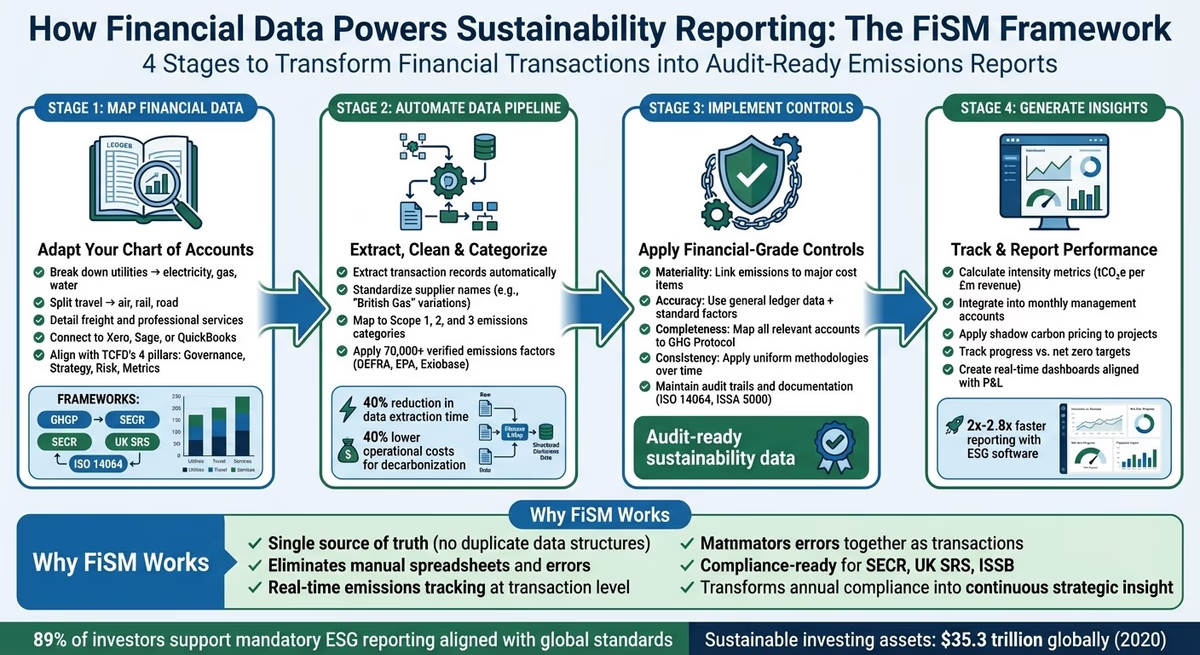

FiSM Framework: From Financial Data to Sustainability Insights - 4 Key Stages

Mapping Financial Data to Sustainability Reporting Requirements

Understanding Framework Requirements and Data Needs

In the UK, reporting standards like SECR (Streamlined Energy and Carbon Reporting) and UK SRS (UK Sustainability Reporting Standards), along with international frameworks such as the GHGP (Greenhouse Gas Protocol) and ISO 14064, require businesses to link emissions data directly to their activities. For instance, SECR obliges large UK companies to disclose energy consumption and greenhouse gas emissions, while UK SRS takes a financial materiality approach, focusing on ESG factors that could impact a company’s economic performance. This contrasts with European standards, which adopt a "double materiality" perspective by examining both financial and environmental impacts.

"We identified that a lot of the foundational data required for ESG reporting is held by accountants and finance teams. They play a key role in sustainability reporting by managing critical accounting data." - Jake Bond, VP of Business Development, neoeco

Compliance with UK SRS is rolled out in stages: Year 1 focuses on climate metrics excluding Scope 3 emissions, Year 2 adds Scope 3, and by Year 3, reporting extends to all sustainability factors. While your accounting ledger already contains much of the required data, the real challenge lies in mapping it accurately. This highlights the importance of fine-tuning your accounting structure to meet these evolving demands.

Adapting Your Chart of Accounts for Sustainability Data

There’s no need to completely overhaul your existing chart of accounts. Instead, it’s about aligning it with the TCFD's four pillars: Governance, Strategy, Risk Management, and Metrics/Targets. To do this, transaction categories - such as travel, energy, freight, and professional services - should be detailed enough to correspond with emissions sources under the GHGP methodology.

