ISO 14064 Data Requirements Explained

ISO 14064 is a global standard for measuring, reporting, and verifying greenhouse gas (GHG) emissions. It helps organisations structure their carbon accounting to align with third-party verifications. The standard is divided into three parts: organisational inventories, project-level activities, and verification requirements. A recent update, ISO/TS 14064-4:2025, adds guidance for applying these rules to organisational inventories.

Key highlights:

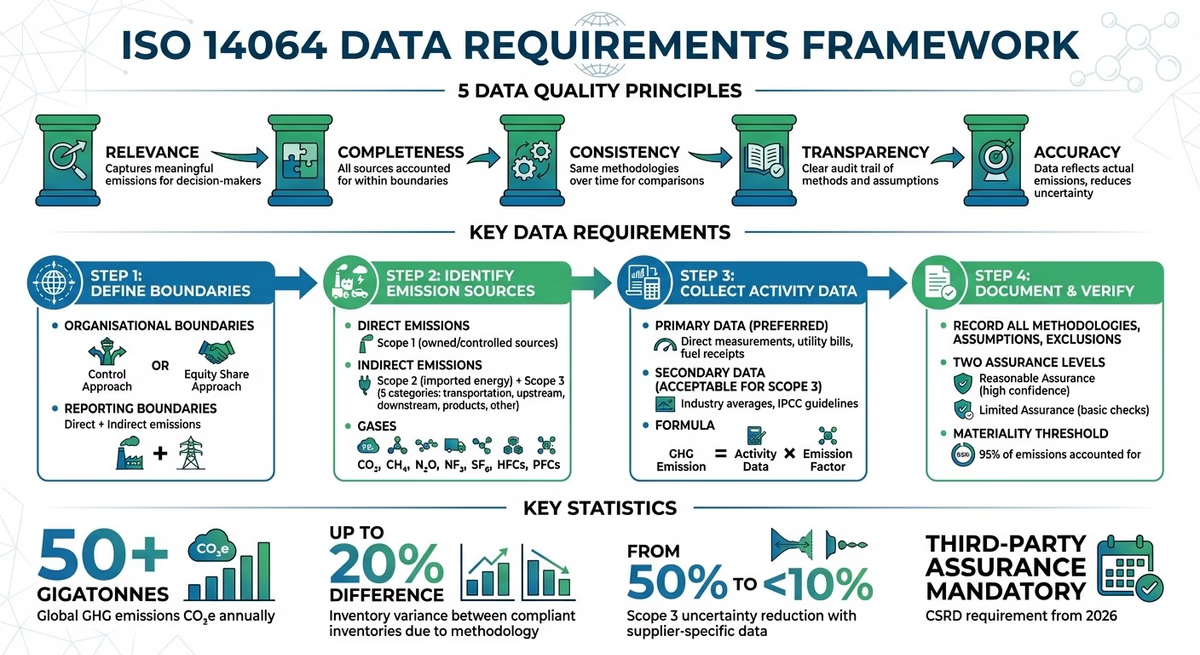

- Data Principles: Five key principles - relevance, completeness, consistency, transparency, and accuracy - ensure reliable GHG data.

- Boundaries: Organisations must define organisational (control or equity share) and reporting boundaries to classify direct and indirect emissions.

- Activity Data: Collect activity-based data (e.g., fuel usage, electricity consumption) and apply emission factors to calculate emissions.

- Primary vs Secondary Data: Primary data (direct measurements) is preferred for Scopes 1 and 2, while secondary data (estimates) is acceptable for Scope 3.

- Verification: ISO 14064-3 requires independent verification with two assurance levels - Reasonable (higher confidence) and Limited (basic checks).

- Documentation: Clear records of methods, boundaries, assumptions, and exclusions are critical for audit readiness.

With GHG emissions exceeding 50 gigatonnes annually, ISO 14064 provides a structured way to ensure emissions reporting is accurate and transparent. Automated tools like neoeco can simplify compliance by integrating carbon data into financial systems, reducing manual errors and supporting audit-ready processes.

