LCA Scenario Analysis for Carbon Reporting

LCA scenario analysis helps organisations assess the carbon impact of different future possibilities, allowing them to plan better for net-zero goals and meet carbon reporting standards like ISO 14064 and SECR. This includes specific applications like ISO 14064 for transport emissions to ensure audit-ready reporting. Instead of just reviewing past emissions, it models "what if" scenarios to predict outcomes, prevent trade-offs, and ensure credible reporting.

Key takeaways:

- Scenario Analysis: Compares different future options using Life Cycle Assessment (LCA) methods.

- ISO Standards: Aligns with ISO 14064-1 and the updated ISO/TS 14064-4:2025 for accurate emissions reporting.

- Scope 1, 2, 3 Mapping: Helps map emissions across direct, energy-related, and supply chain impacts.

- Data Quality: Emphasises high-quality, transparent data for reliable results.

- Automation Tools: Platforms like neoeco simplify reporting by linking financial data to emissions categories.

This approach ensures compliance, transparency, and actionable insights for organisations navigating complex carbon reporting demands.

Life Cycle Assessment and Decarbonization: What is LCA Good At?

LCA is particularly effective at supporting Scope 3 emissions reporting by providing the granular data needed for complex value chain assessments.

Core Components of LCA Scenario Analysis

Effective LCA scenario analysis depends on three key elements: well-defined goals and scope, meaningful comparative scenarios, and high-quality data. These ensure accurate carbon reporting in line with ISO 14064 and SECR standards.

Setting Goals and Scope

Start by clearly defining the purpose of the measurement, its intended application, and the target audience. Without clarity here, you risk missing key reporting obligations.

Another essential step is determining the functional unit. This unit of measurement - like "1 litre of product protected for 6 months" - anchors all impact calculations to a consistent reference point. When comparing scenarios, each option must relate back to this functional unit to ensure fairness and consistency.

Organisational boundaries are another critical aspect. ISO 14064-4:2025 outlines two approaches for defining emission responsibilities: the control approach or the equity share approach. Transparency in these boundaries and the methods used for quantification is a core requirement of the standard.

Setting data quality requirements early on is also vital. This includes establishing standards for data collection and validation, as well as deciding whether to use primary vs secondary data (directly from your operations or industry averages). Increasingly, organisations are prioritising primary data to better highlight their decarbonisation efforts.

Once the scope is defined, you can begin crafting scenarios that compare a "business as usual" approach with potential intervention outcomes.

Creating and Comparing Scenarios

ISO 14064-2 mandates the use of a conservative baseline scenario for comparisons.

For energy-related scenarios, comparisons often involve two methods: location-based (using average grid emissions) and market-based (using contractual instruments like Renewable Energy Certificates). In cases where physical traceability is impractical, Chain of Custody models defined by ISO 22095 - such as Mass Balance and Book and Claim - allow for the separation of physical and accounted products. These models are particularly useful for tracking renewable or recycled content in complex supply chains.

All scenarios must align with the same functional unit and follow the ISO 14040/14044 iterative four-phase methodology. This ensures consistency and accuracy across the analysis.

The reliability of your scenarios hinges on the quality of your data and the rigour of your controls.

Data Collection and Quality Control

High-quality data is the backbone of robust scenario analysis. ISO 14044 requires clear documentation of all data sources, assumptions, and limitations. When primary data isn't available, it's acceptable to use proxies or make reasonable assumptions, but these must be explicitly documented. Refining boundaries and iterating results over time helps improve accuracy.

This process is critical for meeting the transparency standards set by ISO 14064-4:2025. Forward-looking climate metrics require data that is both defensible and robust. For organisations reporting under SECR or UK SRS frameworks, third-party verification under ISO 14064-3 provides additional assurance that greenhouse gas statements are accurate and meet specified criteria.