For instance, instead of a single "Utilities" category, break it down into electricity, gas, and water. Similarly, divide "Travel" into categories like air, rail, and road. This level of granularity makes it easier to map transactions to specific emissions factors. Tools like neoeco simplify this process by connecting directly to accounting platforms like Xero, Sage, or QuickBooks with read-only access. These platforms automatically link ledger entries to Scope 1, 2, and 3 emissions categories, ensuring your sustainability data is audit-ready from the outset.

Using Accounting Systems as Data Sources

Modern accounting systems already house the transaction data needed for sustainability reporting. By integrating sustainability software with platforms like Xero, Sage, or QuickBooks, every invoice, receipt, and payment becomes a potential data point for calculating emissions. The software pulls transaction details and applies recognised emissions factors to create carbon accounts.

"The need to demonstrate your ESG credentials is being driven by top-down regulation currently impacting larger businesses, and it's beginning to be pushed down the supply chains." - Laurie Hill, Partner, Larking Gowen

This integration ensures that sustainability data can be published alongside financial statements, as required under UK standards. By embedding sustainability reporting into your financial processes, you streamline compliance and improve transparency without adding unnecessary complexity.

Building an Automated Data Pipeline for Emissions Reporting

Extracting, Cleaning, and Standardising Financial Data

The first step in preparing for emissions reporting is to extract, clean, and standardise your financial data. This process involves gathering transaction records from your accounting system, addressing any inconsistencies, and ensuring a uniform format. For instance, supplier names can vary across invoices - "British Gas" might also appear as "BG Energy", "British Gas Ltd", or "BG Business". Normalising these variations is crucial for accurate categorisation.

Automation can cut data extraction time by up to 40%, eliminating the need for manual spreadsheet exports and tedious cross-referencing. Advanced platforms tap into over 70,000 verified emissions factors from databases like DEFRA, US EPA, and Exiobase, ensuring your calculations meet established standards. AI-powered Natural Language Processing (NLP) can even extract greenhouse gas data from unstructured documents like invoices and receipts. When supplier emissions data is unavailable, estimation models step in to fill the gaps.

"Leveraging AI-driven automation for GHG emission data extraction empowers organizations to transform ESG reporting from a manual burden into a streamlined, reliable process." – Decimal Point Analytics

Once your data is clean and standardised, the next step is mapping each transaction to its corresponding emissions category.

Mapping Transactions to Emissions Categories

The key to effective emissions reporting lies in linking every standardised transaction to the appropriate emissions category under frameworks like the Greenhouse Gas Protocol (GHGP) or ISO 14064. For example, electricity invoices typically fall under Scope 2 (purchased energy), while business travel expenses are categorised under Scope 3 (Category 6: Business Travel).

Scope 3 is often the most complex, as it includes indirect emissions across your supply chain - from purchased goods and services to employee commuting and waste disposal. AI algorithms simplify this process by identifying and verifying emissions data from suppliers and investments, which can otherwise be a significant challenge. Additionally, automation tools interface directly with supplier systems via APIs, providing real-time updates without the need for manual follow-ups. For more on aligning these efforts with financial strategies, learn how to align ESG data with ISSB standards.

Accurate mapping is essential, as it underpins the automation needed to improve data precision.

How Automation Improves Accuracy

Manual processes, such as relying on spreadsheets or email chains, often lead to errors and create challenges for maintaining clear audit trails. Automated systems like neoeco address these issues by connecting directly to platforms such as Xero, Sage, or QuickBooks with read-only access. These systems pull transaction data and apply recognised emissions factors in real time, eliminating manual conversions and ensuring every calculation is traceable back to the original ledger entry.

AI-driven efficiencies in carbon data collection can lower operational costs related to decarbonisation by as much as 40%. By automating data mapping and calculations, companies reduce errors and improve their readiness for audits. Built-in controls provide live checklists and store supporting documentation to meet ISO 14064 or ISSA 5000 audit requirements. This approach transforms sustainability reporting into a seamless process that integrates directly with financial records, creating a reliable and audit-ready framework for emissions reporting.

Implementing Controls and Assurance for Sustainability Data

Applying Accounting Principles to Sustainability Metrics

To ensure sustainability data is as dependable as financial records, robust control measures are essential. Just as FiSM simplifies data collection, these controls safeguard the accuracy and audit-readiness of sustainability metrics.

