GHG Protocol vs CSRD: Data Alignment Guide

Navigating GHG Protocol and CSRD Compliance

Meeting both GHG Protocol and CSRD requirements is now a mandatory challenge for UK and EU organisations. The GHG Protocol provides a standard for tracking emissions, while CSRD enforces strict reporting rules, especially around Scope 3 emissions. Misalignment can lead to incomplete reports, especially with CSRD's focus on detailed data and double materiality (financial and environmental impacts).

Key points to know:

- GHG Protocol: Focuses on measuring emissions across three scopes (direct, indirect energy, and value chain emissions). It offers flexibility in organisational boundaries and reporting metrics.

- CSRD: Requires mandatory disclosures across all scopes, detailed segmentation of Scope 3 emissions, and GHG intensity metrics. Operational control boundaries are mandatory, with stricter rules for biogenic emissions and carbon credits.

- Scope 3 Challenges: Supply chain emissions can account for 60% of total emissions and demand accurate activity-based data collection from suppliers or financial systems.

- New Updates: The GHG Protocol introduced the Land Sector and Removals Standard on 30 January 2026, adding new guidelines for land-use and CO₂ removal technologies.

Aligning these frameworks requires integrating emissions data with financial systems, automating calculations, and ensuring audit-ready reporting. Tools like neoeco simplify this process by linking financial records directly to emissions categories.

| Feature | GHG Protocol | CSRD |

|---|---|---|

| Primary Goal | Emissions measurement for strategy | Regulatory transparency and consistency |

| Organisational Boundary | Flexible (Equity Share, Financial/Operational Control) | Mandatory Operational Control |

| Reporting Metric | Absolute emissions (CO2e) | Absolute emissions + GHG intensity (per net revenue) |

| Scope 3 Details | Optional segmentation | Mandatory detailed segmentation |

| Materiality | Inventory completeness | Double materiality (financial and environmental impacts) |

To comply effectively, start with GHG Protocol for baseline emissions, segment Scope 3 data, and integrate financial systems for streamlined reporting. Automation tools ensure precision and reduce manual effort.

GHG Protocol vs CSRD: Key Differences in Emissions Reporting Requirements

Sustainability now: Inside the GHG Protocol’s scope 3 update

What is the GHG Protocol?

The GHG Protocol, developed by the World Resources Institute (WRI) and the World Business Council for Sustainable Development (WBCSD), is the global standard for measuring carbon footprints. It serves as the technical backbone for corporate greenhouse gas (GHG) reporting programmes worldwide, covering seven key greenhouse gases: carbon dioxide (CO2), methane (CH4), nitrous oxide (N2O), hydrofluorocarbons (HFCs), perfluorocarbons (PFCs), sulphur hexafluoride (SF6), and nitrogen trifluoride (NF3).

Its widespread adoption underscores its credibility. By 2016, 92% of Fortune 500 companies responding to CDP were using the protocol either directly or indirectly. This universal standardisation benefits accounting firms managing clients across different regions by providing a consistent methodology, eliminating the need to juggle multiple conflicting standards. This consistency is built into the protocol's main components, which are outlined below.

Main Components of the GHG Protocol

The GHG Protocol includes several interlinked standards, each addressing specific areas of carbon accounting. The Corporate Standard is the foundation for creating GHG inventories at the corporate level, while the Scope 2 Guidance focuses on emissions from purchased electricity, steam, heat, and cooling. The Corporate Value Chain (Scope 3) Standard enables companies to assess emissions across their entire value chain, and the Product Standard measures the life cycle emissions of individual products or services.

On 30 January 2026, the protocol introduced the Land Sector and Removals Standard, a global framework for accounting for emissions from agricultural land use and technological CO2 removal methods like direct air capture. This addition reflects the increasing role of carbon removal solutions in achieving net-zero goals.

Emissions are categorised into three scopes under the protocol:

- Scope 1: Direct emissions from sources owned or controlled by the company, such as boilers, company vehicles, or on-site combustion.

