Employee Engagement vs Workforce Sustainability Reporting

Employee engagement and workforce sustainability reporting are two distinct ways businesses evaluate their workforce. Engagement reporting focuses on internal metrics like morale, retention, and productivity to improve workplace dynamics. Sustainability reporting, on the other hand, aligns with ESG standards and caters to external stakeholders like investors and regulators using ESG benchmarking tools for CFOs by assessing policies on diversity, fair wages, and health and safety.

Key Differences:

- Audience: Engagement reporting is for internal use (HR, management), while sustainability reporting targets external stakeholders (investors, regulators).

- Metrics: Engagement uses surveys and sentiment analysis, while sustainability relies on objective, audit-ready data like pay gaps and safety records.

- Purpose: Engagement improves internal processes; sustainability demonstrates accountability and compliance.

Quick Comparison:

| Aspect | Employee Engagement Reporting | Workforce Sustainability Reporting |

|---|---|---|

| Focus | Motivation, retention, productivity | ESG risks, long-term workforce value |

| Audience | Internal (HR, management) | External (investors, regulators) |

| Metrics | Surveys, morale, turnover intent | Diversity, pay gaps, health & safety |

| Data Type | Subjective, qualitative | Objective, auditable |

| Goal | Improve workplace dynamics | Meet compliance, build external trust |

Both approaches can overlap, sharing metrics like diversity and well-being, and integrating them can streamline data management while addressing both internal and external needs.

Employee Engagement vs Workforce Sustainability Reporting: Key Differences

Aligning Employee Engagement & ESG How to build a resilient workforce for sustainability

What is Employee Engagement Reporting?