ISO 14064 Data Requirements Framework: 5 Key Principles and Implementation Steps

ISO 14064-1:2018 Greenhouse Gas Quantification and Reporting

Data Quality Principles in ISO 14064

ISO 14064-1 lays out five key principles that form the backbone of credible greenhouse gas (GHG) accounting: relevance, completeness, consistency, transparency, and accuracy. These principles help ensure that GHG data is reliable, free from major errors, and avoids selective reporting.

Relevance focuses on making sure your GHG inventory captures emissions that are meaningful to decision-makers, whether they are part of your internal team or external stakeholders like investors. Completeness demands that all emission sources within your defined boundary are accounted for, with clear explanations provided for anything excluded. This principle prevents cherry-picking data to create a misleading picture. Consistency is about sticking to the same methodologies over time, enabling reliable year-on-year comparisons. If you make changes to boundaries or calculation methods, those adjustments must be transparently documented.

Transparency is a cornerstone of this framework. Kara Anderson from Greenly explains:

Implementing ISO 14064 ensures a consistent and reliable approach to emissions reporting. This standard requires organisations to disclose their methodologies, assumptions, and data sources, reducing the risk of greenwashing and making sustainability claims more trustworthy.

Transparency means keeping a clear audit trail, documenting every calculation method, emission factor, and assumption. Finally, accuracy ensures that your data closely reflects actual emissions and reduces uncertainties as much as possible.

These principles collectively set the stage for third-party verification under ISO 14064-3. Without them, organisations risk presenting data that might look precise but lacks credibility. For accounting firms managing client reporting through financially-integrated sustainability management, incorporating these principles into data systems early on can save time and money during verification.

Organisations with strong documentation and transparent justifications for exclusions tend to navigate verification more smoothly. On the other hand, incomplete or poorly managed records often lead to delays and added costs. By embedding these principles into your data workflows from the start, you can avoid the hassle of reworking data during the verification process.

These foundational principles naturally lead into more detailed methods for identifying GHG sources and setting boundaries.

Data Requirements for GHG Source Identification and Boundaries

Before diving into quantification, it’s crucial to clearly define your emission sources and boundaries. According to ISO 14064-1, organisations need to establish two types of boundaries: organisational boundaries (which facilities or operations are included) and reporting boundaries (which emission sources within those operations will be measured). These boundaries form the backbone of reliable GHG data, ensuring adherence to the data quality principles previously outlined. They also set the stage for distinguishing between direct and indirect emissions in later steps.

For organisational boundaries, you’ll need to decide between two consolidation approaches. The Control Approach includes 100% of emissions from facilities under your direct control, while the Equity Share Approach accounts for emissions based on your economic stake in each facility. Both methods are valid, but the choice you make will determine how emissions appear in your inventory.

After setting organisational boundaries, you can move on to defining reporting boundaries by identifying both direct and indirect emission sources. Direct emissions come from sources your organisation owns or controls - like company vehicles, on-site boilers, or chemical processes. Indirect emissions, on the other hand, stem from imported energy sources such as purchased electricity, steam, heating, or cooling. The 2018 update to ISO 14064-1 broadened the scope of indirect emissions, dividing them into four additional categories: transportation, upstream supply chain activities, downstream product impacts, and other sources.

Direct and Indirect Emissions Sources

Once your boundaries are in place, ISO 14064-1 requires separate quantification of direct emissions for each greenhouse gas, including CO₂, CH₄, N₂O, NF₃, SF₆, and specific groups of HFCs and PFCs. These emissions typically arise from activities like fuel combustion in owned equipment, leaks from refrigeration systems, or emissions from manufacturing processes.

Indirect emissions, meanwhile, occur at sources controlled by other organisations but are a result of your operations. ISO 14064-1 identifies five categories to help integrate organisational accounting with a broader life cycle emissions perspective. To ensure transparency, you’ll need to establish criteria for determining which indirect emissions are significant enough to include. This prevents selective reporting that could favour less impactful categories while ignoring more critical ones.

Setting Operational Boundaries

Operational boundaries focus on which emission sources within your organisational boundary will be measured. ISO 14064-1 doesn’t enforce universal thresholds for significance; instead, it allows organisations to set their own criteria. However, these criteria must be well-documented and any exclusions must be clearly justified.