- Scope 2: Indirect emissions from the generation of purchased electricity, heating, cooling, or steam.

- Scope 3: All other indirect emissions within the value chain, including those from purchased goods and services, waste management, employee commuting, and business travel.

These categories are crucial for practical carbon accounting, particularly for firms working with a variety of clients. When direct supplier data is unavailable, firms can use financially integrated approaches to Scope 3 emissions, extracting emissions data directly from purchase records instead of relying on supplier disclosures.

How Accountants Use the GHG Protocol

For accountants, the GHG Protocol serves as a bridge between carbon data and financial systems, enabling compliance with frameworks like SECR and ISO 14064. Tools like Xero, QuickBooks, and Sage allow firms to integrate carbon metrics into financial records, streamlining the process and ensuring audit-ready reporting.

The protocol requires accountants to start by defining boundaries - both organisational (which entities are included) and operational (which emission sources fall under each scope). Next, they convert activity data, such as litres of fuel or kilowatt-hours of electricity, into CO2e values using recognised emission factor databases. For Scope 3 reporting, emissions are broken down into 15 categories, including purchased goods and services (Category 1), business travel (Category 6), and the use of sold products (Category 11).

In complex supply chains, firms often use the hybrid method, which blends supplier-specific data with secondary industry averages to fill in gaps. This approach is particularly useful for small and medium-sized enterprises (SMEs) with diverse supply chains and limited access to detailed data. Automation further simplifies this process by categorising transactions into carbon data groups in real time, reducing manual errors and ensuring consistency across client portfolios.

The GHG Protocol’s neutral design makes it the backbone for mandatory regulations like the EU’s CSRD, the UK’s SECR, and the SEC’s climate disclosure rules. This adaptability is invaluable for accounting firms navigating multiple regulatory frameworks, allowing them to align supply chain data with both GHG Protocol and CSRD requirements efficiently.

What is CSRD and ESRS E1?

The Corporate Sustainability Reporting Directive (CSRD) is the European Union's mandatory sustainability reporting framework, designed to support the region's 2050 net-zero goal. Unlike voluntary standards, CSRD is legally binding - companies operating in the EU, along with certain non-EU entities with a significant presence in European markets, must comply or face penalties.

Central to CSRD is ESRS E1, the standard dedicated to climate change reporting. This standard outlines detailed requirements for both qualitative and quantitative climate-related disclosures. To meet these demands, businesses must pair precise emissions data with structured, compliant reporting methods. Below, we’ll explore the key requirements of CSRD and how its approach differs from the GHG Protocol.

What CSRD Requires

CSRD mandates reporting on emissions across all scopes. Initially, companies must focus on Scope 1 and 2 emissions - covering direct emissions and purchased energy - before tackling the more complex Scope 3 emissions from their value chains in later phases. This phased approach allows businesses time to develop reliable systems for tracking supply chain data. Starting early on Scope 3 preparations can save companies from last-minute challenges as deadlines approach.

A cornerstone of CSRD is the concept of double materiality. This means companies must evaluate two perspectives: how sustainability issues affect their financial performance (outside-in) and how their operations impact society and the environment (inside-out). ESRS E1 requires both numerical emissions data and narrative disclosures, ensuring that companies not only measure emissions accurately but also explain how climate considerations influence their strategies. These disclosures include climate transition plans, governance structures, risk management approaches, and details on how climate factors shape decision-making.

Another important requirement is the separate disclosure of biogenic emissions. This gained clarity when the GHG Protocol released its Land Sector and Removals Standard on 30 January 2026. This standard provides guidelines for accounting for emissions from agricultural land use and CO2 removal technologies like direct air capture. These updates are particularly relevant for businesses with agricultural or forestry operations in their supply chains.

How CSRD Differs from Other Frameworks

While CSRD builds on the GHG Protocol's measurement principles, it introduces additional reporting obligations, including more detailed value chain analysis and market-based emissions data. For Scope 2 emissions, CSRD requires companies to report market-based figures - such as renewable energy certificates and power purchase agreements - in addition to location-based averages. This level of detail ensures a more accurate reflection of a company’s energy use and its sustainability efforts.