By applying financial reporting principles - materiality, accuracy, completeness, and consistency - to sustainability data, you can link major emission sources to significant cost items. For UK accounting firms, this involves prioritising climate and ESG matters that could reasonably affect financial statement users. Materiality can be defined by connecting key emission sources to major cost lines in the profit and loss account, such as purchased goods, logistics, or business travel. For accuracy, finance-grade data - like supplier spend, energy bills, and fuel costs - should be drawn from general ledgers, bank feeds, and subledgers, with standard emission factors and automated calculations applied. Completeness involves mapping all relevant accounts and vendors to emission categories under frameworks like the GHG Protocol, SECR, UK SRS, or ASRS 2, and regularly identifying unmapped transactions. Consistency requires clear methodologies, such as which emission factor database to use or how to handle estimates, and applying these consistently over time, with any changes justified and disclosed. Aligning these principles with those used in statutory audits and SECR energy and carbon disclosures ensures partners and reviewers can rely on a unified approach.

Setting Up Data Governance and Internal Controls

Effective governance begins with clearly defined roles:

- Executive Owner: Typically the CFO or a senior ESG partner, accountable for the reliability and completeness of sustainability reporting.

- Data Steward: An ESG controller or member of the finance/sustainability team who oversees processes like system configuration, mapping rules, and exception management.

- Data Owners: Individuals from operational areas (e.g., procurement, HR, facilities) responsible for maintaining accurate and timely data inputs, such as energy bills or travel records.

A well-structured RACI matrix clarifies responsibilities, detailing who approves methodologies, updates emission factors, and signs off disclosures in line with frameworks like SECR and ISO 14064. Centralised software with role-based access and audit trails enforces governance by controlling who can modify mappings, emission factors, or reported figures. For firms handling clients across multiple regions, local coordinators ensure compliance with region-specific frameworks (e.g., UK SECR versus Australian ASRS 2) while maintaining a consistent firm-wide methodology. Tools such as neoeco, which integrate directly with clients' financial ledgers, provide system-level controls, templates, and automated validation, reducing spreadsheet dependency and demonstrating control effectiveness to regulators and assurance providers.

Key controls mirror those in financial reporting. Input controls include automated data feeds from systems like accounting, HR, and utilities, with validation checks for missing fields, duplicates, or anomalies. Processing controls involve locked mapping rules between accounts and emission categories, controlled updates to emission factors, and versioning of calculation methodologies to maintain traceability. Reconciliation controls ensure that emissions calculations align with general ledgers and subledgers, with tolerances and documented explanations for discrepancies. Review controls use analytical techniques akin to financial analytics, such as trend analysis of emissions (tCO₂e) by category, intensity ratios (e.g., tCO₂e per £m revenue), and comparisons of energy usage against prior periods or operations.

These controls integrate seamlessly with existing procedures, bolstering the audit-ready nature of sustainability data.

Maintaining Audit-Ready Documentation

Standards like ISO 14064-1 require detailed documentation of organisational and operational boundaries, base year, reporting period, and methodologies. This includes emission factors, data sources, and calculation steps for each emission category. Similarly, UK SECR mandates documented methodologies for energy and emissions calculations, intensity ratios, and any material estimation techniques, along with evidence for kWh, fuel use, and any exclusions. A structured digital binder should be maintained, with sections for governance, methodologies, data sources, calculations, reconciliations, and management approvals. Each major data stream - such as electricity, gas, fleet fuel, or air travel - should have dedicated workpapers detailing the source, extraction method, transformations, and control checks. ESG platforms with built-in audit trails simplify compliance by automatically storing calculation logic, factor sets, user actions, and report versions.

Documentation should also cover emission factor sources (e.g., BEIS/Defra for the UK or IPCC), the version and date used, and any overrides. Allocation methods for shared data across sites or entities should include allocation keys and rationale. When direct data isn’t available, estimation techniques should be explained, along with how uncertainty is handled (e.g., data gaps or proxies). Changes in methodology year-on-year should be quantified for comparability. For SECR, firms must also document chosen intensity metrics and their relevance to decision-making. Assurance providers will expect a clear link between methodologies and reported figures, as well as evidence of reviewed and approved significant judgements.

Turning Financial Data into Sustainability Insights

Calculating Key Sustainability Metrics

To measure environmental efficiency, calculate intensity metrics like carbon, energy, and water intensity. These metrics - such as emissions or energy use per unit of revenue - help standardise sustainability performance, making comparisons over time straightforward.