Aligning LCA Scenarios with Carbon Reporting Frameworks

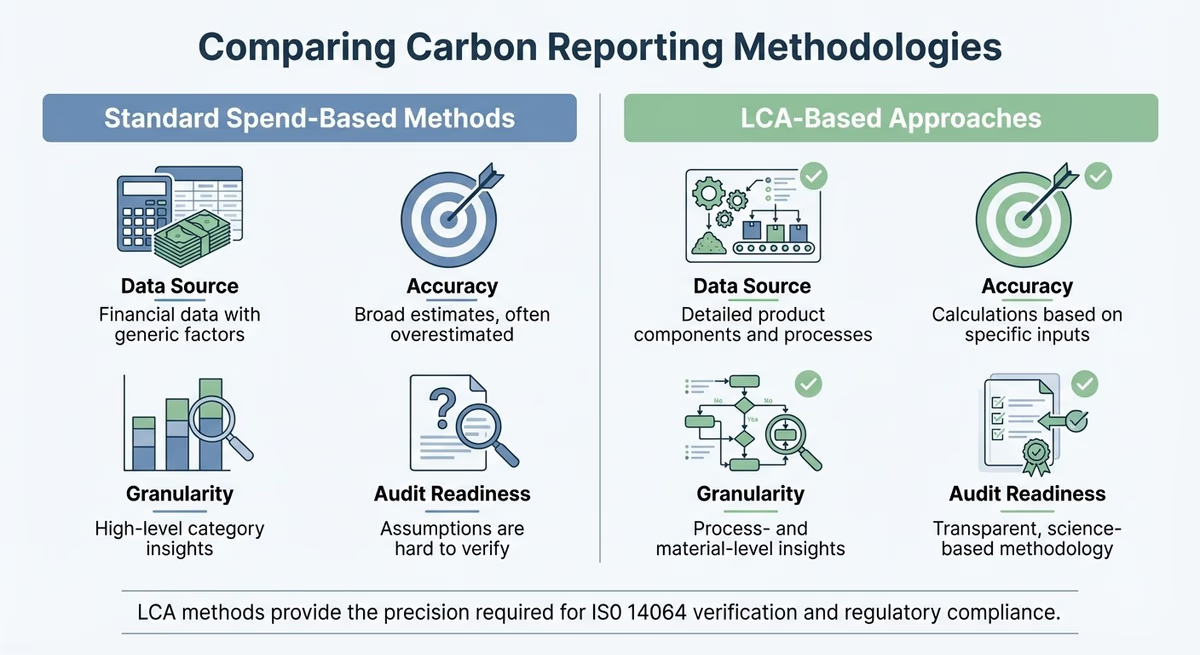

LCA-Based vs Spend-Based Carbon Reporting Methods Comparison

Translating Scenarios to Scope 1, 2, and 3 Emissions

Once boundaries are established, the next step is to map Life Cycle Assessment (LCA) stages to Scope 1, 2, and 3 emissions.

- Scope 1: These are direct emissions from sources owned or controlled by the organisation. Examples include emissions from boilers, company vehicles, and other on-site assets.

- Scope 2: This category includes indirect emissions from purchased energy, such as electricity, steam, heating, or cooling.

- Scope 3: These emissions cover the broader value chain, both upstream and downstream. This includes impacts from purchased goods, capital equipment, transportation, and even the end-of-life treatment of products.

The 2019 update to ISO 14064-1 broadened the scope of indirect emissions to incorporate additional categories like transportation and products used by the organisation. LCA methods are particularly effective here, as they meticulously trace impacts across the supply chain, offering a level of precision that spend-based methods - relying on financial data and generic emission factors - simply cannot match.

| Aspect | Standard Spend-Based Methods | LCA-Based Approaches |

|---|---|---|

| Data Source | Financial data with generic factors | Detailed product components and processes |

| Accuracy | Broad estimates, often overestimated | Calculations based on specific inputs |

| Granularity | High-level category insights | Process- and material-level insights |

| Audit Readiness | Assumptions are hard to verify | Transparent, science-based methodology |

This level of detail is crucial for meeting today’s verification and regulatory standards. By mapping LCA data to these scopes, organisations can ensure compliance while gaining deeper insights into their carbon footprint.

Meeting ISO 14064, SECR, and UK SRS Requirements

ISO 14064-3 outlines the process for independently verifying greenhouse gas (GHG) statements. LCA-based reporting complements this by ensuring transparency, with clearly documented assumptions and rigorous, science-backed calculations. The recently published ISO/TS 14064-4:2025 further highlights the importance of transparency, particularly in quantification and managing uncertainty.

For UK companies reporting under SECR or UK SRS frameworks, this level of precision is non-negotiable. Audit-ready reporting not only meets regulatory requirements but also aligns with client expectations. This approach is consistent with ISSB reporting, ensuring robust compliance and readiness for verification.

How neoeco Automates Carbon Reporting

neoeco streamlines carbon reporting by directly linking financial transactions to established emissions categories under frameworks like GHGP, ISO 14064, SECR, and UK SRS. Say goodbye to tedious spreadsheets and manual conversions - neoeco provides accurate, finance-grade carbon data with ease.