Furthermore, CSRD demands a deeper dive into value chain emissions than the GHG Protocol typically requires. Companies must map emissions across their entire supply network with greater precision. Unlike the voluntary nature of GHG Protocol reporting, CSRD enforces compliance for all entities affected by EU regulations.

In 2023, 97% of S&P 500 companies using the GHG Protocol for CDP reporting highlighted its dominance in emissions measurement. However, firms operating internationally must now adapt to align their ISSB reporting with CSRD’s expanded disclosure demands, ensuring compatibility with both frameworks in an increasingly complex regulatory environment.

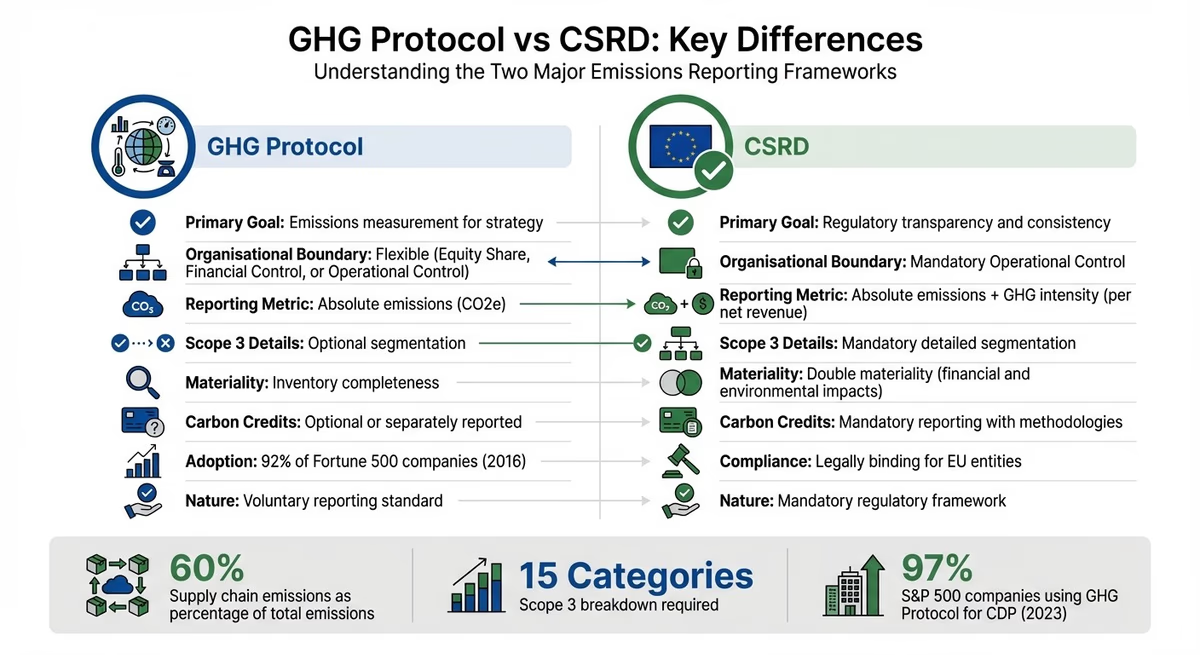

GHG Protocol vs CSRD: Main Differences

Understanding the distinctions between the GHG Protocol and CSRD is crucial for accurate supply chain emissions reporting. Both frameworks categorise emissions into Scopes 1, 2, and 3, but their objectives set them apart. The GHG Protocol is primarily used for voluntary reporting, whereas CSRD enforces mandatory compliance for companies operating within the EU.

Scope Definitions and Boundaries Compared

CSRD establishes stricter requirements compared to the GHG Protocol, particularly concerning organisational boundaries. The GHG Protocol allows flexibility, letting companies choose between equity share, financial control, or operational control approaches. In contrast, CSRD mandates the use of operational control boundaries, requiring firms to account for all entities under their operational control, regardless of ownership stakes.