For instance, carbon intensity is calculated by dividing total greenhouse gas (GHG) emissions (measured in tCO₂e) by revenue (£m). If a manufacturing business generates £5m in revenue and emits 250 tCO₂e, its carbon intensity is 50 tCO₂e per £m. A rise in revenue with unchanged emissions would show a lower carbon intensity, highlighting a decoupling of emissions from growth. Similarly, energy intensity is determined by dividing total energy consumption (kWh) by revenue or production volume. In real estate, Energy Use Intensity (EUI) - energy usage per square foot - provides a benchmark for comparing building performance across properties. Water intensity, calculated as consumption per occupant, is another metric used to evaluate resource efficiency in commercial or residential spaces.

When calculating these metrics, it’s crucial to normalise for factors like production volume, occupancy, or even weather conditions. Select a denominator that aligns with your client’s primary business operations and stays consistent over time. For example, a logistics company might track emissions per tonne-kilometre, while a professional services firm might use emissions per full-time equivalent employee.

These metrics lay the groundwork for embedding sustainability into broader financial decision-making.

Integrating Sustainability Metrics into Financial Reporting

Once key metrics are calculated, the next step is integrating them into financial reporting. By embedding sustainability data into regular financial documents - such as management accounts, board reports, and budget reviews - you can turn these insights into actionable strategies. Instead of relying solely on standalone ESG reports, include carbon and energy metrics in monthly or quarterly updates. For example, a management accounts pack could present revenue, gross margin, and operating costs alongside carbon intensity, energy expenditure, and progress towards reduction targets.

One powerful tool is shadow carbon pricing, which assigns an internal cost per tCO₂e to project evaluations. This allows finance teams to account for potential future emissions costs in net present value (NPV) calculations, even before regulatory carbon taxes are implemented. For instance, when comparing two warehouse fit-outs, applying a shadow price to projected energy use might make energy-efficient options like LED lighting and heat pumps more financially attractive, even if their upfront costs are higher.

Another approach, Lifecycle Cost Analysis (LCCA), takes this one step further by evaluating the total cost of ownership, including environmental and social impacts, rather than focusing solely on initial ROI. For example, investing in green building practices can increase a property’s value by 10% or more, a consideration that should inform both internal decisions and client recommendations. Tools like neoeco simplify this process by pulling emissions data directly from financial ledgers, offering real-time dashboards that align carbon metrics with profit and loss statements.

Using Data to Track Decarbonisation Targets

Financial data can also be a powerful tool for tracking progress towards net zero or science-based targets. By monitoring emissions at the transaction level, you can pinpoint which cost centres, suppliers, or activities contribute the most to a client’s carbon footprint - and identify where reductions will have the greatest impact. For example, a client aiming for a 30% reduction in Scope 1, 2, and 3 emissions by 2030 could use monthly ledger data to track energy costs, fuel consumption, and refrigerant usage, comparing actual performance against their baseline and reduction trajectory.

Making sustainability metrics visible can also make budget allocation more strategic. If business travel is a client’s largest emission source, finance teams can set departmental carbon budgets alongside financial budgets, flagging overspending in both monetary and carbon terms. This dual approach ensures that decarbonisation becomes a core part of resource planning and performance assessment. For more guidance, check out the FiSM manifesto, which outlines principles for integrating financial and sustainability management.

Data also enables scenario modelling. For example, what happens if a company switches to renewable electricity? Or electrifies its fleet? By linking these scenarios to actual spending data, finance teams can estimate the carbon and cost implications of different strategies. This helps clients make informed, evidence-based decisions rather than relying on aspirational targets. With 89% of investors now backing mandatory ESG reporting aligned with global standards, and sustainable investing assets reaching $35.3 trillion globally in 2020, demonstrating credible progress backed by data isn’t just a compliance issue - it’s a competitive edge.

This approach aligns with the FiSM framework, transforming financial transactions into actionable sustainability insights.

Comparing and Contrasting Financial Reporting to Sustainability Reporting: Patricia Dechow ASW2023

Conclusion

Financial data serves as the most dependable backbone for sustainability reporting because it reflects a business's true operational landscape - covering energy expenses, travel, procurement, and capital investments. By building carbon accounting directly onto the general ledger, accounting firms can produce detailed, auditable, and framework-compliant disclosures without duplicating data structures or relying on potentially error-prone spreadsheets. This approach ties sustainability data directly to the trial balance, creating a single, trusted source of truth. The result? Streamlined automation and stronger internal controls.