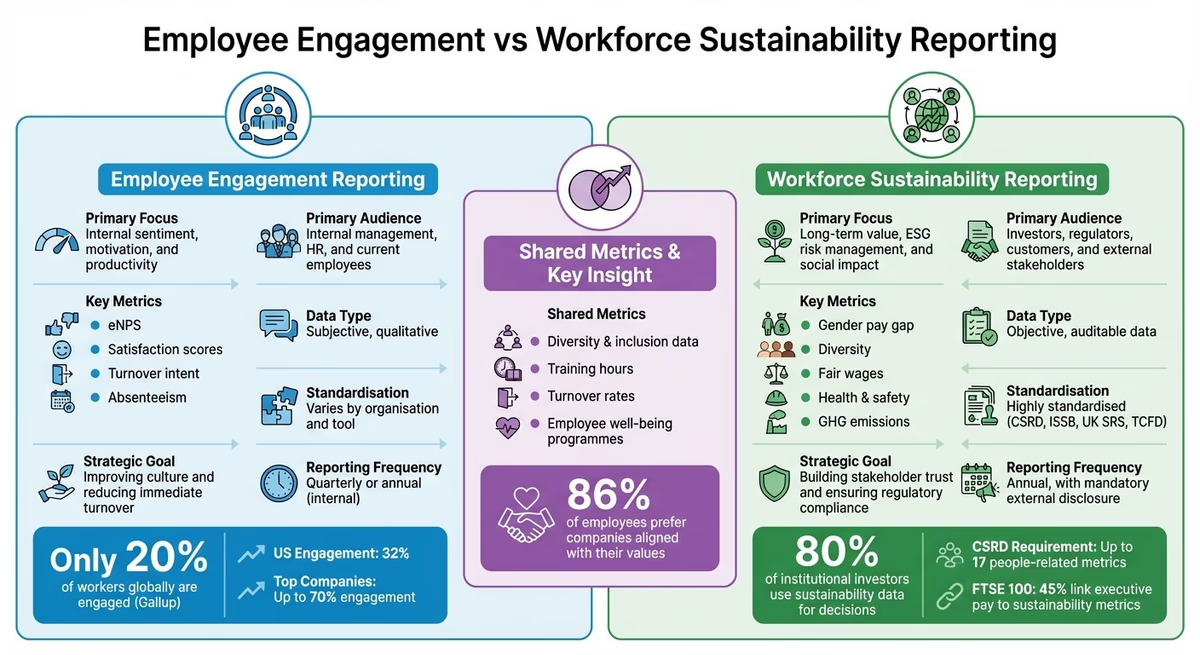

Employee engagement reporting is all about gauging how invested employees are in their company's mission and objectives. It’s not just about whether employees feel satisfied - it digs deeper to identify those who are genuinely motivated and feel supported by their leadership. Gallup's research highlights a striking trend: only 20% of workers globally are considered engaged. In the US, the figure rises to 32%, while standout companies can hit engagement levels of up to 70%.

What It Measures and Why

This type of reporting focuses on psychological commitment rather than surface-level satisfaction. As Ed O'Boyle, Global Practice Leader at Gallup, puts it:

"There's no business reason to define engagement as contentment, except to inflate the percentage of engaged employees on a corporate dashboard."

The aim is to identify employees who are not just content but actively contributing to innovation and problem-solving. Why does this matter? Because engaged employees help drive better team performance, higher productivity, and stronger customer loyalty. A Gallup meta-analysis of over 112,000 teams found that highly engaged teams consistently outshine those with low engagement, excelling in profitability, productivity, and even safety records. These insights are invaluable for turning data into actionable strategies.

Common Metrics and Tools

Engagement reporting often relies on validated survey tools, such as Gallup's Q12. This survey includes 12 carefully crafted questions designed to predict team performance. Using a five-point scale, it’s recommended that organisations share the full range of responses, not just the top-tier results, to maintain transparency and avoid artificially inflated scores.

Key metrics in engagement reporting include morale scores, survey participation rates, retention statistics, and satisfaction levels. However, the most impactful reports go beyond these basics. They establish a clear link between engagement efforts and measurable business outcomes, like lower employee turnover or increased profitability. For organisations advising on workforce strategies, combining these internal engagement metrics with tools like financially-integrated sustainability management offers a more comprehensive view of organisational health. This internal focus on engagement stands in contrast to external workforce sustainability benchmarks, creating a more nuanced approach to performance measurement.

What is Workforce Sustainability Reporting?

Workforce sustainability reporting allows organisations to showcase how their workforce practices create value while adhering to both global and local regulations. Unlike employee engagement reporting, which focuses on internal employee sentiment, this type of reporting is increasingly shaped by external demands from investors, regulators, and lenders. Notably, 80% of institutional investors now rely on sustainability data when making investment decisions. This external focus drives the need for detailed and measurable performance data.

What It Measures and Why

Workforce sustainability reporting tracks a range of metrics, including diversity, employee turnover, gender pay gaps, health and safety, and well-being initiatives. Under the Corporate Sustainability Reporting Directive (CSRD), businesses are required to disclose up to 17 people-related metrics. A key part of this process is the Double Materiality Assessment (DMA), which helps identify workforce-related impacts, risks, and opportunities (IROs) that are financially relevant. These metrics are closely tied to evolving regulatory demands.

In the UK, workforce data must meet high standards of accuracy and reliability, aligning with the ISSB baseline through the UK Sustainability Reporting Standards (SRS). For accounting firms advising on compliance, platforms like neoeco simplify the process by automatically mapping transactions to recognised frameworks such as GHGP, ISO 14064, SECR, and UK SRS, effectively integrating financial and sustainability reporting.

Common Metrics and Frameworks

Key metrics in workforce sustainability reporting include health and safety, employee well-being, diversity, fair wages, and gender pay gap transparency. Gender pay gap reporting is particularly prominent in the UK, where it is a regulatory requirement aimed at ensuring fairness in compensation. Additionally, nearly 45% of FTSE 100 companies now include sustainability targets in executive pay structures, highlighting the growing emphasis on ESG considerations within corporate governance.