Additionally, CSRD requires emissions to be disclosed in absolute terms (metric tonnes of CO2eq) before accounting for removals or offsets. Companies must also separately report biogenic emissions and removals, distinguishing between those within and outside the value chain. This aligns with the GHG Protocol's Land Sector and Removals Standard, which, starting 30 January 2026, will provide methodologies for quantifying CO2 removals from land use and technologies like Direct Air Capture.

A notable emphasis of CSRD is on double materiality - companies must evaluate both how climate issues influence their financial performance and how their operations impact the environment. The GHG Protocol, on the other hand, focuses on delivering a comprehensive and accurate inventory of emissions.

These stricter boundary and disclosure requirements set the stage for the more detailed data reporting obligations outlined below.

Data Requirements Compared

CSRD introduces mandatory disclosure of GHG intensity (emissions per net revenue), a metric that is optional under the GHG Protocol. Additionally, companies must break down Scope 3 emissions into specific categories rather than reporting a single total. For firms with complex supply chains, this necessitates integrating financial and environmental data systems to calculate intensity and track Scope 3 emissions across multiple categories.

CSRD also requires detailed reporting on carbon credits used to offset emissions, including the methodologies behind their calculation. While the GHG Protocol addresses removals and credits in separate guidance, CSRD makes these disclosures obligatory. Moreover, companies are expected to prioritise collecting primary activity-based data from value chain partners to improve the accuracy of Scope 3 reporting. This shift from estimation to verified supplier data presents a significant challenge for accounting firms assisting clients with compliance.

| Feature | GHG Protocol (Corporate Standard) | CSRD (ESRS E1) |

|---|---|---|

| Primary Goal | Provide a comprehensive account of emissions for management and strategy | Ensure transparency, consistency, and comparability for regulatory purposes |

| Organisational Boundary | Choice of Equity Share, Financial Control, or Operational Control | Mandatory Operational Control boundary |

| Reporting Metric | Absolute emissions (tonnes CO2e) | Absolute gross emissions and GHG intensity (per net revenue) |

| Removals | Covered in the Land Sector and Removals Standard | Mandatory disclosure of removals, storage, and biogenic emissions |

| Materiality | Focus on inventory completeness | Emphasises "Double Materiality" (evaluating both climate impacts and financial effects) |

| Carbon Credits | Optional or separately reported | Mandatory reporting, including methodologies used |

These differences in boundaries, metrics, and reporting obligations highlight the need for accounting firms to refine their approaches when helping clients navigate compliance with both frameworks.

How to Align Supply Chain Data

To align supply chain data with the GHG Protocol and CSRD requirements, organisations need to map emissions categories and connect them to financial records. The GHG Protocol forms the basis for CSRD and ESRS E1, giving companies experienced in Scope 3 reporting a head start. However, while the GHG Protocol allows flexibility for voluntary reporting, CSRD imposes stricter disclosure rules. Below, we break down how specific Scope 3 categories align with CSRD requirements.

Mapping Scope 3 Categories to CSRD Requirements

CSRD requires companies to dissect Scope 3 emissions into detailed categories rather than reporting a single total. These categories align with the 15 defined in the GHG Protocol Corporate Value Chain (Scope 3) Standard. To begin, firms should identify "hotspots" - categories with the highest emissions or financial spend - to focus their data collection and improve reporting clarity.

For Category 1 (Purchased Goods and Services), when supplier-specific data isn't available, firms can enhance accuracy by combining secondary data with what is available from suppliers. By applying reliable, up-to-date emission factors, financial data can be converted into emissions, ensuring reports are both transparent and verifiable.

Here’s a quick look at how some key Scope 3 categories align with CSRD value chain disclosures:

| GHG Protocol Scope 3 Category | CSRD Value Chain Relevance |

|---|---|

| Category 1: Purchased Goods & Services | Upstream emissions from all goods/services purchased |

| Category 4: Upstream Transportation | Logistics and distribution services paid for by the company |

| Category 6: Business Travel | Transportation of employees for business-related activities |

| Category 11: Use of Sold Products | Emissions from the use of goods and services by the customer |

| Category 12: End-of-Life Treatment | Waste disposal and treatment of products sold by the company |

To ensure comprehensive reporting, firms can use the GHG Protocol's Scope 3 Calculation Guidance decision trees. These help determine the best method - whether spend-based, activity-based, or a hybrid approach - for each category, capturing all relevant upstream and downstream activities.