For example, if your organisation chooses to omit certain indirect sources - such as business travel below a specific threshold - you’ll need to provide a detailed rationale that can stand up to verification. Accounting firms, for instance, can simplify emission source identification by linking GHG data with financial transactions, streamlining the process.

Thorough documentation of your boundaries is essential to avoid data gaps. Start with direct emissions, as they are generally more straightforward, before tackling the complexities of indirect sources. By defining boundaries clearly from the outset, you lay the groundwork for a dependable life cycle emissions analysis under ISO 14064.

Activity Data Collection and Emission Factors

Once boundaries are set, the next step is to gather activity data - the measurable quantities of activities that generate or remove greenhouse gases. This includes things like fuel usage (in litres), electricity consumption (in kWh), waste production (in kilograms), and travel distances (in kilometres). This data forms the basis of the greenhouse gas (GHG) calculation formula:

GHG Emission/Removal = Activity Data × Emission Factor.

Under ISO 14064-1, collecting accurate activity data is key to ensuring transparency and traceability. It allows organisations to categorise emissions into direct (Scope 1), energy indirect (Scope 2), and value chain indirect (Scope 3) sources. High-quality data is indispensable for ISO 14064-3 verification. Interestingly, two GHG inventories for the same organisation - both compliant with standards - can differ by up to 20%, simply because of the methods used. This highlights the importance of choosing between primary and secondary data.

Primary vs Secondary Data

ISO 14064-1 differentiates between primary data, which is directly measured, and secondary data, which is based on estimates or averages. Primary data comes from sources like utility bills, fuel receipts, metre readings, or production logs - information directly tied to specific activities in the value chain. Secondary data, on the other hand, relies on external sources like the IPCC guidelines, FAOSTAT, or national benchmarks, often used when direct measurements aren’t available.

For Scope 1 and Scope 2 emissions, primary data is essential to meet "Reasonable Assurance" during verification. Secondary data is generally acceptable for Scope 3 emissions or less critical sources, as long as the assumptions and databases used are clearly documented. For example, working with suppliers to obtain specific data can reduce uncertainty in Scope 3 emissions from 50% to under 10%. However, many organisations still rely on spreadsheets, which can lead to errors and inconsistencies. Using high-quality data ensures consistency across the inventory, aligning with previously defined data quality principles.

| Feature | Primary Data | Secondary Data |

|---|---|---|

| Source | Directly measured (e.g., invoices) | Estimated (e.g., industry averages) |

| Accuracy | High; specific to the organisation | Lower; higher uncertainty |

| ISO 14064 Preference | Preferred for all categories | Acceptable when primary data isn’t available |

| Typical Use Case | Scope 1 and Scope 2 emissions | Scope 3 (value chain) emissions |

| Compliance Requirement | Requires traceability to source | Requires disclosure of assumptions/databases |

Once you’ve gathered the activity data, the next step is to apply emission factors to convert these figures into GHG emissions.

Choosing and Applying Emission Factors

Converting activity data into emissions accurately is crucial for understanding the life cycle impact of activities. Emission factors are standardised values used to translate activity data into greenhouse gas emissions, usually expressed in CO₂ equivalent (CO₂e). For instance, Scope 2 emissions are calculated by multiplying electricity usage by the appropriate regional emission factors. ISO 14064-1 mandates the use of recognised methodologies and emission factors to ensure consistent, transparent, and accurate reporting.

When selecting emission factors, it’s best to use trusted international or national databases, such as the IPCC Guidelines, the GHG Protocol, or regional sources like ADEME. Make sure the emission factors are "time-matched", meaning they correspond to the same reporting period as your activity data. Activity-based data, such as litres of fuel or kWh of electricity, is generally more precise than spend-based data, as it better reflects operational realities and efficiency improvements. To stay audit-ready under ISO 14064-3, maintain a clear record linking each emission factor to its source. This level of detail is especially important for organisations handling complex Scope 3 emissions.