Automation plays a key role here. Firms utilising ESG software achieve results 2x–2.8x faster, while automated platforms eliminate the laborious tasks of manual data entry, validation, and reconciliation. This efficiency allows specialists to focus on delivering what clients value most: actionable insights, decarbonisation strategies, and high-level advisory services. Tools like neoeco exemplify this approach by operating directly on clients' financial ledgers, automatically categorising transactions into recognised emissions categories. The outcome is finance-grade carbon data and audit-ready reports, all without the hassle of spreadsheets or manual data conversions.

Beyond automation, maintaining strong controls is equally vital for sustainability data, just as it is for financial reporting. Clear data ownership, rigorous validation rules, reconciliations tied to the ledger, comprehensive audit trails, and well-documented methodologies ensure carbon accounts can withstand regulatory scrutiny and third-party assurance. As reporting requirements tighten in regions like the UK and Australia, firms that establish systematic processes for sustainability data now will be better equipped to support clients and mitigate risks effectively.

In line with the FiSM framework, integrating sustainability metrics into financial reporting transforms compliance from an annual chore into a continuous source of strategic insight. Embedding these metrics into monthly management accounts, budget reviews, and board reports enables firms to help clients monitor decarbonisation progress, identify emissions hotspots, and assess the financial implications of reduction strategies. This evolution - from one-off annual reports to ongoing, integrated sustainability management - is at the heart of the FiSM manifesto and represents the future of professional practice. Firms adopting this model stand to not only enhance their offerings but also unlock new recurring revenue streams and secure a more resilient future for both their clients and themselves.

FAQs

How does Financially-Integrated Sustainability Management (FiSM) enhance the accuracy of emissions reporting?

FiSM enhances the precision of emissions reporting by directly connecting financial data to recognised emissions categories. This ensures results are both accurate and consistent. By automating the mapping of transaction-level data and validating it instantly, it removes the common risks of manual errors often linked to spreadsheet-based processes.

The result? Audit-ready carbon figures that meet the requirements of widely accepted standards, including the GHGP, ISO 14064, and UK-specific frameworks like SECR and UK SRS. With FiSM, you can rely on sustainability reports that are dependable and align with established guidelines.

What are the advantages of integrating sustainability metrics into financial systems?

Integrating sustainability metrics into financial systems brings clear advantages for accounting firms and their clients. By linking data such as carbon emissions, energy consumption, and other ESG factors directly to financial ledgers, organisations can do away with manual data entry and minimise the use of spreadsheets. This not only saves time but also reduces errors. The result? Accurate, audit-ready reports that comply with both financial and sustainability guidelines, including frameworks like the GHGP, ISO 14064, and the UK SRS.

This kind of integration also enables smarter decision-making by offering real-time insights into how sustainability efforts influence financial outcomes. Dashboards that combine profitability metrics with data on carbon intensity or water usage empower leaders to make more informed, strategic choices. For accounting firms, automation simplifies the process of managing reports for multiple clients, making it easier to scale services while adhering to evolving UK regulations such as SECR and Sustainability Reporting Standards.

Tools like neoeco highlight these benefits by delivering finance-grade precision, cost savings, and regulatory assurance. They achieve this by categorising transactions under recognised emissions categories and automating carbon reporting - completely removing the need for spreadsheets.

How can businesses adapt their accounting systems to meet sustainability reporting standards?

Businesses can streamline sustainability reporting by integrating ESG data directly into their existing accounting systems, treating it as an extension of their financial processes rather than a separate task. The first step is to centralise all relevant data - think financial transactions, utility bills, travel records, and supplier invoices - into one platform. Tools like neoeco, which use the 'Financially-integrated Sustainability Management' (FiSM) approach, make this easier by connecting seamlessly with accounting software like Xero, Sage, or QuickBooks. These tools automatically categorise transactions according to established standards such as the Greenhouse Gas Protocol, ISO 14064, SECR, or UK Sustainability Reporting Standards (UK SRS), eliminating the need for manual data conversions.

After centralising the data, automation becomes essential. Real-time inputs from energy meters, HR systems, or supplier platforms can replace clunky, error-prone spreadsheets, cutting down on manual work and reducing mistakes. Automated systems not only simplify compliance with evolving regulations but also create audit-ready reports in no time. By aligning financial data with ESG frameworks like ISSB, GRI, or TCFD, businesses can generate precise, regulator-compliant disclosures while saving both time and resources. This integrated approach is flexible enough to adapt as a company grows or incorporates new ESG metrics, ensuring long-term efficiency and accuracy.