Using Financial Data for Compliance

Once the category mappings are in place, firms can streamline compliance by integrating financial data. Financial systems offer a solid foundation for aligning GHG Protocol and CSRD requirements. When direct activity data (like litres of fuel or kWh of electricity) isn't available, financial spend data can be used, applying emission factors to convert transactions into CO2e values. This spend-based method is especially useful for managing emissions across complex supply chains. Implementing traceability systems can further enhance this visibility.

Tools like neoeco simplify this process by directly linking financial transactions to recognised emissions categories under frameworks like the GHG Protocol and SECR. With integrations to platforms such as Xero, Sage, and QuickBooks, neoeco removes the need for manual data handling, ensuring that carbon data is accurate and audit-ready.

This integration also automates the calculation of GHG intensity (emissions per net revenue), meeting CSRD requirements. By leveraging financial systems, firms can efficiently generate these metrics while maintaining the transparency and documentation standards CSRD demands. This approach bridges the gap between voluntary GHG Protocol reporting and mandatory CSRD compliance, ensuring firms are equipped to navigate both frameworks effectively.

Implementation Guide for Accounting Firms

For accounting firms juggling both GHG Protocol and CSRD frameworks, a well-structured strategy is essential. The goal is to minimise duplication while ensuring full compliance. Firms with existing Scope 3 reporting experience are better positioned to meet CSRD's tighter timelines and more detailed segmentation requirements. However, the CSRD framework demands even stricter data governance, making a systematic approach non-negotiable. Below is a streamlined five-step process, followed by recommendations for software solutions to simplify compliance efforts.

5-Step Alignment Process

-

Calculate baseline emissions using GHG Protocol best practices.

Start by determining your client's carbon footprint across Scope 1, 2, and 3 emissions.

-

Segment Scope 3 emissions into the 15 distinct categories.

Use the GHG Protocol's Value Chain Standard to break down Scope 3 emissions into its 15 categories. Pay special attention to high-impact areas such as purchased goods and upstream transportation. As the GHG Protocol highlights,

"the Scope 3 Standard is the only internationally accepted method for companies to account for these types of value chain emissions".

-

Gather supplier-specific data and adopt the hybrid method.

When primary data is unavailable, supplement it with secondary industry averages. Apply

appropriate emission factors to financial spend data to fill gaps where supplier-specific information is missing.

-

Report emissions intensity trends.

Automate the calculation of GHG intensity trends by integrating emissions data with financial records.

-

Align inventories to CSRD deadlines.

Since CSRD requires annual reporting with strict deadlines, align your reporting schedule with clients' financial year-ends. Use audit-ready controls to monitor completed, pending, or missing items. For clients in land-use or agriculture, keep in mind that the GHG Protocol's Land Sector and Removals Standard - due in January 2026 - will introduce requirements for tracking land-sector emissions and technological CO₂ removals, such as direct air capture.

Software for Compliance Automation

Once the alignment steps are in place, automation becomes key. Relying on spreadsheets or disconnected systems can lead to compliance risks and inefficiencies. For firms managing multiple clients, software that integrates with financial systems offers a way to automate emissions tracking and ensure audit-readiness.

neoeco is one such platform designed to streamline compliance. It integrates with financial systems like Xero, Sage, and QuickBooks to automate emissions mapping and produce audit-ready reports. By working directly with clients' financial data, neoeco maps transactions to recognised emissions categories under frameworks like the GHG Protocol, ISO 14064, and national standards such as SECR, UK SRS, and ASRS 2. The platform also includes features like a live checklist and a Policy & Evidence Hub for secure documentation storage, ensuring all reporting meets the required standards.