These metrics align with established frameworks like ISO 14064 and ASRS 2, promoting consistency across organisations. The Task Force on Climate-related Financial Disclosures (TCFD) also plays a significant role, with its four key pillars - governance, strategy, risk management, and metrics/targets - incorporated into the UK SRS. This requires companies to clearly document how their boards prioritise and address workforce ESG issues. For businesses aiming to stay ahead, consolidating ESG data into a unified system before external audits become mandatory is increasingly important.

Main Differences Between the Two Reporting Types

Looking at the definitions above, the distinctions between internal engagement reporting and external sustainability reporting become clear. While employee engagement reporting focuses on understanding internal dynamics - like how employees feel about their workplace and their likelihood of staying - workforce sustainability reporting shifts the perspective outward. It highlights how workforce practices contribute to long-term value creation and address risks tied to environmental, social, and governance (ESG) factors.

One of the biggest differences lies in the audience. Engagement data typically stays within HR and management circles, helping guide decisions about workplace culture and retention strategies. On the other hand, sustainability data is designed for external scrutiny. It needs to meet the same rigorous standards as financial statements, with transparent audit trails and verifiable data sources.

The metrics used in these reports also differ significantly. Engagement reporting often relies on subjective measures, such as employee Net Promoter Scores (eNPS) or survey-based sentiment analysis. Sustainability reporting, however, depends on objective data, such as gender pay gap statistics, diversity levels, health and safety records, and even Scope 3 emissions from employee commuting. For example, while 26% of workers planned to leave their jobs in 2023 - highlighting internal engagement challenges - 45% of FTSE 100 companies now link executive pay to sustainability metrics, reflecting the external accountability tied to sustainability reporting.

Side-by-Side Comparison

Here’s a quick look at how these two types of reporting stack up:

| Aspect | Employee Engagement Reporting | Workforce Sustainability Reporting |

|---|---|---|

| Primary Focus | Internal sentiment, motivation, and productivity | Long-term value, ESG risk management, and social impact |

| Primary Audience | Internal management, HR, and current employees | Investors, regulators, customers, and external stakeholders |

| Key Metrics | eNPS, satisfaction scores, turnover intent, absenteeism | Gender pay gap, diversity, fair wages, health and safety, GHG emissions |

| Data Type | Often subjective and qualitative | Objective, auditable data |

| Standardisation | Varies by organisation and tool | Highly standardised (CSRD, ISSB, UK SRS, TCFD) |

| Strategic Goal | Improving culture and reducing immediate turnover | Building stakeholder trust and ensuring regulatory compliance |

| Reporting Frequency | Typically quarterly or annual (internal) | Annual, with mandatory external disclosure requirements |

The regulatory landscape further highlights these distinctions. In the UK, public sector organisations with over 500 full-time equivalent (FTE) staff or £500 million in operating income are required to meet minimum sustainability reporting standards. For accounting firms advising on compliance, understanding how to align ESG data with ISSB and UK SRS is critical for producing workforce sustainability reports that are ready for audits.

Where the Two Reporting Types Overlap

Although employee engagement and workforce sustainability reporting serve different purposes and audiences, they share more similarities than many organisations might expect. Both rely heavily on workforce data pulled from HR systems, including metrics like diversity figures, training hours, turnover rates, and employee participation in company initiatives. With 86% of employees preferring to work for companies that align with their values, sustainability efforts not only ensure compliance but also enhance employee engagement. This overlap creates opportunities to identify shared metrics that serve both reporting needs.

Shared Metrics and Objectives

Certain metrics naturally serve both employee engagement and sustainability reporting. For example, diversity and inclusion data helps organisations assess employees' sense of belonging while also meeting external requirements like aligning ESG data with ISSB reporting and UK SRS standards. Similarly, tracking training programmes supports internal engagement by fostering skill development and contributes to sustainability reports by highlighting human capital growth and readiness for roles that support greener initiatives.