Quantification, Uncertainty, and Documentation

Quantification Methods

Under ISO 14064-1, organisations must calculate emissions from two main sources: direct emissions from owned or controlled sources and indirect emissions from imported energy and value chain activities, keeping them separate. Direct emissions are broken down by specific gases, such as CO₂, CH₄, N₂O, NF₃, SF₆, and grouped categories like HFCs and PFCs, ensuring clarity in reporting. The 2019 update to the standard further categorised indirect emissions into five distinct groups: imported energy, transportation, products used by the organisation, products used by others, and other sources.

For project-level reporting under ISO 14064-2, emissions are calculated by identifying all relevant Sources, Sinks, and Reservoirs (SSRs), then comparing these against a conservative baseline scenario. Organisations must also select a consolidation method - either the control approach or the equity share approach. This choice directly affects the reported emissions volume and the level of uncertainty in the data. These quantification practices lay the groundwork for managing uncertainty effectively in greenhouse gas (GHG) inventories.

Managing Uncertainty in GHG Data

Addressing uncertainty is a key requirement for ISO 14064 compliance. Organisations need to assess and report uncertainty levels to ensure transparency in their GHG inventories. Verification under ISO 14064-3 evaluates whether reported emissions fall within an acceptable uncertainty range, as defined by the organisation or regulators. Decerna highlights the importance of this with the following:

Information is material if its omission or misstatement could influence intended users' decisions.

This makes it essential to define clear criteria for indirect emissions, ensuring that exclusions are justified and not selectively applied to present favourable data.

Adopting robust data management systems early can help reduce uncertainty and minimise the risk of material misstatements. For organisations undergoing verification, starting with Reasonable Assurance is recommended to build confidence in data systems before transitioning to Limited Assurance in subsequent years. Decerna explains the difference between these levels:

Reasonable assurance provides high confidence in the GHG statement through extensive evidence-gathering, with conclusions expressed in positive form: 'the GHG statement fairly represents actual emissions'.

Meanwhile:

Limited assurance provides reduced confidence, with the verifier concluding in negative form: 'nothing has come to our attention to suggest the GHG statement is materially misstated'.

By conducting thorough uncertainty assessments, organisations can not only strengthen their verification process but also improve their overall record-keeping practices.

Documentation and Record-Keeping

Comprehensive documentation is essential for ISO 14064 compliance and successful verification. Organisations must record their chosen consolidation approach and ensure it is applied consistently. Additionally, they need to document all identified greenhouse gas SSRs, along with the methodologies used for quantification, such as emission factors and global warming potential (GWP) values. For indirect emissions, it’s important to document the criteria used to determine significance and provide transparent explanations for any exclusions.

According to Carbon Accounting UK:

Proactive preparation - particularly around data collection and documentation - makes the certification process smoother.

Maintaining a detailed audit trail is crucial. This includes everything from source data, such as utility bills and fuel receipts, to the final GHG assertions, ensuring a seamless verification process. Documentation should also cover uncertainty assessments and materiality thresholds, which define the level of misstatement that could influence decision-making. For organisations dealing with complex value chain emissions, aligning ISO 14064 documentation with frameworks like ISSB reporting can help streamline processes and maintain consistency across reporting standards.

Verification and Audit-Ready Data under ISO 14064-3

ISO 14064-3 takes the groundwork of solid documentation and uncertainty management a step further by focusing on independently verifying that greenhouse gas (GHG) data is ready for audit. This standard ensures that reported emissions are not only accurate but also meet specific criteria for reliability. It provides a structure for the independent verification of GHG statements, covering both verification (evaluating historical data) and validation (reviewing future projections). However, most organisations primarily focus on verification when it comes to their GHG inventories.

Verification bodies play a critical role here, but they must maintain independence and impartiality from the organisations they assess. To achieve this, they are required to have management systems in place to handle appeals and complaints. Additionally, verification teams must comply with ISO 14065 standards for impartiality and ISO 14066 standards for technical expertise. The process itself is broken down into four clear phases: analysing the organisation strategically, conducting a risk assessment to identify potential material misstatements, gathering evidence to address these risks, and forming a final conclusion.