The platform generates audit-ready reports, complete with built-in controls. Auditors can securely access supporting evidence directly through the system, eliminating the need for endless email exchanges. For organisations tackling Scope 3 emissions across complex supply chains, neoeco ensures the transparency and traceability required for ISO 14064-3 verification.

LCA Scenario Analysis in Practice

Let’s dive into how Life Cycle Assessment (LCA) principles are applied in real-world scenarios.

Alternative Fuel Life Cycle Scenarios

When evaluating alternative fuels, it’s essential to compare a project scenario against a baseline scenario while identifying all relevant SSRs (controlled, related, and affected sources). This ensures a thorough assessment of the project’s impact.

Leakage, such as land-use changes or displaced fossil fuel production, must be accounted for to avoid overstating emission reductions. LCA examines every stage - from extraction to end-of-life - ensuring that environmental burdens aren’t simply shifted from one phase to another. Consistency is key: all comparisons should use the same functional unit defined at the start.

Building Energy Efficiency Scenarios

In energy efficiency projects, organisations must establish a credible baseline that reflects emissions without the project. Demonstrating additionality is crucial - projects need to show they achieve more than what would have occurred under normal circumstances.

From 2019 to 2023, Nottinghamshire County Council implemented a Carbon Reduction Plan targeting energy efficiency in buildings and highways. Key initiatives included converting street lighting to LED and investing in building upgrades. These efforts led to a 39% total reduction in greenhouse gas (GHG) emissions. Notable reductions included:

- Heating fuels in buildings: A 30% drop, from 2,970 to 2,087 tCO2e.

- Electricity in buildings: A 41% decrease, from 2,336 to 1,387 tCO2e.

- Electricity for highways assets: A 49% reduction, from 6,750 to 3,476 tCO2e.

These results highlight the measurable benefits of energy efficiency improvements and set the groundwork for analysing biomass and carbon removal projects.

Biomass and Carbon Removal Scenarios

Biomass projects, such as reforestation or biomass energy, provide another opportunity to apply LCA principles. These scenarios compare emissions from the project against a baseline that represents what would have occurred without it. Net CO2e reductions are calculated by subtracting project emissions from baseline emissions, while factoring in any increases in affected SSRs (leakage).

Recent updates to ISO 14044 have refined how biogenic carbon, land-use changes, and carbon storage are quantified. For carbon removal scenarios, it’s vital to ensure that reductions exceed the baseline to avoid creating "phantom" carbon credits. Including affected SSRs is equally important to account for indirect impacts, such as displaced fossil fuel production or land-use changes. Projects aiming for carbon credit certification under ISO 14064-2 typically require third-party verification to confirm the accuracy and legitimacy of claimed removals.

Common Challenges and Practical Solutions

Organisations often encounter real-world obstacles that can disrupt even the most well-planned Life Cycle Assessment (LCA) analyses. Let’s look at some of the key challenges and actionable ways to address them.

Ensuring Data Quality and Consistency

When data quality falters, LCA scenario analysis becomes unreliable. On average, poor data quality costs organisations around £10 million annually, with data engineers spending up to 40% of their time fixing data issues. Common problems include:

- Typos and unit conversion mistakes (e.g., cubic metres to litres)

- Mixing outdated datasets or incompatible database versions (like Ecoinvent 3.4 with 3.8)

- Methodological inconsistencies

- Geographic mismatches, such as applying a European electricity mix to a Southeast Asian facility

As Monte Carlo explains, "Data quality issues arise any time data is missing, broken, or otherwise erroneous based on the normal function of a given pipeline".

To combat this, organisations can carry out hotspot analyses to catch anomalies early. Replacing generic datasets with Environmental Product Declarations (EPDs) from suppliers and performing sensitivity analyses can also highlight how uncertain assumptions impact the final results.

Maintaining Consistent Boundaries and Metrics

LCA comparability relies heavily on consistent methodologies. For instance, ISO 14064-1 requires organisations to define boundaries using either:

- The control approach, which includes 100% of emissions from facilities under financial or operational control.

- The equity share approach, which allocates emissions based on economic interest.

Transparent, standardised criteria for including indirect emissions are crucial. A central repository for key elements like GHG Protocol calculation methods, emission factors, and assumptions helps ensure consistency across departments and reporting periods.

Additionally, assigning clear data ownership roles can streamline operations. For example, facilities teams can manage energy data, while logistics teams handle fuel data. For UK organisations adapting to ISSB reporting requirements, such structured methods are essential for compliance.