Employee well-being programmes also straddle both areas. Internal engagement surveys might evaluate how supported employees feel, while sustainability reports focus on health and safety statistics, fair wages, and work-life balance policies. With 14% of employees worldwide struggling to pay their bills each month, ensuring fair wages has become not only an employee retention priority but also a critical ESG consideration.

Benefits of Integration

Integrating the two reporting approaches offers practical advantages. Instead of maintaining separate systems for data collection, organisations can establish a unified workforce data source to power both internal dashboards and external disclosures. This approach simplifies data management, improving both operational decision-making and regulatory compliance.

Moreover, integration helps organisations move away from superficial "junk metrics" that fail to predict performance. By embedding sustainability goals into their culture and talent strategies, companies can measure deeper factors like emotional commitment and psychological engagement - key drivers of business success. With 45% of FTSE 100 companies now tying executive pay to sustainability goals, the link between engaged employees and credible sustainability results is becoming increasingly evident.

When to Use Each Type of Reporting

Deciding between engagement reporting and sustainability reporting - or using both - depends on your goals. Whether you're looking to enhance internal processes, meet external compliance standards, or achieve both, knowing when to apply each type ensures you're gathering the right insights at the right time. Here's how each approach works best and how combining them can simplify your reporting efforts.

Engagement Reporting for Internal Needs

Engagement reporting is your go-to when focusing on improving internal operations, retaining talent, and fostering a positive workplace environment. If you're struggling with high employee turnover, difficulty hiring skilled workers, or declining productivity, these metrics can provide actionable insights to address the root causes. For example, in 2023, 26% of employees planned to leave their jobs within a year - a jump from 19% in 2022. This underscores the importance of using engagement data to tackle retention challenges before they escalate.

This type of reporting is especially useful for shaping decisions around employee development, well-being programmes, and workforce investments. Unlike external disclosures, engagement metrics focus on qualitative aspects like employee sentiment, emotional connection, and overall commitment to the organisation. These insights are invaluable for creating value internally. When your primary audience is your leadership team and workforce - not regulators or investors - engagement reporting delivers the depth needed to inform policies and strengthen workplace culture.

Sustainability Reporting for External Requirements

On the other hand, sustainability reporting is essential when you're addressing regulatory requirements, investor expectations, or ESG (Environmental, Social, and Governance) obligations. With frameworks like ISSB reporting, CSRD, and UK SRS enforcing stricter workforce disclosure standards, organisations must provide clear, verifiable data on areas like diversity, pay equity, training effectiveness, and health and safety.

Investors are increasingly scrutinising sustainability efforts, with 80% of institutional investors now factoring this information into their decisions. This makes workforce sustainability reporting not just a compliance task but a strategic tool to build trust and even lower capital costs. As Phillippa O'Connor, Workforce ESG Leader at PwC United Kingdom, explains:

"Those that get ahead of this curve, building a comprehensive data strategy that drives workforce reporting and actionable insights, will be best placed to send a clear message this organisation is motivated to do right by its workforce and can be trusted".

Many organisations start with straightforward metrics like workforce composition and costs to simplify audits. Interestingly, only 11% of FTSE 100 companies disclosed internal hire rates, showing that external reporting often prioritises simpler, quantifiable data.

Combined Reporting Approaches

More organisations are now adopting a combined strategy, recognising the advantages of integrating both engagement and sustainability reporting. This approach is especially effective when you need to meet the demands of both internal stakeholders and external regulators. With 96% of companies confident in their ability to meet workforce reporting standards under CSRD, the real challenge lies in merging these efforts seamlessly. Involving HR leaders, CFOs, and Chief Sustainability Officers early on can help close data gaps and reduce reputational risks.

A notable example of this integration is linking executive pay to sustainability outcomes. By creating a unified data system, companies can generate internal dashboards to monitor retention and culture while also producing audit-ready reports for compliance with frameworks like UK SRS or CSRD. Tools like neoeco can simplify this process by connecting financial and sustainability data, eliminating the need for manual conversions or disjointed spreadsheets.