Conclusion

For accounting firms navigating supply chain emissions reporting, aligning GHG Protocol with CSRD data is no longer optional. CSRD's stricter demands for Scope 3 emissions reporting segmentation and audit-ready evidence call for systems that can integrate both frameworks seamlessly, avoiding duplication and inefficiencies.

The solution lies in a unified data approach, with Financially-Integrated Sustainability Management (FiSM) at its core. By embedding carbon data directly into financial ledgers, FiSM removes data silos, cuts down on manual processes, and ensures sustainability reports hold the same level of accuracy as financial statements. For firms working across SECR, UK SRS, or CSRD timelines, this integration transforms compliance into a scalable process.

neoeco plays a pivotal role in this integration by leveraging financial data from platforms like Xero, Sage, and QuickBooks. It automates the mapping of data and generates reports directly from financial transactions, ensuring a streamlined workflow. Tools such as live checklists and the Policy & Evidence Hub ensure all assurance requirements are met without gaps. This automation not only simplifies compliance but also opens doors to new business opportunities.

Compliance isn't just about ticking boxes - it’s a growth driver. Offering services like live sustainability dashboards and ESG advisory enhances recurring revenue streams and boosts client loyalty. With automated updates to frameworks, firms can stay ahead of evolving standards without the burden of constant manual adjustments.

FAQs

What is the difference between the GHG Protocol and CSRD when it comes to Scope 3 emissions?

The GHG Protocol provides in-depth guidance for measuring and accounting for Scope 3 emissions. It highlights the importance of using primary data, which offers a high level of accuracy and specificity but can be resource-intensive to gather. Alongside this, it acknowledges the role of secondary data, which is more accessible but comes with a trade-off in precision.

The CSRD builds upon the GHG Protocol's framework, placing a stronger emphasis on integrating detailed supply chain data. It often mandates businesses to deliver thorough Scope 3 emissions reports, meeting regulatory requirements and boosting transparency for stakeholders. This approach helps organisations stay compliant while responding to the increasing demand for more detailed sustainability reporting.

What are the main challenges in aligning GHG Protocol data with CSRD requirements for UK and EU organisations?

Aligning GHG Protocol data with CSRD requirements can be tricky for organisations in the UK and EU, largely because of differences in scope and reporting criteria. The GHG Protocol provides global guidelines for measuring emissions, while the CSRD introduces more detailed, EU-specific rules. For example, the CSRD requires extensive Scope 3 emissions reporting and integrating supply chain data, which often means reworking data collection and reporting processes to meet both frameworks.

One of the biggest hurdles is ensuring data accuracy and completeness, especially for Scope 3 emissions. These rely heavily on supplier-provided data, and the quality of that data can vary widely. Organisations need to juggle primary data (directly from suppliers) with secondary data (estimates or averages), which adds another layer of complexity. On top of that, differences in how organisational boundaries and thresholds are defined between the two frameworks can make alignment even more challenging.

As regulations continue to evolve, staying compliant becomes a moving target. Systems and processes need regular updates, which can be resource-intensive. Automated tools like neoeco can ease the burden by streamlining data mapping and reporting. These tools help ensure disclosures are accurate, audit-ready, and less reliant on manual effort. Successfully addressing these challenges is critical for compliance and maintaining the trust of stakeholders.

How does neoeco help organisations comply with GHG Protocol and CSRD requirements?

neoeco takes the hassle out of meeting GHG Protocol and CSRD standards by automating crucial parts of carbon reporting and sustainability data management. By connecting directly with financial tools like Xero and QuickBooks, it automatically categorises transactions into recognised emissions categories. This eliminates manual data entry, cutting down on errors and saving valuable time.

The platform ensures your data is accurate, traceable, and ready for audits, aligning seamlessly with frameworks such as GHGP, ISO 14064, and regulations like SECR and UK SRS. Plus, it simplifies the process of including supply chain emissions (Scope 3), which is a must-have for compliance with both GHG Protocol and CSRD. For organisations, this means more efficient and dependable sustainability reporting.