As Decerna puts it, "Comparability requires consistent methodology".

Using Automation Tools like neoeco

Automation offers a practical way to navigate these challenges. Manual spreadsheets often introduce errors and make scenario comparisons cumbersome. Automation platforms, however, enable organisations to perform "what-if" analyses, pinpoint carbon hotspots, and model effective reduction strategies - all before committing resources.

neoeco is one such platform designed to simplify these processes. It integrates directly with clients' financial ledgers, mapping transactions to recognised emissions categories under frameworks like GHGP, ISO 14064, SECR, and UK SRS. This reduces manual errors and ensures audit-ready documentation, which is vital for third-party verifications under ISO 14064-3.

neoeco has received glowing reviews, including a 5.0 out of 5 stars rating on the Xero App Store. One user, Stephen Pell, shared his experience:

"End to end reporting solution built for accountants. Seamlessly integrates with Xero!".

Conclusion

LCA scenario analysis transforms carbon reporting into a precise, audit-ready process. By moving away from spend-based emission methods and adopting primary, process-based data, organisations can meet the detailed requirements of ISO 14064-1 and SECR while gaining deeper insights into their emissions hotspots. The 2019 revision of ISO 14064-1 expanded the framework for indirect emissions, adding five new categories that include transportation, products used by the organisation, and products used by others. This makes LCA's scientific approach essential for accurately measuring these complex Scope 3 emissions flows. The upcoming publication of ISO 14064-4 in November 2025 further underscores the importance of standardised methods for emissions quantification.

The trend towards using primary data is gaining momentum. Industry-led initiatives like Catena-X and Together for Sustainability (TfS) are encouraging organisations to share product carbon footprint (PCF) data, moving away from reliance on secondary industry averages. This shift highlights the role of automation in ensuring consistent and verifiable reporting.

For accounting firms, the increasing complexity of carbon reporting presents both challenges and opportunities. Automation platforms like neoeco help bridge the gap by mapping financial transactions to recognised emissions categories, producing audit-ready data. This approach simplifies independent verification under ISO 14064-3, whether firms are aiming for reasonable or limited assurance.

As ISO 14040 explains, "LCA is conducted by defining product systems as models that describe the key elements of physical systems". This principle - modelling real-world operations into clear and comparable data - is what makes LCA scenario analysis so effective. When paired with automation, it enables organisations to deliver Scope 3 emissions reports that are both compliant and actionable.

LCA scenario analysis equips organisations with the clarity to make informed decisions, monitor progress, and build trust in a world where transparency is increasingly critical.

FAQs

What is the role of LCA scenario analysis in improving carbon reporting?

Life Cycle Assessment (LCA) scenario analysis provides a thorough, science-based way to assess emissions throughout a product's entire lifecycle. This method is especially useful for navigating the complexities of supply chains and tackling Scope 3 emissions, which are notoriously difficult to measure with precision.

By modelling different scenarios, LCA pinpoints uncertainties and fine-tunes emission calculations. It ensures alignment with global frameworks like the GHG Protocol, ISO 14064, and UK-specific standards such as SECR. The outcome? More dependable, audit-ready carbon data that bolsters compliance efforts and supports sustainability objectives.

What is the difference between Scope 1, Scope 2, and Scope 3 emissions?

Scope 1 emissions refer to direct greenhouse gas emissions that come from sources your organisation directly owns or controls. This can include things like fuel burned in company vehicles or boilers. On the other hand, Scope 2 emissions cover indirect emissions linked to the production of electricity, heat, or steam that your organisation purchases and uses. Lastly, Scope 3 emissions encompass all other indirect emissions throughout your value chain. This might involve emissions from your suppliers, the use of your products, or even waste disposal.

Grasping these categories is crucial for accurate carbon reporting under standards like ISO 14064 and SECR. They provide a thorough understanding of your organisation’s overall impact on the environment.

How does neoeco streamline carbon reporting for businesses?

Neoeco makes carbon reporting straightforward by automatically linking financial transactions to recognised emissions categories. It aligns with established frameworks like the GHGP, ISO 14064, and national regulations such as SECR. This approach removes the hassle of using spreadsheets or manually converting data, ensuring precise, audit-ready carbon data that meets finance-grade standards.

With direct integration into clients' financial systems, Neoeco offers an efficient and professional solution tailored for sustainability reporting. This allows accounting firms to confidently provide accurate and reliable carbon accounting services.