Parul Munshi, Partner, Workforce Transformation at PwC Singapore, highlights the impact of this approach:

"Workforce Sustainability Reporting is an impactful way for an organisation to communicate a clearly defined purpose and the progress it is making in the pursuit of its organisational goals. This goes a long way in building trust with its people and broader stakeholders".

Conclusion

Employee engagement and workforce sustainability reporting may serve different purposes, but both are essential for building trust and creating long-term value. Engagement reporting focuses on understanding internal sentiment, improving employee retention, and strengthening workplace culture - areas where recent data reveals ongoing challenges. On the other hand, sustainability reporting meets external demands from investors and regulators, with frameworks like CSRD and UK SRS requiring detailed, audit-ready insights into diversity, pay equity, and health and safety metrics.

Interestingly, these two areas overlap in meaningful ways. Both rely on the same HR data - such as retention rates, diversity figures, and pay structures - and both aim to show that an organisation genuinely values its people. Transparent reporting isn't just about ticking compliance boxes; it’s a way to attract and retain top talent in a competitive market. This intersection presents a strategic opportunity for accounting firms.

For accounting firms, integrating engagement and sustainability reporting creates a unique chance to offer more comprehensive advisory services. While 96% of companies express confidence in meeting workforce reporting requirements, HR leaders are often left out of the implementation process. By using unified data systems, firms can provide clients with actionable internal insights and ensure external compliance, enhancing the value of their services.

Tools like neoeco simplify this process by combining financial and sustainability data into audit-ready sustainability reports, reducing manual effort and ensuring consistency. This integration aligns workforce metrics with the precision of financial data, minimising errors and protecting reputations.

Whether clients need internal dashboards to track workplace culture or external reports to satisfy regulatory demands, understanding the synergy between these reporting types enables accounting firms to offer more strategic and impactful advice.

FAQs

What are the benefits of combining employee engagement and sustainability reporting?

Combining employee engagement with sustainability reporting gives organisations a more comprehensive view of their social and environmental impacts. This approach helps align workforce strategies with broader sustainability objectives. By including metrics like employee engagement, diversity, and wellbeing in these reports, businesses can pinpoint risks, uncover opportunities, and identify areas that need attention more efficiently.

This integration boosts transparency, simplifies adherence to frameworks such as UK SRS and ISSB standards, and ensures disclosures are ready for audits. It also signals a firm commitment to social responsibility, enhancing the organisation's reputation and strengthening trust among stakeholders.

What are the main metrics used in workforce sustainability reporting?

Workforce sustainability reporting zeroes in on metrics that reveal the social impact of an organisation's workforce. These metrics often include workforce composition - covering details like gender, ethnicity, age, and other demographic factors - as well as engagement, retention rates, and diversity levels. Together, these indicators reflect how much value an organisation places on its employees as a key resource.

Additionally, the reporting typically examines health and safety standards, opportunities for skills development, and labour practices. These areas highlight how a business supports its workforce while aligning with broader sustainability objectives. By monitoring and sharing data in these categories, companies can maintain transparency, address stakeholder priorities, and ensure the long-term, responsible management of their employees.

Why is it essential to align sustainability reporting with regulatory standards?

Meeting regulatory standards in sustainability reporting is crucial for ensuring compliance and delivering accurate, audit-ready disclosures. Frameworks like the UK’s SECR (Streamlined Energy and Carbon Reporting), UK SRS (Sustainability Reporting Standards), and globally recognised standards such as the GHGP (Greenhouse Gas Protocol) and ISO 14064 offer structured approaches to tracking and reporting emissions and sustainability data. Following these guidelines helps organisations avoid penalties and maintain their credibility.

Sticking to these standards also promotes consistency, transparency, and comparability in reports, which can build trust with stakeholders. Additionally, it aligns businesses with broader ESG (Environmental, Social, and Governance) and climate objectives. As regulations continue to shift, staying compliant ensures organisations meet investor expectations, reduce reputational or legal risks, and simplify the often complex task of managing multiple reporting requirements.