Organisations have two assurance levels to choose from. Reasonable Assurance provides a high level of confidence, confirming that the GHG statement is accurate, while Limited Assurance involves fewer checks and focuses on confirming the absence of material misstatements. For organisations just starting to establish their reporting systems, opting for Reasonable Assurance can help build a strong baseline of data quality. Once this foundation is in place, they may transition to Limited Assurance for interim reporting periods. This approach requires meticulous documentation to ensure audit readiness.

Proper documentation is key. Organisations need to maintain transparent records, including data sources, calculation methods, assumptions, and any identified limitations. For verification purposes, it’s essential to have an assumptions register and audit logs that trace every raw input - such as utility bills or fuel receipts - through to its CO₂e conversion.

The materiality principle is at the heart of the verification process. As Decerna highlights:

Information is material if its omission or misstatement could influence intended users' decisions.

Verifiers set materiality thresholds based on the scale and purpose of the GHG statement, typically requiring that at least 95% of emissions within the defined scope are accounted for. These thresholds are crucial for ensuring the integrity of life cycle emission analyses.

For organisations dealing with complex value chain emissions, aligning their documentation practices with frameworks like ISSB reporting can simplify the verification process. This alignment not only ensures consistency across various reporting standards but also integrates seamlessly with life cycle emission analysis, making it easier to meet the demands of thorough verification.

Integrating ISO 14064 Data with Life Cycle Emission Analysis

ISO 14064 data plays a crucial role in life cycle emission analysis (LCA), especially for organisations aiming to track cradle-to-gate emissions within their supply chains. The 2018 update to ISO 14064-1 introduced an expanded framework for indirect emissions, now encompassing five categories that better align organisational inventories with product-level carbon footprints by addressing both upstream and downstream impacts. This alignment bridges gaps between organisational and product-focused carbon accounting, paving the way for a deeper understanding of specific ISO 14064 emission categories.

For instance, Category 4 focuses on indirect emissions associated with products used by an organisation, covering everything from raw material extraction to delivery. When paired with ISO 14067 data, it offers a comprehensive view of supply chain emissions. The critical difference between these standards lies in how they define boundaries: ISO 14064-1 uses legal or financial control, while ISO 14067 employs a physical cause-and-effect approach across supply chains.

Adding to this, ISO/TS 14064-4:2025, introduced in November 2025, provides detailed guidance on setting reporting boundaries for indirect emissions. This helps organisations justify exclusions and maintain transparency in their Scope 3 disclosures. For companies managing complex value chain emissions, this technical specification clarifies which indirect emissions are significant enough to measure. Decerna highlights this effort, stating:

The indirect emission categories in ISO 14064-1 attempt to bridge this gap by encouraging upstream and downstream accounting.

For accounting firms assisting clients with Scope 3 reporting, the ISO 14064-3 verification framework offers a unified method applicable to both organisational inventories and product carbon footprints. This ensures independent assurance of lifecycle data accuracy. By adopting this framework, organisations can streamline Scope 3 reporting and enhance the credibility of their lifecycle emissions analysis. Establishing clear significance criteria early on also prevents selective reporting of favourable data, ensuring that all material emissions are accounted for.

neoeco: Managing ISO 14064 Data Requirements

neoeco simplifies ISO 14064 data management by eliminating the need for manual processes like spreadsheets. For accounting firms handling ISO 14064-compliant data, the real hurdle lies in gathering detailed, reliable activity data. neoeco addresses this challenge by embedding sustainability accounting directly into financial ledgers, streamlining the entire process.

At the heart of the platform is the FiS Ledger, which incorporates over 90 ESG impact factors into financial transactions. This allows firms to monitor emissions in real time. Automated transaction mapping connects ledger entries to recognised emission factors under the GHGP and ISO 14064. This ensures precise identification of both direct and indirect emissions across Scope 1, 2, and 3. By automating these processes, neoeco supports the "audit-ready" standards of ISO 14064-3, offering verifiable controls over the entire data pipeline.

Unlike generalised spend-based estimates, which often inflate emissions figures at the category level, neoeco delivers detailed insights down to specific processes and materials. This ensures data accuracy, which is crucial for third-party verification. By integrating carbon data with financial ledgers, neoeco helps firms align with ISO 14064 requirements. With the Corporate Sustainability Reporting Directive (CSRD) set to require third-party assurance of greenhouse gas data from 2026, neoeco allows firms to structure their reporting to meet ISO 14064-3 standards, ensuring they are prepared for regulatory and investor scrutiny.

The platform also includes compliance-ready templates that follow ISO 14064-1 principles, promoting transparency, consistency, and accuracy. Additionally, the Policy & Evidence Hub securely stores supporting documentation for audit purposes. For firms navigating ISSB reporting or tackling complex Scope 3 emissions, neoeco’s automation ensures traceability and accountability across all quantification methods and data sources required for ISO 14064-3 verification.

Seamless integration with tools like Xero, Sage, and QuickBooks means firms can deliver ISO 14064-compliant carbon accounts effortlessly. The result? Finance-grade carbon data that's accurate, traceable, and ready for verification.

Conclusion

ISO 14064 offers a globally recognised framework for organisations to measure, report, and verify their greenhouse gas (GHG) emissions with consistency and reliability. It requires organisations to define boundaries, classify emissions across Scopes 1–3, use standardised quantification methods, and document all assumptions clearly. With over 50 gigatonnes of CO₂e emitted annually worldwide, the stakes are immense, and scrutiny from investors, regulators, and independent verifiers is sharper than ever.

This framework highlights the critical need for accurate data management. Even small methodological decisions can significantly influence reported emissions, which is why ISO 14064-3 verification ensures transparency and evidence-based reporting. New regulations like the CSRD and SEC climate disclosure rules now require third-party assurance of GHG data, making it essential for businesses to adopt audit-ready systems, especially when preparing for ISSB reporting or addressing complex Scope 3 emissions. These requirements align closely with ISO 14064 standards.

The intricate task of managing countless methodological choices is driving the adoption of advanced data management systems. For UK accounting firms, digital solutions are becoming indispensable. Gathering detailed, reliable activity data is no small feat, and manual spreadsheets often fall short. Platforms like neoeco simplify this by integrating sustainability accounting into financial systems, automating the mapping of transactions to recognised emission factors, and ensuring audit-ready documentation from the outset.

Whether your goal is mandatory verification or voluntary disclosure, the steps are the same: define clear boundaries, implement reliable systems, and maintain transparent records. Tackling these challenges with the right tools transforms ISO 14064 compliance from a mere obligation into a strategic opportunity.

FAQs

What data is needed first to begin ISO 14064 reporting?

To kick off ISO 14064 reporting, the first step is to compile data on your organisation’s greenhouse gas emissions. Begin by building an inventory that accounts for both direct and indirect emissions. This involves three key actions:

- Collecting activity data: Gather detailed records of activities that contribute to emissions, such as energy usage or transportation.

- Applying relevant emission factors: Use standardised factors to convert activity data into measurable emissions.

- Defining organisational boundaries: Clearly establish which parts of your organisation and operations are included in the report.

By following these steps, you’ll align with the ISO 14064 framework and ensure your reporting is accurate and thorough.

How do we set boundaries for subsidiaries and joint ventures?

Defining boundaries under ISO 14064 means establishing clear organisational and reporting limits for greenhouse gas (GHG) emissions. Organisations can choose between two approaches: the control approach (based on financial or operational control) or the equity share approach (reflecting ownership stakes). This ensures that both direct and indirect emissions are accounted for, making audits and verification more reliable. Setting clear boundaries is crucial for transparent and credible emissions reporting, particularly for subsidiaries and joint ventures, while staying aligned with ISO standards.

What evidence do verifiers usually request under ISO 14064-3?

Verifiers working under ISO 14064-3 often require sufficient and appropriate evidence to back up greenhouse gas assertions. This evidence usually consists of documentation, records, and data that prove the accuracy and completeness of the reported emissions. Additionally, they look for evidence of the verification activities carried out. These materials are crucial for ensuring the organisation meets the standard's requirements.